Company Overview - Rio Tinto searches for and extracts a variety of minerals worldwide, with the heaviest concentrations in North America and Australia. Major products include aluminium, copper, diamonds, energy products, gold, industrial minerals and iron ore. The 1995 merger of RTZ and CRA, via a dual listed structure created the present day company. The two operate as a single business entity. Shareholders in each company have equivalent economic and voting rights in Rio as a whole.

Analysis – We see the major diversified miners as the most preferred in the space given their ability to manage margins and cash flow. Rio has been focussed on growth and is currently undergoing an expansion of its Pilbara Iron Ore mining capacity to 360Mtpa. However at the London Investor Seminar in December 2013, RIO deprioritised growth from first to third use for funds. RIO’s focus for 2014 is now to reduce net debt and increase returns to shareholders which we think is positive. RIO like its competitors is currently focusing on removing costs from the business, divesting non-core assets, increasing free cash flow and increasing the progressive dividend. We think Rio’s 2014 strategy of reducing debt and increasing returns to shareholders is welcomed by investors and we think a buyback in 2015 may be possible.

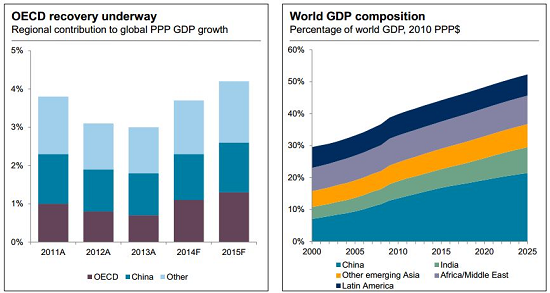

Global demand growth (Source - Company Reports)

Global demand growth (Source - Company Reports)

The outlook for Rio Tinto is largely dependent on the outlook for the iron ore price as well as the urbanisation and income growth of developing nations in particular China given it is the largest contributor to Rio Tinto’s revenue. In our view Rio Tinto is well placed to take advantage of growing demand in emerging markets through its expandable long life operations. Our view is that increasing iron ore supply globally will weigh on the long run iron ore price. However RIO is the lowest cost producer and in our view will continue to be the most competitive player in the iron ore space. RIO# has limited pricing power over most of its products. The notable exception is in iron ore where along with BHP and Vale, Rio is a member of the global seaborne export oligopoly, with 25% share. Minimal pricing power is aggravated by the volatile and cyclical nature of commodity prices. Given Rio’s large , low cost and irreplicable operations, they are in an advantageous position. The lack of comparable mega deposits and increasingly prohibitive capital costs pose barriers to entry.

Exploration and evaluation costs (Source - Company reports)

Exploration and evaluation costs (Source - Company reports)

On 26 May 2014, the government of Guinea and its partners, Rio Tinto, Chinalco and the IFC signed the investment framework for development of block 3 and 4 of the Simandou Project. The US$20bn project is expected to be the largest combined iron ore and infrastructure project ever developed in Africa and is set to provide Guinea with an opportunity to benefit from its rich minerals. The agreement provides the legal and commercial foundation for the project and within the coming days the government of Guinea will submit the investment framework to the Guinean National Assemble for ratification. The Simandou Project is an iron ore mining development in the South East Guinea. The project partners include the Republic of Guinea (7.5%), Rio Tinto (46.57%), Aluminium Corporation of China (41.3%) and the International finance Corporation (4.625%). The project will be the largest combined iron ore mine and infrastructure project ever developed in Africa and has the potential to transform the Guinean economy and transport infrastructure. The project has 3 principal components: 1- A high grade iron ore mine of 100Mtpa at full production; 2- A new 650km trans – Guinean multi-user railway to transport iron ore to the Guinean coast; 3- A new deep water multi user port in the Forecariah prefecture.

Expected capital expenditure profile (Source - Company reports)

Expected capital expenditure profile (Source - Company reports)

Given the renewed momentum, RIO’s outlay of capital to the project over the short term may increase slightly, which could Impact group capital expenditure over the next two years and consequently the potential for increased payback to shareholders. We estimate Rio will spend US$500m on Simandou in each of the FY14 and FY15, relative to RIO’s estimated group capital spend of US$11bn in 21014 and US$8bn in 2015. However given RIO’s recent internal focus on eliminating non-essential capital expenditure, we suspect our estimate could be at the high end.

Net debt profile (Source - Company reports)

Net debt profile (Source - Company reports)

Operationally the mine should be very low cost, based on RIO’s Pilbara metrics (where rail distances are shorter but labour costs are multiples higher). The strip ratio of the mine should also be low due to the topography of the deposit. We do note however that shipping product from guinea to target customers in China and India could attract freight rates of up to US$25/t, or 2-3 times the rate applied to ore transported from Cape Lambert, Australia to Qingdao, china. Arguably the addition of a further 100Mtpa to the seaborne market appears undesirable at a time when investors are nervous about a declining iron ore price, given the recent additional capacity to the market and questions around global demand growth f or the commodity. We do highlight however that the Simandou project is unlikely to be producing for a further six+ years at which point he market dynamics may be more favourable. The mine also uniquely offers high grade Fe, above all of the additional planned production at present. The iron ore deposit at Simandou is considered the last of the world’s high grade iron ore at 65-66% Fe versus Pilbara at 60% Fe and China at sub20% Fe.

RIO Daily chart (Source - Thomson Reuters)

RIO Daily chart (Source - Thomson Reuters)

After years of plumbing the depths, RIO’s aluminium division is resurfacing after a long period of restructuring. Through a combination of cost cutting and asset and product mix optimisation, we see fresh cash flow growing to over US$2b a year during the next there years. The division surprised in 2013 after US$600m of costs were removed and we expect this momentum to continue into 2014. We believe over the next few years the aluminium division will once again become a significant contributor to the Rio portfolio. We see significant upside from a stronger aluminium and bauxite price. The value of Rio’s aluminium business has been mentally written off by the market in our view . We expect this to change in 2014 with the division close to completing the majority of its transformation. After years of generating negative cash flow, the long process of restructuring n RIO’s aluminium division is about to pay off.

RIO’s cash flow base is diversified and the company is less susceptible to the vagaries of the market than the single commodity producers are. The company is run exceptionally well at the asset level and enjoys a broad portfolio of first class low cost assets. We reiterate our BUY on the stock at the current price of $59.40.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...