Company Profile - Santos Limited is an oil and gas producer, supplying Australian and Asian customers. The Company is primarily engaged in the exploration for, and development, production, transportation and marketing of, hydrocarbons. The Company develops major oil and gas liquids businesses in Australia, and operates in all mainland states and the Northern Territory. The Company has exploration-led Asian portfolio, with a focus on three core countries: Indonesia, Vietnam and Papua New Guinea. The Company operates in four business units of Eastern Australia; Western Australia and Northern Territory; Asia Pacific, and Gladstone LNG (GLNG). The Asia Pacific operating segment includes operations in Indonesia, Papua New Guinea, Vietnam, India and Bangladesh.

Analysis – Santos has delivered production of 12.2Mboe in the March Quarter which is down 7% Quarter on Quarter largely due to disappointing oil output from natural decline and some weather related issues. Santos reported a 14% decline in revenue to AUD 913 Million compared with the previous quarter. Revenue was 28% higher than a year earlier. Marginally softer production of 12.2 million barrels of oil equivalent (mmboe) overall was offset by higher than anticipated crude production. Crude is a higher value product and quarterly pricing of AUD 128.50 per barrel improved slightly on the December Quarter. Despite maintenance of the Moomba plant in Cooper basin, gas production was stronger than expected and Darwin LNG sales rebounded strongly 27% quarter on quarter. The Vietnamese Dua oil field is due to come online mid-2014 and should offset some of this decline in oil production.

Hides Gas Conditioning Plant, PNG LNG (Source - Company Reports)

Hides Gas Conditioning Plant, PNG LNG (Source - Company Reports)

Third party revenue may have been down 22% quarter on quarter but interestingly, the cost of purchasing these volumes was down a more notable 28%. As a result EBITDA from this business in 1Q14 was $51m up 6% quarter on quarter. This combined with a strong growth in 1Q revenue of 27% year on year, ahead of oil indexed sales from PNG LNG, confirms the revenue growth should be material in 2014 and again in 2015 after the start-up of GLNG. We note that STO’s own production continues to exceed volumes sold, suggesting an inventory build is occurring.

Santos Assets By Basin (Source - Company Reports)

Santos Assets By Basin (Source - Company Reports)

PNGLNG is now more than 95% completed with start up on track for 3rd Quarter 2014. Condensate production from Hides has commenced and most of the development work on Hides drilling has been completed or is well progressed. The PNGLNG project is on budget and schedule for first cargo delivery is around 3rd Quarter 2014. PNGLNG will contribute around one eighth of expanded Santos revenue from 2015, a major driver of the anticipated 50% jump in forecast 2015 earnings. The short term focus is on delivery of PNGLNG with start up in 3Q2014. The commencement of this project will be the signal of delivery of the company’s growth phase.

Integrated East Coast Portfolio (Source - Company Reports)

Integrated East Coast Portfolio (Source - Company Reports)

Gladstone LNG remains on track and budget for first LNG in 2015 and is now 80% finished. Gladstone will comprise one-quarter of expanded revenue from 2016. Fairview field deliverability continues to exceed expectations. Roma field now has 50 wells on line and dewatering – performing in line with expectations and 3 upstream gas hubs are 85% complete. All pipes to Gladstone are in the ground and 85% are buried. The 4.3km harbour tunnel is complete and the pipes are laid inside – integrity testing has commenced.

Water Treatment Facility, Fairview (Source - Company Reports)

Water Treatment Facility, Fairview (Source - Company Reports)

LNG project progress means development risk is greatly reduced and cost pressures from rising Australian dollar and tight labour and contracting capacity have significantly abated in the past year. Commissioning of East Coast export plants is driving domestic gas prices higher. Santos is Australia’s largest domestic gas supplier and little additional capital is required to take advantage of the higher domestic gas prices.

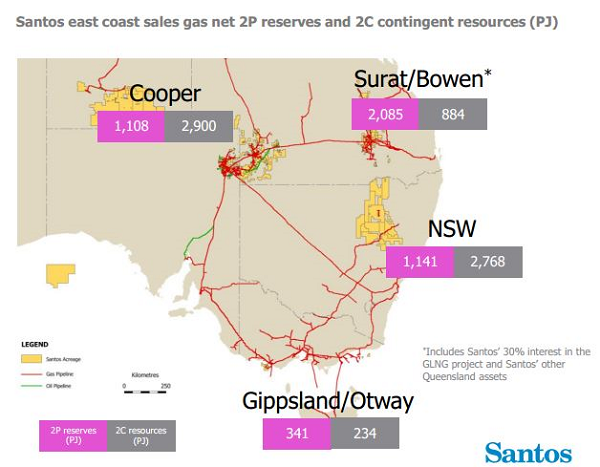

Australia's Natural Gas Reserves (Source - Company Reports)

Australia's Natural Gas Reserves (Source - Company Reports)

The cooper unconventional programme progresses and some early data has been reported with flow rates on the flow Langmuir – 1 and Roswell – 2 wells. Although the data is not definitive we are encouraged by the early results with Langmuir flowing at 1.5mmcfd constrained by fluid inflow and Roswell flowing at 0.75mmcfd from a five stage frac only, in a limited horizontal section. This asset play is strategically important for Santos to provide the next tranche gas opportunity that will be required to not only replace the 750PJ committed from the Cooper Basin to GLNG but will also provide domgas supply volumes.

Narrabri Gas Project (Source - Company Reports)

Narrabri Gas Project (Source - Company Reports)

Santos proposes to develop its coal seam gas reserves in the Narrabri area in North West New South Wales to provide a much needed source of natural gas for the State. Momentum is seemingly building in Narrabri CSG operations as STO ramps up drilling, re-starts existing pilots and progresses the construction of new water processing facilities. We still see the ramp up to 100TJ/d of Narrabri gas production by 2020 achievable.

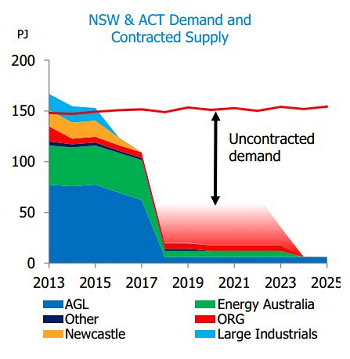

NSW Gas Supply (Source - Company Reports)

NSW Gas Supply (Source - Company Reports)

Despite lower oil price forecast over coming years earning should grow strongly following the start-up of the PNG and GLNG projects. ExxonMobil the operator has suggested that the PNGLNG project should reach peak rates within 4 months of start-up. The two LNG processing trains will have capacity of 6.9Mt/year. The GLNG project will sell its first LNG cargo in 2015. Given the rate of construction we consider the first cargo will be made in 1Q2015. The two train projects will have a total capacity of 7.8Mt/year. The first train should reach peak rates within 6 months but STO continues to state the second train will ramp up to peak rates over 3 years.

STO Daily Chart (Source - Thomson Reuters)

STO Daily Chart (Source - Thomson Reuters)

The company’s historical reliance on the cooper basin as the core asset is shifting towards new LNG projects at Gladstone and in PNG. This means a rising proportion of revenues will be linked to oil prices rather than the CPI linked gas contracts. The company is also pursuing an Asian growth strategy. The Cooper Basin’s unconventional potential could become a significant asset if industry evaluation demonstrates commerciality. We reiterate our BUY on SANTOS at the current price of $13.75.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...