Company Overview –The Company is engaged in oil and gas exploration and production. The Company’s operating segments include gas and oil. The gas segment include the Company’s interest in the coal seam gas permits in the Surat Basin in Queensland, and its unconventional gas prospects in the Cooper Basin in South Australia. Its oil exploration and production segment pertains to the Company’s interest in oil prospects in the Cooper and Eromanga Basins in South Australia and Queensland. The Company’s subsidiaries include Azeeza Pty Ltd, Victoria Petroleum Offshore Pty Ltd, Victoria Oil Pty Ltd, Victoria International Petroleum N.L., and Remers Pty Ltd. In January 2013, the Company sold 100% interests in Port Bonython Fuels Pty Ltd (PBF). Senex energy conducts its operations through three business areas namely oil business, coal seam gas business and unconventional gas business.

Analysis – SXY delivered a strong quarterly result and continues the theme of Cooper Western Flank players offsetting the oil field decline with successful well connections. SXY has around 6-8 successful wells ready to come online over the 2

nd half, in addition to the anticipated discoveries, so we forecast significantly higher production during 2

nd half 2014. We believe that SXY offers the best value and running room among the cooper basin focused players.

Source - company Reports

Source - company Reports

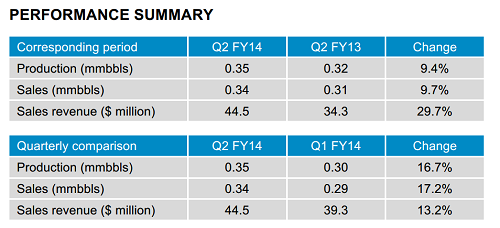

Senex reported strong beat in its top line – production, sales pricing and therefore revenue. Production was 0.3mmbbls. This continues the theme of strong production in the cooper. New wells coming online helped offset decline. Sales volume was 0.34mmbbls. Sales revenue was A$44.5 Million. Oil pricing was A$131M/bbl. Capex of A$53Million includes another A$5Million of license acquisition costs.

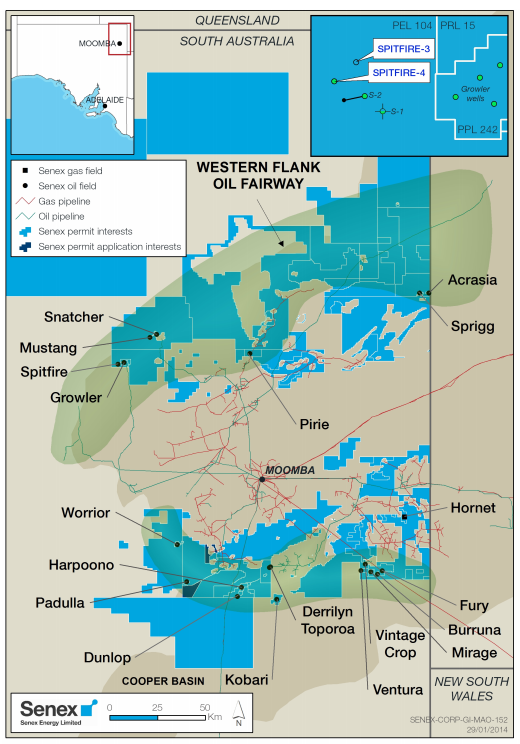

SXY is on track to drill the planned 30 Oil wells in FY14, with 15 completed in 1H and 15+ planned in the second half. The second half oil drilling program is focussed more on the Western Flank Licenses, including Snatcher, Growler and Spitfire. The spitfire region hold particular potential after Spitfire-4 extended the length of Spitfire field to 1 Km. Prospectivity analysis across Senex permits in the Cooper – Eromanga basin delivered more than 450 oil and gas leads and prospects. Oil prospects being developed from the interpretation of the Cordillo and Dundinna 3D seismic surveys should be incorporated in to the series later in CY14. Dundinna processing commenced in Dec-13 quarter. The existing and future dataset of prospects from 3D seismic gives us confidence that the current rate of drilling in FY14 of 30+oil wells can be sustained for some years.

Over the last three years Senex has focussed on rapid growth through both organic and inorganic means. Their strong production profile today is in part due to the acquisition of Stuart Petroleum Limited in 2011 and highlights the rewards of a dual track growth strategy.

Senex delivered net oil production of 0.35 mmbbls for the three months to 31 December 2013, up 16.7% on the previous quarter and a new quarterly production record. This result coupled with an expected lift in production as new wells are brought on line means that Senex is on track for achieving production guidance of 1.4 mmbbls to 1.6 mmbbls for FY14.

Senex delivered record oil revenue, with the revenue for the three months to 31

st December 2013 of $44.5 million representing a 13.2% improvement on the September Quarter. Senex oil sales for the December quarter were 0.34 mmbbls, up 17.2% on the previous quarter. Underpinning the record revenue result was a strong US dollar Brent oil price and a favourable AUD/USD exchange rate.

Senex offers significant exploration upside through the potential commercialisation of its 1.2Million net acres of unconventional gas acreage through PEL 115 and PEL 516 in the cooper basin, targeting the full spectrum of gas plays such as the Roseneath and Murteree shales and the Epsilon and Patchawarra tight sand formations. Production testing at the Worrior – 8 development well flowed gas from the Patchawarra Formation at a rate of 0.7 Million standard cubic feet per day and flowed oil at a stabilised rate of 670 bopd. This was the first time that crude oil had been produced from the Patchawarra Formation at the Worrior Oil Field.

Source - Thomson Reuters

Source - Thomson Reuters

The Dunlop 1 exploration well intersected approximately 3 metres of net pay in the McKinlay Member and flowed at 1200 barrels of oil per day (bopd) during drill stem testing. The well began extended production testing in December quarter. Thee Burruna-3 appraisal well intersected approximately 3 metres of net pay in a previously untapped oil accumulation in the lower Birkenhead formation. The well also successfully intersected the Namur formation that delivered flow rates of up to 3600 bopd at Burruna-2. The spitfire structure now extends for more than 1 kilometre from spitfir4 to spitfire1 and the field volume has been further increased with Spitfire – 4 intersecting oil around five metres higher than in spitfire -2.

Source - Company Reports

Source - Company Reports

In November 2013, Senex quantified a significant contingent oil resource within the Murta Formation sandstones across the southern region of the South Australian Cooper-Eromanga Basin.

At the end of December quarter Senex was in a strong financial position with no debt and cash and liquid investments of $102.5 Million. Oil Sales revenue for the quarter was $44.5 Million and major expenditure categories for the period are shown below.

Source – Company Reports

Source – Company Reports

There is potential to greatly expand oil production in low risk fashion on the western and southern flanks of the Cooper Basin. It also includes some value for SXY’s cooper unconventional gas exploration acreage including Hornet and its QLD coal seam gas licenses. They could feed the tight market emerging on Australia’s East coast. Some of the key risks that we see are development delays, exploration and infrastructure risks. The current drilling program also includes further wells at Spitfire, Growler and Snatcher, which will seek to extend the reserve coverage areas of the fields. We continue to see oil reserve upside as a key near term catalyst. We will be putting a BUY on SXY at the current price of $0.685.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...