Company Overview –The Company is engaged in oil and gas exploration and production. The Company’s operating segments include gas and oil. The gas segment include the Company’s interest in the coal seam gas permits in the Surat Basin in Queensland, and its unconventional gas prospects in the Cooper Basin in South Australia. Its oil exploration and production segment pertains to the Company’s interest in oil prospects in the Cooper and Eromanga Basins in South Australia and Queensland. The Company’s subsidiaries include Azeeza Pty Ltd, Victoria Petroleum Offshore Pty Ltd, Victoria Oil Pty Ltd, Victoria International Petroleum N.L., and Remers Pty Ltd. In January 2013, the Company sold 100% interests in Port Bonython Fuels Pty Ltd (PBF). Senex energy conducts its operations through three business areas namely oil business, coal seam gas business and unconventional gas business.

Analysis – Senex is growing its oil business significantly focusing on exploration and development in the Western Flank Cooper Basin, South Australia. We believe there is a significant oil growth play not being recognised by the market but certainly supported by reserves additions and drilling results particularly delivered over the last few years. Senex is conducting a 30 well oil drilling programme through FY14 with 25 out of 27 well successful to date including a number of new pool and new field discoveries within the Western Flank acreage.

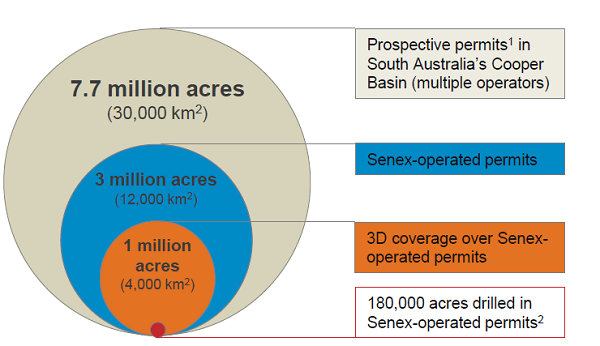

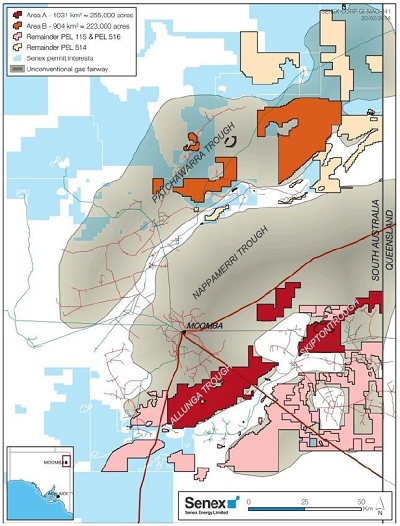

Cooper Basin Operations (Source - Company Reports)

Cooper Basin Operations (Source - Company Reports)

The company is set to increase its coal seam gas reserves in an increasingly shorter Queensland gas market and we suspect it may be able to monetise this asset by end – 2014. A number of recent CSG transactions in Queensland serve to highlight how limited gas supply options are and how the focus is turning to those plays with only limited development to date or still in an evaluation phase. We see Senex as strongly placed within that environment with well-located permits and credible JV partners.

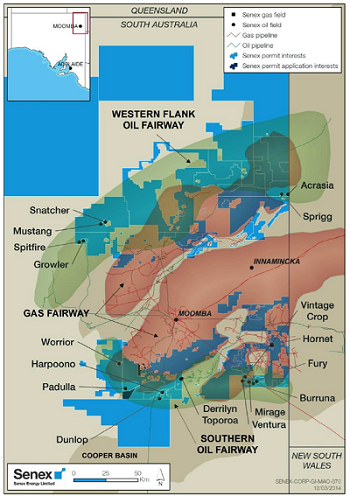

Experienced Cooper Basin Operator (Source - Company Reports)

Experienced Cooper Basin Operator (Source - Company Reports)

In its unconventional gas business, Senex is further evaluating shale and coals in Cooper, which is attracting plenty of interest as a tight gas play. We note that the company recently declared a new gas field at Hornet and booked more than 3.5Tcf of contingent resources attributable. The location of the field some 30km from Moomba-Sydney transmission pipeline makes this accumulation ideal for rapid commercialisation. The company is conducting field development studies which ware likely to continue till the end of 2014. Senex remains the only company of scale and unaligned with a major partner in the cooper unconventional play which we see as in a strategically advantageous position at this stage.

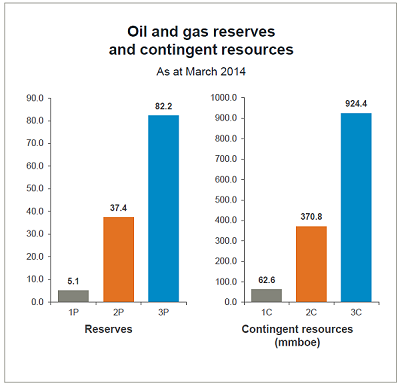

Oil & Gas Reserves (Source - Company Reports)

Oil & Gas Reserves (Source - Company Reports)

Senex released its 1Q14 Quarterly operations report indicating production volumes of 300kb underpinning quarterly revenue of A$37.3mn. Production was down 14% and revenue was down 16% quarter on Quarter, on strong realised oil prices of A$129/b. Quarterly oil production of 300kb was weaker than anticipated and represents a very soft outcome. Sales volumes mirrored the fall in production but again pointed to a small inventory build. Sales of 290kb were down 15% Quarter on Quarter (340kb). The company realised A$129/b in the period for the oil prices (4Q13 : A$131/b). On weaker volumes sales revenue fell 16% Quarter on Quarter to A$37.2 Mn.

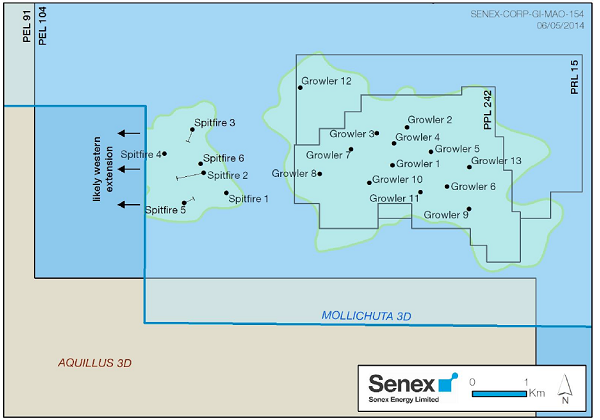

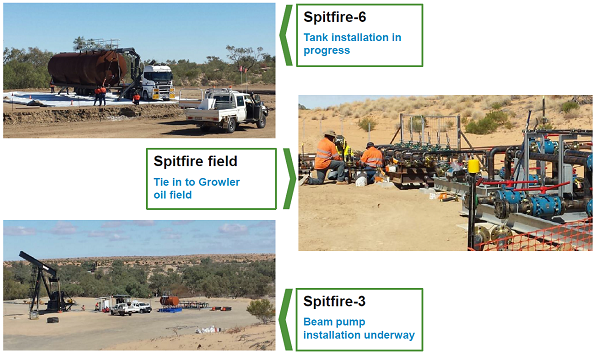

Spitfire Oil Field Extended (Source - Company Reports)

Spitfire Oil Field Extended (Source - Company Reports)

The 30 well oil drilling is well underway and has delivered 25/27 successes by our estimate with extended production testing underway at Dunlop and Spitfire-4 intersecting 13.5m net pay. Analysis of the data from the four core holes commenced in the Senex-operated (45%) western Surat Basin CSG permits post desorption testing. In the QGC – operated eastern permits Senex expects to commence work on 6 wells later in 2014. At the end of the period the company had A$91mn (4Q13: A$102mn) in cash with no debt and is fully funded for work programmes through to end-2014. An unconventional JV deal with origin is worth up to $252mn and provides some arm length validation for the Southern Cooper Basin gas potential, although first drilling is targeted for 2015.

Senex & Origin Energy Focus on Tight Sands (Source - Company Reports)

Senex & Origin Energy Focus on Tight Sands (Source - Company Reports)

We highlight a number of specific excellent, drilling results: The Spitfire results are very good, with the S-3, 4 and 6 wells intersecting thicker than expected sands. Spitfire-4 intersecting 13.8m net oil in the Birkhead, which is the largest oil column in the field – this well has already been placed on production. There is 20.8m gross oil column (13.8m net column) in the target Birkhead sands. This has extended the field by approximately one kilometre (from spitfire – 1). This will likely lead to significant reserves upside in our view.

Work Underway at Spitfire (Source - Company Reports)

Work Underway at Spitfire (Source - Company Reports)

The announcement of an unconventional JV deal with origin worth up to $252mn caught the markets’ attention although the initial positive reaction has dissipated from the share price. It has been over a year since Senex first flagged that it would seek a partner in the cooper unconventional, the farm in excludes existing discoveries which gives sxy the upside and now some financial flexibility to get after the project. If there is a downside it’s that there is no immediate activity driver – the next 12 months is about seismic acquisition and interpretation ahead of drilling to commence in CY15. Upon success a second stage drilling campaign with pilot testing and economic evaluation will be undertaken, perhaps for another two years. It seems obvious that ORG have determined this project is long dated perhaps targeting FY18.

SXY Daily Chart (Source - Thomson Reuters)

SXY Daily Chart (Source - Thomson Reuters)

In light of the decline faced at Growler, SXY is now pointing to the bottom end of its 1.4 – 1.6 mmbbl guidance range. While production rates in June quarter will have to improve by 50% to deliver the bottom end of this range, SXY has or plans to tie in a number of wells which will see production increase in the current quarter. The onset of pressure decline at SXY’s largest producing field earlier than expected is disappointing. However management appear to be reacting quickly by committing to water flood project next year. Separately SXY appears on track to deliver significant reserves additions in the coming years. We reiterate our BUY on the stock at the current price of $0.68.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...