Company Overview - The Company is engaged in oil and gas exploration and production. The Company’s operating segments include gas and oil. The gas segment includes the Company’s interest in the coal seam gas permits in the Surat Basin in Queensland, and its unconventional gas prospects in the Cooper Basin in South Australia. Its oil exploration and production segment pertains to the Company’s interest in oil prospects in the Cooper and Eromanga Basins in South Australia and Queensland.

Analysis – Senex is growing its oil business significantly focusing on exploration and development in the Western Flank, Cooper Basin, South Australia. We believe there is a significant oil growth play not being recognized by the market but certainly supported by reserves additions and drilling results particularly delivered over the last few years. Senex has completed a 30 well oil drilling programme through FY14 with 26 out of 30 wells successful to date including a number of new pool and new field discoveries within the Western flank acreage.

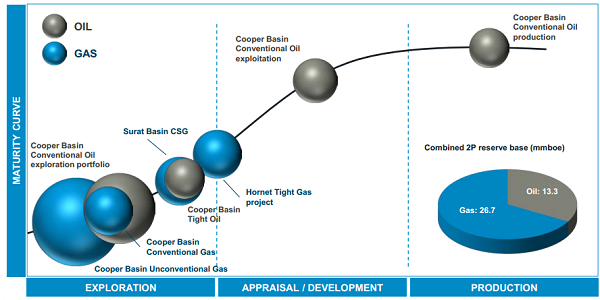

Senex's Oil & Gas Portfolio (Source - Company Reports)

The company is set to increase its coal seam gas reserves in an increasingly shorter Queensland gas market and we suspect it may be able to monetize this asset through FY15. A number of recent CSG transactions in Queensland serve to highlight how limited gas supply options are and how the focus is turning to those plays with only limited development to date or still in an evaluation phase. We see Senex as strongly placed within that environment with well located permits and credible JV partners.

Wells Drilled + Production + Revenue (Source - Company Reports)

In its unconventional gas business, Senex is further evaluating shales and coals in Cooper, which is attracting plenty of interest as a tight gas play. We note the company has recently declared a new gas field at Hornet and booked more than 3.5Tcf of contingent resources attributable. The location of the field some 30km from the Moomba-Sydney transmission pipeline makes this accumulation ideal for rapid commercialization. The company is set to commence a testing and evaluation phase on Hornet in October 2014.

SXY's Asset Portfolio (Source - Company Reports)

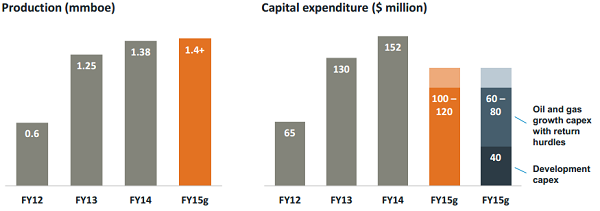

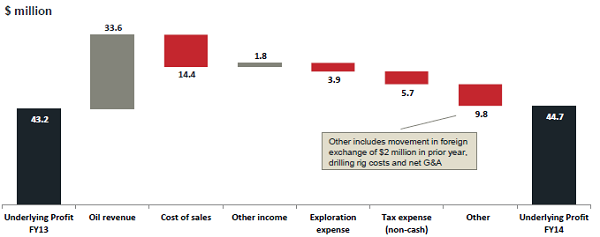

Senex released its FY14 financials with reported NPAT of $37.9m and underlying NPAT of $44.7m. The result is somewhat disappointing, as a 24% increase in revenue has only translated to $1.5m increase in underlying NPAT although gross operating margins remained strong. The company has released FY15 production guidance at 1.4Mboe+ and we see this estimate as conservative. Capex guidance is set at $100 – 120m.

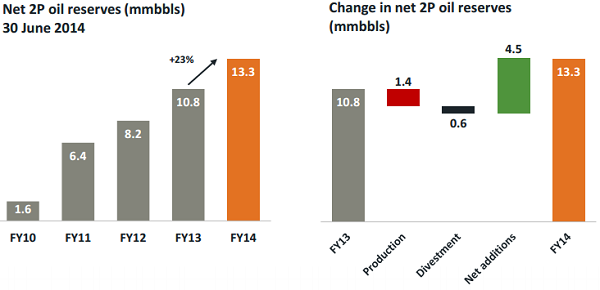

Net2P Oil Reserves (Source - Company Reports)

Net2P Oil Reserves (Source - Company Reports)

The company has outlined an ambitious and aggressive growth acceleration strategy (GAS) for the period to FY18 looking (as a set of aspirational targets) to grow: 1) Production to 3-5Mboe from 1.38Mboe in FY14. 2) 2P reserves to 100-150Mboe (net) - from 42Mboe (FY14). These targets are derived from existing asset base and permit holdings and imply a significant rate of new discoveries. We believe there is no shortage of growth opportunities, and in our view it will come down to funding and being able to conduct the required work within the timeframe. Given the size of these targets gas commercialization is likely to feature prominently in this strategy. However with much of the gas portfolio still in the exploration/early appraisal phase and with pilot production planned at both Hornet and Vanessa in FY15,

SXY will seemingly have to move quickly to full field development to meet these targets organically.

FY15 Guidance (Source - Company Reports)

FY15 Guidance (Source - Company Reports)

The outlook for FY15 will be about continuing to deliver on the oil potential in terms of production and reserves growth although we see some value potential in progressing commercial activities associated with the Hornet gas opportunity. A continuing focus on conventional oil activity, after all it is the high margin prize with some 85% of the nominated wells targeting the play. Oil drilling will continue to be predicated on 3D seismic and we note with interest the extension of that exploration premise into the conventional gas play. Of importance in FY15 will be the activity conducted in the northern Cooper Basin areas and particularly the PEL182 area containing the Vanessa – 1 gas discovery.

Underlying Profit (Source - Company Reports)

Underlying Profit (Source - Company Reports)

The Hornet appraisal programme is set to commence from October 2014 and could be important as a substantial and relatively rapid addition to the production profile. We hold to our investment premise that the oil play can continue to drive incremental growth and a base case of reserves replacement certainly over the next 3-5 years is not an unrealistic scenario in our view.

SXY has been awarded the CO2013-A and CO2013-D permits which are more than 3000km

2 in the SA Cooper Basin. To secure the blocks SXY has bid a total work program of A$72m including up to 22 wells and 1,175km

2 of seismic over the exploration period. With limited 2D seismic data and only one well drilled across this license previous exploration activity remains limited. The CO2013-A permit is located west of SXY’s Worrior and Padulla fields and is on trend with Western Flank oil fields. The primary targets include stack oil plays, both

stratigraphic and structural gas plays, and conventional gas. The CO2013-D permit covers 3,114km

2 south of SXY’s Burrana oil field.

While little progress has been reported on SXY’s Surat Basin Coal Seam Gas interest over the last 12 months, management has suggested that an update here is imminent, which could prove a positive catalyst. While the CSG assets have been earmarked for divestment in the past given the focus on gas development to meet long term targets, SXY could look to sole risk development.

SXY reported that 7.8mb of oil reserves remain undeveloped (largely relating to the Patchawarra at Worrior and Spitfire extensions). This would seemingly represent low hanging fruit which could be developed at low costs /low risk to grow short term production. That said the six development wells budgeted for in the FY15 capital program would look to exploit this untapped potential.

We believe SXY offers the best value among its Cooper Basin focused peers. Management has outlined an ambitious growth strategy to FY18 with an aim to more than double the production and 2P reserves. We think that is achievable but FY15 will need to set the base. We put a BUY recommendation on the stock at the current price of $0.59.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...