Company Overview

Company Overview - Sirtex Medical Limited is an Australia-based healthcare and medical device company, which manufactures and distributes liver cancer treatments utilizing small particle technology. The Company's segments are based on the regional markets it operates, which include Asia Pacific, The Americas, and Europe, the Middle East and Africa (EMEA). The Company's lead product is a focused radiation therapy known as SIR-Spheres Y-90 resin microspheres, which is a radioactive treatment for liver cancer. The treatment is called Selective Internal Radiation Therapy (SIRT) and consists of a minimally invasive surgical procedure performed by an interventional radiologist. The SIR-Spheres microspheres lodge in the small blood vessels of the tumor where they destroy it from the inside over a short period while sparing the surrounding healthy tissue. It is available in more than 40 countries and over 900 hospitals. The Company has manufacturing and operations in the United States, Germany and Singapore.

.png)

SRX Details

Finished patient recruitment for SIRveNIB clinical study: Sirtex Medical Limited (ASX: SRX) finished its patient recruitment for SIRveNIB clinical study in patients with unresectable primary liver cancer (hepatocellular carcinoma or HCC). Pierce Chow, a major Investigator of the SIRveNIB study, commented that they are also pursuing several major secondary endpoints besides primary endpoints which comprise comparison of the side effects and patient quality of life. SIRveNIB is a major Asia Pacific study which is a direct comparison to SIRT and sorafenib, while a major randomized study was being made on sorafenib in the region. The SIRveNIB clinical study is specifically designed to examine the efficacy and safety of SIRSpheres® Y-90 resin microspheres against sorafenib, which is the present standard of care systemic treatment in advanced HCC, especially with Asian population. The group recruited >360 patients for the study and conducting at over 10 Asia-Pacific countries which even comprise New Zealand with 27 centers. SRX expects its SIRveNIB study results to be available by the first half of 2017.

Meanwhile, in the month of April the group also finished Patient Recruitment for its RESIRT study, investigating the use of SIRSpheres® Y-90 resin microspheres for treating key Renal Cell Carcinoma (RCC) which is the most common type of kidney cancer. David N. Cade, the group’s Medical Officer commented that RESIRT is the first clinical study investigating the use of SIR-Spheres microspheres outside of the liver. Based on SEER, over 61,560 new cases of kidney cancer in the United States were reported in 2015, which is 3.7% of all cancer cases, and RCC comprises 90% of all new kidney cancers. Early results of the RESIRT study are expected by the fourth quarter of 2016.

Sirtex’s target opportunity: The group expects its addressable market to be increasing in the coming years. SRX believes that their elevation to higher treatment lines would substantially expand their market opportunity. Based on company’s reports, over 965,000 cases have annual incidence of colorectal cancer (the group’s target markets) with 50% of them developing secondary liver metastases from primary colorectal cancer. From these, over 349,000 get palliative treatment which involves chemotherapy, biologic agents and SIR-Spheres microspheres. Accordingly, the group estimates around 279,000 would be qualified for SIR-Spheres microspheres by 2016 – 2020. For hepatocellular carcinoma, over 616,000 reported an annual incidence of hepatocellular carcinoma (which is the other group’s target markets) with 50% of them that is around 308,000 in their Intermediate to advanced stage disease. Around 262,000 patients are eligible for palliative treatments which involves TACE, Sorafenib and SIR-Spheres microspheres. Accordingly, over 209,000 are eligible for SIR-Spheres microspheres. On the other side, the group has already built a broad reimbursement coverage for its SIR-Spheres microspheres including Medicare and Private Payers for US while EMEA’s region coverage is broad and specific to country. Meanwhile, the group’s major clinical program finished patient recruitment.

.png)

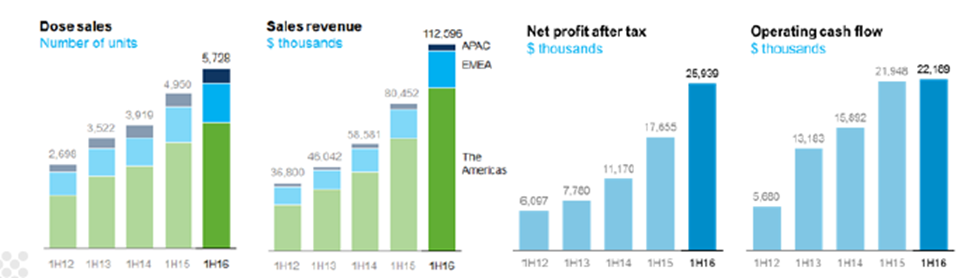

Strong clinical results driving the potential opportunity (Source: Company Reports)

Decreased second half performance estimates: The group reported an outstanding dose sales of 5,728 doses, which is an increase of 15.7% for the first half of 2016, against prior corresponding period, while revenues surged by 40% to $112.6 million. Sirtex net profit after tax delivered even better performance, which is 46.9% more against the same period of last year. The group delivered a CAGR dose sales (as of first half of 2016) of 19.8% while revenues improved 27.0% for the same period. Sirtex even enhanced their cash by 33% to $73.7 million and has no debt. Meanwhile the group issued a lower than estimated trading update for second half of 2016 on the back of dose sales performance impact in the EMEA and APAC regions. This subdued performance is mainly due to delays incurred in realizing product reimbursement in certain major EMEA countries coupled with unexpected delays in SIRFLOX clinical study in the Journal of Clinical Oncology Publication than expected leading to limited sales and marketing initiatives. Moreover, tighter funding environment in many major European markets and provisional supply disruptions in certain Asian markets is also leading to slowdown in these regions. On the other hand, the group expects an ongoing solid performance in the Americas, with dose sales growth expected to be in the range of 18% to 20% for the second half of the year and forecasts a similar range even for the fiscal year of 2016.

However, with the estimated slowdown in EMEA, the group revised their overall full year dose sales estimates in the range of 15% to 17%. But, management believes that on a long term perspective, their core SIR-Spheres Y-90 resin microspheres product would be solid as this core product has penetrated only over 2% of the target market till date.

First half of 2016 performance (Source: Company Reports)

Received regulatory clearance in Canada and endorsement from NICE: In the month of April, the group reported that UK National Institute for Health and Care Excellence (NICE) gave a new Medtech Innovation Briefing (MIB) and commented that NHS doctors and commissioners might consider SIR-Spheres® Y-90 resin microspheres as an alternative to standard therapy having trans-arterial chemoembolization (TACE) or sorafenib in the treatment of patients having inoperable primary liver cancer (hepatocellular carcinoma or HCC). NICE commented that current clinical research indicates that SIR-Spheres microspheres is as capable as TACE as well as sorafenib. With just only these two effective therapy options, NICE MIB reported that SIR-Spheres Y-90 resin microspheres is an additional option for NHS patients.

NICE reported that this local radiotherapy form is well tolerated as well as appropriate for the patient. This update would further strengthen the group’s UK market wherein the funding of its product would be available in specialist centers through the commissioning via evaluation process for those patients who have earlier treated inoperable, liver predominant metastatic colorectal cancer and intrahepatic cholangiocarcinoma. On the other side, the group even got Medical Device Licence (MDL) for SIR-Spheres® Y-90 resin microspheres from Health Canada. This license would enable the group to provide SIR-Spheres Y-90 resin microspheres as a Class III medical device for treating patients having advanced non-operable liver cancer in Canada.

Stock performance: The shares of Sirtex Medical Limited have been under pressure in the last six months and fell over 33.7% (as of June 17, 2016) as the group issued a lower than estimated forecasts for EMEA region in the second half of 2016. On the other hand, the group has lot of room to expand product penetration having over 61,000 doses offered for more than 950 medical centers in over 40 countries till date. The group delivered a ten year CAGR of 30.1% and undertaking solid expansion strategies which would continue to grow its SIR-Spheres business. SRX new clinical evidence in mCRC/HCC would lead to an adoption at earlier stages of disease. The group intends to enhance their number of treatment sites, trained clinicians, as well as output. They are pursuing efforts to expand reimbursement coverage and geographic expansion, as well as looking for new indications like kidney.

On the other side, SRX is even making efforts to strengthen its management position and recently appointed Kevin Richardson as CEO of the Americas Region starting from July 01, 2016, who is now the General Manager and Vice President for North America for the group. Having a low penetration till date of over 2% and forecasted addressable patient population of 488,000 per annum, the group’s long term prospects are solid despite short term challenges. We believe long term investors need to leverage the recent correction in the stock. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $26.89

.PNG)

SRX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...