Kalkine has a fully transformed New Avatar.

Company Overview: South32 Limited (ASX: S32) is a globally diversified mining and metals company involved in the production of bauxite, energy coal, metallurgical coal, alumina, aluminum, manganese, nickel, silver, lead, and zinc. The company’s operations are located in Australia, Southern Africa and South America. The company has a diversified profile of customers spread across Australia, Singapore, Southern Africa, Switzerland, Netherlands, India, China, etc. The company has developed various partnerships with junior explorers with a bias to base metals..png)

S32 Details.png)

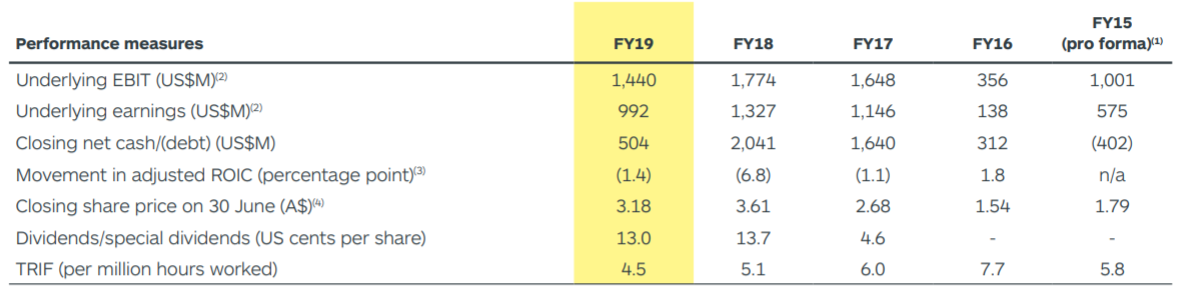

Track Record of Rewarding Shareholders: South32 Limited (ASX: S32) is a globally diversified metals and mining company with operations in Australia, Southern Africa, and South America. The company’s portfolio is diversified by commodity and customer with growth options embedded and a pathway to exit low returning businesses. It is worth noting that the company’s diverse portfolio strengthens its resilience to the disruption of any one commodity, geography, or operation, compared with single mine or commodity companies. With the disciplined allocation of capital and a simple capital management framework, the company has been able to reward its shareholders through dividends in the past few years. During 2015-2019, the company’s underlying EBIT and underlying earnings have increased at a CAGR of 9.5% and 14.61%, respectively.

Financial Highlights for Last 5-Years (Company Reports)

With a focus on optimising the performance of its existing operations and unlocking its potential by converting high-value resources into the reserve, the company intends to create a pipeline of high-quality development opportunities in commodities with strong fundamentals into the future. The company has maintained its focus on improving return on invested capital and prioritising a strong balance sheet to ensure that it remains in control through economic cycles. With a robust balance sheet and resilient portfolio, the company seems to be well-positioned to successfully navigate the current period of uncertainty, caused by Covid-19. The company aims to outperform its peers by reshaping its portfolio which will create exposure to high-quality operations in commodities with a strong and sustainable outlook.

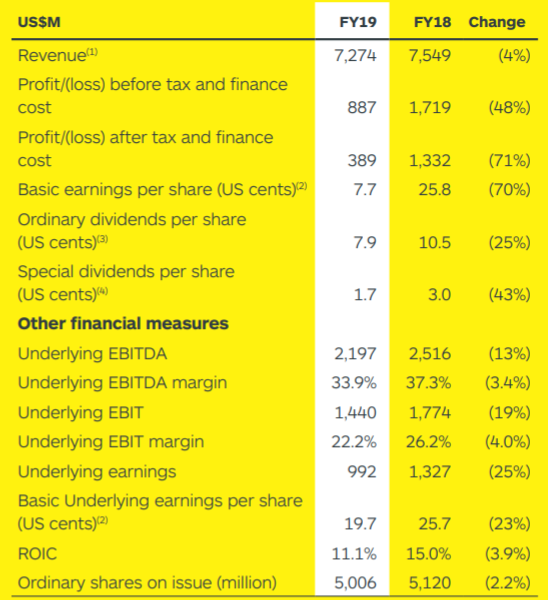

FY19 Performance Highlights: During the financial year 2019 or FY19, the company saw strong operating performance which allowed it to deliver underlying EBITDA of US$2.2 billion with an operating margin of 34% and free cash flow of US$1 billion. The company’s statutory profit after tax stood at US$389 million in FY19.

In FY19, the company saw record production at Hillside Aluminium, a 57% increase in volumes at Illawarra Metallurgical Coal and strong manganese ore production of 5.5 million tonnes, underpinning a 3% increase in the total production volumes. Progressing on its strategy of reshaping and improving its portfolio to promote long-term shareholders’ value, the company completed the acquisition of Arizona Mining, acquired a 50% interest in the Eagle Downs Metallurgical Coal project, and progressed the divestment of South Africa Energy Coal. Over the period, the company returned US$938 million to shareholders and ended the year with a net cash balance of US$504 million. For the full year, the total dividend stood at US 7.9 cents per share.

Snapshot of FY19 Results (Source: Company Reports)

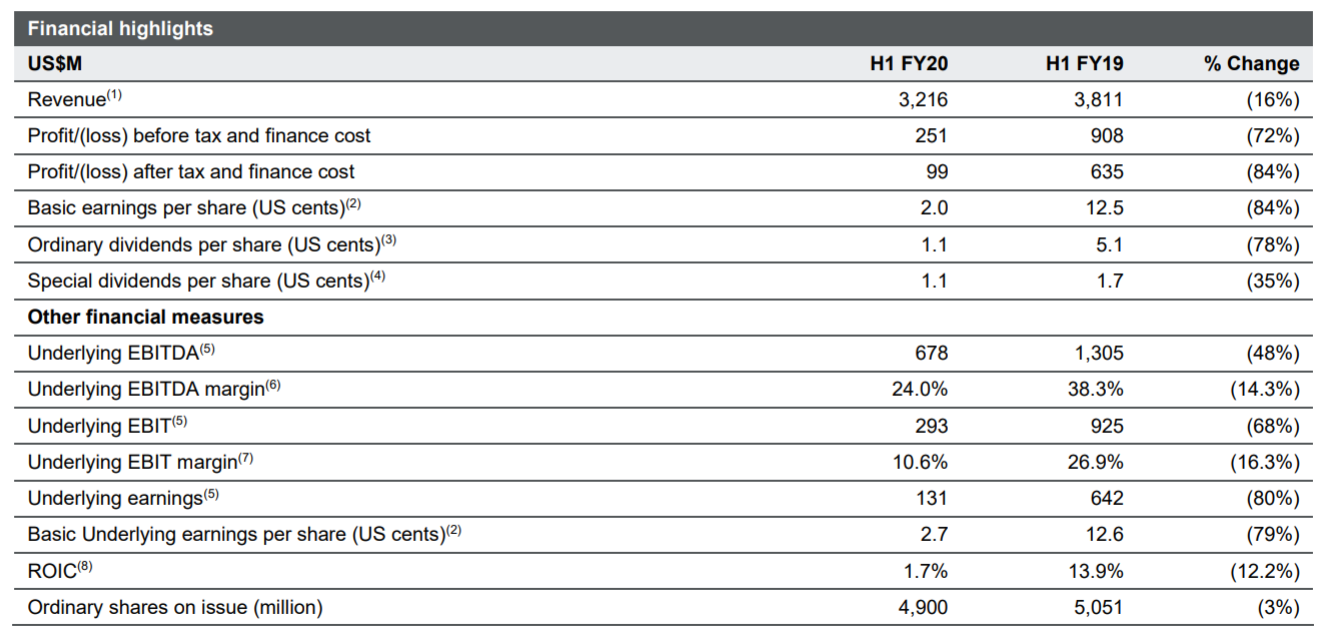

H1FY20 Performance Highlights: For the first half of FY20, the company reported an underlying EBITDA of US$678 million and a free cash flow of US$284 million. During the half-year period, the company maintained higher output rates at Worsley Alumina and reported record production at Brazil Alumina. In response to lower manganese prices at South Africa Manganese, the company reduced the use of higher-cost trucking. For the half-year period, the company declared a fully franked interim dividend of US$54 million and saw a US$180 million increase to its capital management program, demonstrating the company’s strong financial position, a track record of returning excess capital to shareholders and positive outlook for its business. The company ended the half-year period with a net cash balance of US$277 million.

H1FY20 Results (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 33.0%. Schroder Investment Management Ltd. and Vanguard Investments Australia Ltd. hold the maximum interest in the company at 10% and 6.07%, respectively.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick Look at Key Margins: For H1FY20, the company’s EBITDA margin stood at 18%, higher than the EBITDA margin of H2FY19. The company has a current ratio of 2.03x, higher than the industry median of 1.81x, demonstrating that the company is well equipped to pay its short-term obligations. The company has a debt to equity ratio of 0.11x, lower than the industry median of 0.21x.

Key Ratios Metrics (Source: Refinitiv, Thomson Reuters)

Mineral Resource Estimate Declaration: On 12 May 2020, the company reported a Mineral Resource estimate for the Clark Deposit which forms part of its 100% owned Hermosa Project located in Arizona, USA. This deposit provides the company an additional option to realise longer-term value from within the broader land package.

Covid-19 Update: In response to Covid-19, the company has implemented several measures to keep its people safe and well and to maintain reliable operations. In order to maintain the financial strength of its business during the current period, the company has lowered its FY20 sustaining capital expenditure guidance and has suspended the remaining US$121 million of its current on-market share buy-back program.

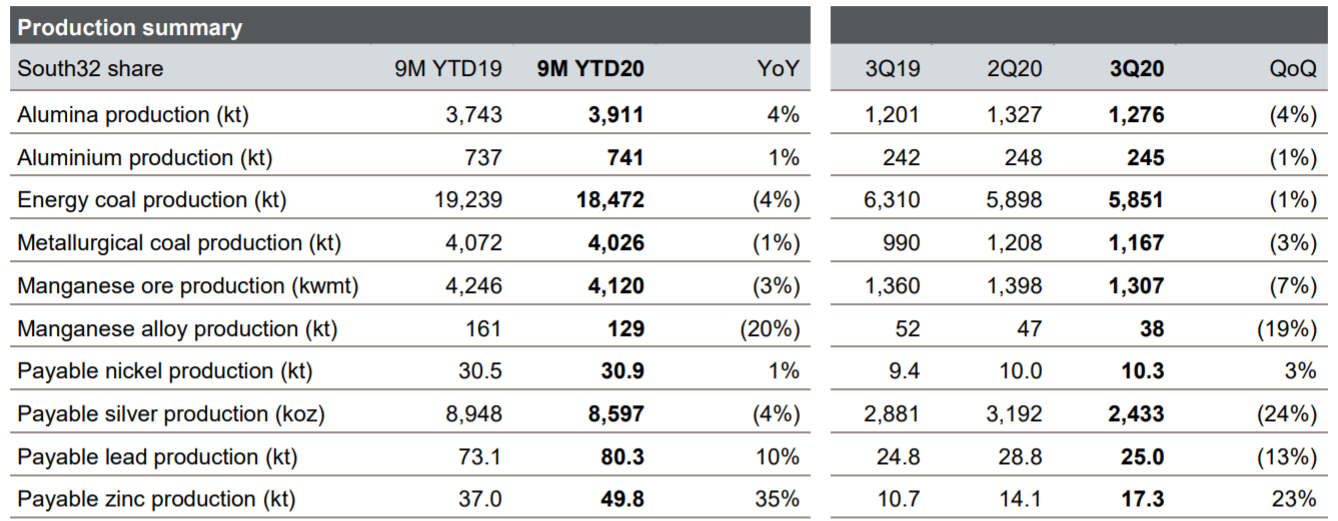

March Quarter Update: Despite the market volatility during the March quarter, the company progressed on its strategy of reshaping and improving its portfolio. Over the period, the company maintained the momentum at Hermosa, formed the Ambler Metals Joint Venture and progressed with the sale of South Africa Energy Coal.

In order to protect its strong financial position, the company took several important steps during the quarter which include suspending its on-market share buyback; reducing capital and exploration expenditure and initiating a group-wide review aimed at delivering a reduction in controllable costs. In terms of operations, the company delivered a strong operating result on the year to date basis, highlighted by record production at Brazil Alumina and Hillside Aluminium.

March Quarter Production Summary (Source: Company Reports)

What to expect: Moving ahead, the company intends to include industry-leading positions in alumina and manganese and will continue to embed development options with a bias to base metals that have the potential to deliver meaningful growth in shareholder value. The company continues to reshape as well as improve its portfolio, evident from its recent achievements which include forming the Ambler Metals Joint Venture, maintaining momentum at Hermosa, and progressing the sale of South Africa Energy Coal.

Due to the uncertainty caused by Covid-19 and associated restrictions aimed at containing the spread of COVID-19, the company has suspended its guidance for its operations in South Africa and Colombia and lowered FY20 production guidance at Australia Manganese by 5%. For the rest of its operations, the company has maintained its FY20 guidance.

Key Risks: Right now, the FY20 results of the company’s various operations are subject to the impact from existing or additional COVID-19 restrictions or measures during the remainder FY20. Further, the company is also exposed to the risk of disruption of any one commodity, geography or operation. The company’s operations and transport networks can be disrupted by events such as fire, explosion, flooding, loss of power supply, etc. The company uses a strong system of risk management in design, construction and operation phases, to analyse risks and design plans that prevent or limit business impacts.

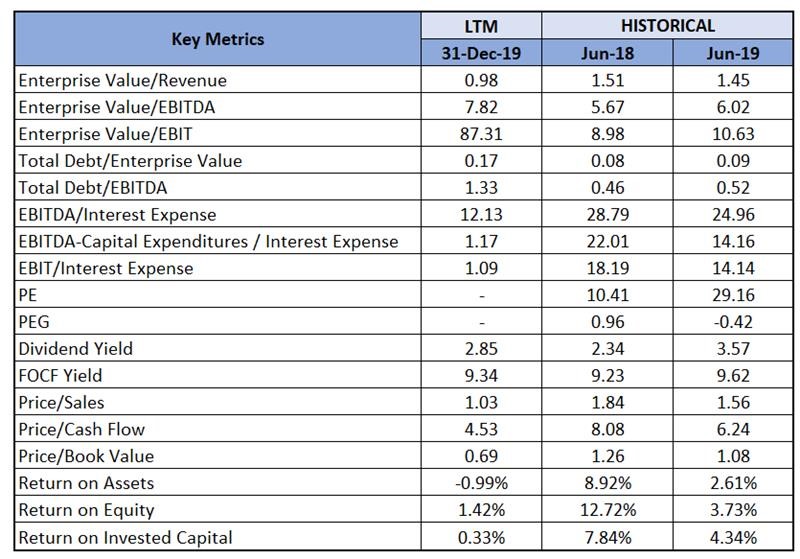

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

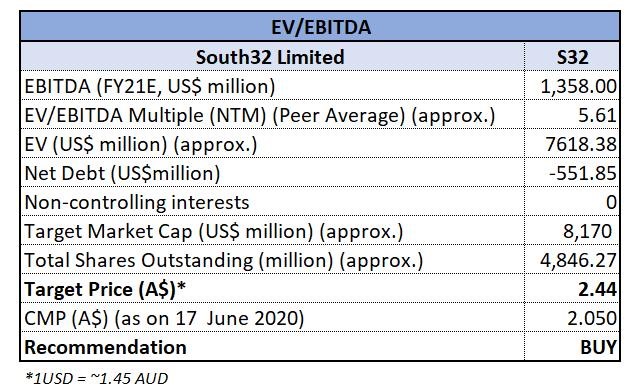

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of S32 has corrected by 29.11% on ASX and is inclined towards 52-weeks low price, offering investors a decent opportunity for accumulation. The company’s strong financial position and a resilient portfolio have placed it well to navigate and respond to COVID-19’s impact. We have valued the stock using an EV/EBITDA multiple based illustrative relative valuation method and have arrived at a target price with a low double-digit upside. For the purpose, we have taken peers like OZ Minerals Ltd (ASX: OZL), IGO Ltd (ASX: IGO) and, Mineral Resources Ltd (ASX: MIN). Considering the aforesaid facts, the company’s resilient portfolio, recently taken initiatives to strengthen the company’s financial strength, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $2.050, down by 0.485% on 17 June 2020..jpg)

S32 Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...