Company Overview -

Stockland Corporation Limited is an Australia-based property company. The Company develops, owns and manages retail centers, business parks, logistics centers, office buildings, residential communities and retirement living villages. It operates through four segments: Residential, which delivers a range of master planned and mixed use residential communities in growth areas; Retirement Living, which is engaged in the design, development and management of communities for retirees; Commercial Property, which invests in, develops and manages retail, office, logistic and business park properties, and Other, which includes its other assets in the United Kingdom, former apartments and aged care businesses and other operations. It has residential properties in areas, such as New South Wales, Queensland, Victoria and Western Australia and retirement living communities in areas, including New South Wales, Southern Australia and Victoria. It also owns shopping centers in Australia.

.png)

SGP Dividend Details

First quarter of 2016 highlights:

Stockland Corporation Ltd (ASX: SGP) reported a decent performance in the first quarter of 2016 across all of its segments with its total retail sales segment improving by 1.9% (comparable growth) as compared to the first quarter of 2015, driven by 5.8% year on year (yoy) and 2.8% yoy increase of Mini-Majors & Other as well as specialties segments respectively. Retail segment delivered a solid MAT growth of 4.2% on a yoy basis driven by communication technology, food catering, retail services and homewares segments. The group is finishing its Wetherill Park project before schedule and opening a fully leased Point Cook. Harrisdale, WA stage one development is expected to open by second half of 2016 while Glasshouse H&M flagship store opened before the schedule. Stockland is also factoring the rapidly changing retail trends in its centers by focusing on Entertainment like cinemas, restaurants, fast casual dining, bars and bowling. Food and dining themes have surged to 175 outlets in the group’s centers. As per the Logistics & Business Parks segment highlights, SGP witnessed around 176,000 square meters (sqm) of leasing activity during the quarter while it enhanced portfolio occupancy by a further 62,000 sqm leasing from the first quarter. SGP also acquired Wonderland Drive, Sydney for $34 million, 8% initial yield which is a 4.3 hectare site. The site work started at 10,702 sqm pre-committed facility at Oakleigh (Vic), which is estimated to finish by May 2016 with an incremental internal rate of return (IRR). The group also finished the sale of its 50% interest in Waterfront Place and Eagle St Pier for $ 317.5 million which delivered a cash IRR of 14.3% on the Tower from its acquisition in 2004. SGP also made NSW acquisitions at Botany and Warwick Farm, which has yields of over 7.6%. The group also has an active development pipeline of over $350 million for its Logistics & Business Parks segment.

.png)

Highlights (Source: Company Reports)

Solid commercial property portfolio:

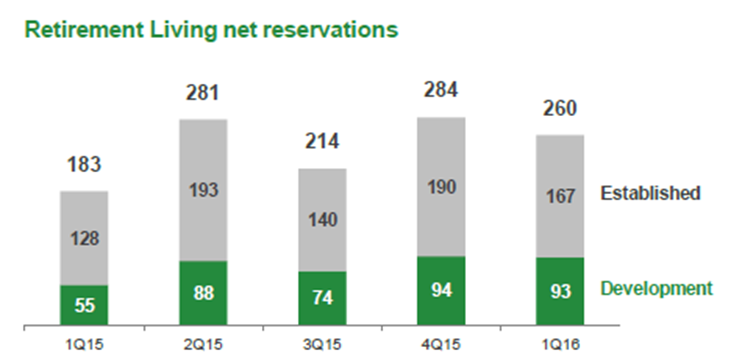

Stockland revalued its commercial property portfolio for the first quarter of 2016 and the preliminary results of these revaluations showed an increase of over $430 million (over 5 %) in the combined value of their assets. This strong results indicate the solid recurring income from its Commercial Property portfolio driven by strong Residential business and Retirement Living performance. The revaluations indicated a rental growth as well as a tightening of its portfolio’s weighted average capitalization rate to 6.5% as of December 2015 as compared to 6.9% as at June 2015. With regards to the Retirement living segment performance during the first quarter of 2016, Retirement Living net reservations improved to 260 during the quarter from 183 in prior corresponding period (pcp), as the group’s sales efforts were paid off. Cardinal Freeman project at NSW is on track to finish first two buildings by April 2016, and already witnessed around 85% of reservations. New village at Willowdale (NSW) has started development and is estimated to be launched by second quarter of 2016. SGP also acquired South Australian villages and forecasts to start construction of 33 homes at Lightsview. However, the first half of 2016 profit is expected to be impacted by timing of the settlements having a major skew towards second half of 2016. Meanwhile, SGP’s Residential sales generated strong performance and delivered more 1,557 net deposits during the first quarter of 2016. First quarter of 2016 deposits coupled with deposits by FY15 ending led to an overall of 5,299 wherein most of these deposits would settle by fiscal year of 2016 and FY17.

Retirement Living net reservations (Source: Company Reports)

Generating value projects by focusing on residential segment:

The group forecasts to generate an underlying earnings per security growth in the range of 6% to 7.5% for fiscal year of 2016. Funds from operations (FFO) per security growth is expected to be in the range of 8.5% to 10% for the year, based on the market conditions. SGP expects to deliver over 6000 residential settlements by fiscal year of 2016. The group estimates its Commercial Property comparable FFO growth in the range of 3% to 4% and a comparable NOI growth in the range of 2% to 3%. Management reported that their active residential projects are positioned in low supply corridors with decent demand and forecasts a moderate growth in Sydney and inner Melbourne markets. Brisbane and Melbourne growth corridors are showing improvements while growth at Perth slowed as expected. SGP estimates its new projects to contribute for its operating profit margins of around 14%. The group launched two residential projects during 1Q16 and received a favorable response from clients. Aura got around 900 leads from its launch last year while SGP’s Arve, a medium density project, at Ivanhoe Melbourne is 80% are pre-sold. The group recently reported that it estimates a distribution of 12.20 cents per ordinary Stapled Security during the six months ended on December 2015 and is on track to achieve its distribution guidance of 24.5 cents per security for FY16.

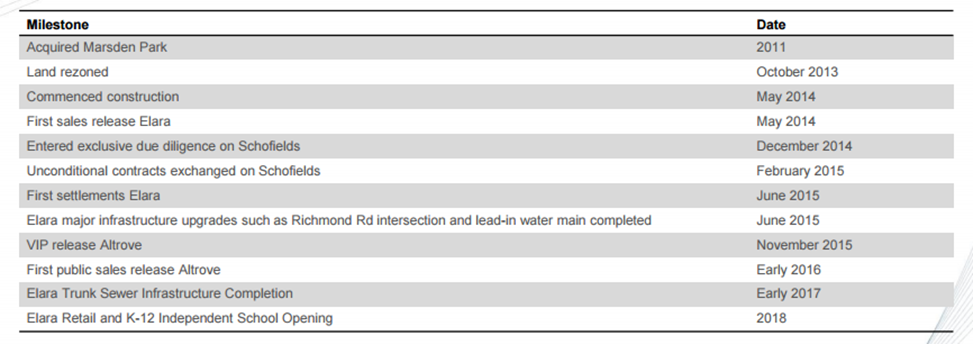

Leverage positive NSW Outlook: Stockland Corporation Elara and Altrove projects are well positioned to leverage the improving NSW market going forward. NSW economy (Gross State Product) is anticipated to increase by 2.1% during 2015-16, and by 2.5% per annum through to 2018- 2019. NSW is also planning to spend over 69 billion for infrastructure in the next four years. In the metro Sydney, rezoning of land in North West and South West is ongoing. Based on the NSW Department of Planning estimates with regards to Metro Sydney, over 664k new dwellings are estimated to be through by 2031 driven by urban renewal as well as Greenfield. Altrove project received a solid demand from over 12,000 leads and received a high proportion of FHB enquiry of 40%. Most of the house and land budgets are in the range of $550 to $800K. Altrove project is situated near the Schofields area and is positioned to leverage growing areas like Residential and Retirement segments.

Stockland’s current and past projects in NSW (Source: Company Reports)

Stock Performance:

The shares of Stockland corrected over 3.8% (as of January 22, 2016) in the last six months as investors were concerned over the group’s growth track on the back of challenging economic conditions. SGP delivered a decent first quarter of 2016 performance and is on track to achieve its FY16 guidance. The group has a strong commercial portfolio and is focusing on the growth areas in its residential as well as retirement living portfolio. Meanwhile, the group also recently undertook a $377 million renovation and expansion of its Green Hills Shopping Centre located at the East Maitland in the Lower Hunter Valley of New South Wales. The group would double the size of the center to over 70,000 square meters of Gross Lettable Area (GLA) with estimated redevelopment by mid-2018 as compared to the current under 33,000 square meters of GLA. The group is seeking to add 141 additional specialty stores in Stockland Green Hills leading to an overall number of specialties to more than 225 stores as well as intends to enhance the center’s present mini-majors. With this redevelopment contract, SGP would generate an incremental IRR of greater than 12% in the ten years after finishing while expects an incremental, stabilized FFO yield of around 7%. Moreover, SGP’s positive commercial portfolio update indicates its solid portfolio of assets. SGP stock recovered over 3.3% in the last three months (as of January 22, 2016) and we may see positive momentum going forward. The stock is also trading at attractive valuations with a reasonable P/E and has a decent dividend yield. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $4.08

SGP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...