Kalkine has a fully transformed New Avatar.

Company Overview: The Citadel Group Limited is engaged in the development and delivery of technology and education solutions to federal and state government departments and the private sector. The Company's principal activities consist of professional and managed services provision in the technology and education sectors throughout Australia. Its segments include Technology, which sells professional and managed services to government agencies and private enterprises; Education, which focuses on the delivery of a range of nationally-accredited business qualifications (including Advanced Diploma level) that enable students to articulate into second year university or to gain practical skills for employment, and Other, which includes corporate assets, such as investments in subsidiaries. The Company is engaged in providing vocational education, and training and supporting technology applications to empower learners (typically 17-24 years old) to achieve their individual education or employment goals.

.png)

CGL Details

CGL Reports Expansion in SaaS Revenue: The Citadel Group Limited (ASX: CGL) is a technology company engaged in the provision of software and services, product sales and installation, and consulting and professional services across Australia. The company’s offerings are divided among three key segments – Knowledge, Health and Technology. In FY19, the company invested in building the required capabilities to execute its Citadel 2.0 strategy. As guided by the company, the strategy is aimed at continued investment for the development and distribution of products with large addressable markets. The company has reported continued progress against the strategy, in the form of an increase in the size of SaaS business, multiple contract wins, and a significant pipeline of opportunities as Citadel 2.0 products gain traction. Growth in the SaaS business has been a key highlight of the year. During FY19, the company has made significant efforts to enhance its software and platform capabilities. The return on investments made for developing the platform capabilities was evident in the success of the Citadel-IX offering, which reported revenue growth of 157% from FY18. Moreover, the company also entered into new contracts for the product, taking the total number of contracts for Citadel-IX to 12. However, FY19 experienced a financial slowdown due to delay in customer-controlled project extensions that were moved into H1FY20, partly due to the Federal Government election, and softer results in the last quarter of the year as compared to the previous years. During the year, the company executed two acquisitions namely, Gruden and Noventus, strengthening its offerings in the Government, Defence and National Security verticals.

To reiterate, the company has been progressing well on its Citadel 2.0 strategy and expects to deliver better results in the coming financial year. It has reported an increase in the share of revenue from the SaaS business. In FY19, SaaS revenue comprised of 35% of the segment revenue, as compared to 26% in the prior corresponding year. Over a period of three years covering FY16-FY19, SaaS revenue from continuing operations has reported a CAGR of 144%, with continuous upward movement. Looking at the current business scenario, the trend is expected to be continued as the company confides in the investments made on developing its capabilities during FY19..png)

Growth in SaaS Revenue (Source: Company Reports)

In the light of the above developments, the company has provided for FY20 guidance of low double-digit organic revenue growth, pre Noventus margins to be in-line with FY19, and a positive revenue and EBITDA contribution from Noventus, amounting to $18 million and $2 million, respectively. Moreover, the company’s commitment towards reshaping the business through the Ciitadel 2.0 strategy truly holds the potential to boost revenue growth and drive financial security for its investors.

Q1FY20 Update: During the quarter ended 30th September 2019, the company reported a set of contract wins and developments across its three key segments. In the Knowledge segment, the company sold ~8,600 new software licenses with a total contract value of $2 million recurring annual revenue. The company began with business intelligence and analytics work on the Austender platform for Government procurement and expects to receive further work orders within H1FY20. Developments in the Health segment included 2 new sites won at Ramsay Healthcare and CGL becoming the preferred supplier for Melbourne Genomics Health Alliance. In the Technology segment, the company notified about a new deal with the Department of Veterans Affairs, commenced work with two new clients for multiple facilities, and also reported progress on the customer-controlled project extensions delayed from FY19.

FY19 Financial Highlights: During the year ended 30th June 2019, the company reported revenue amounting to $99.2 million, down 6.9% on prior corresponding year. However, revenue for the period met the guidance issued for revenue in the range of $97 million - $104 million. SaaS revenue for the year went up by 23% year over year, as a result of investments made for the development of secure cloud-based software solutions. For instance, the company invested significantly on the security of the Citadel-IX platform. In addition, the period saw continued development and product enhancement initiatives that will benefit the company, going forward..png)

FY19 Financial Performance (Source: Company Reports)

In FY20, the company is aiming for growth across all its operating segments with a continued focus on the recurring revenue model. Through continued innovation on the SaaS platform, the company is unlocking its true potential for growth. With the progress in Citadel 2.0 strategy, it has built a significant pipeline of opportunities across key product offerings. Furthermore, significant contract wins from FY19 to date have added to future revenue streams and increased the credibility of the business.

Recent Update on Health Contract: As per an announcement released on 13th December 2019, the company notified the market that it has signed an extension for its Auslab™ system to operate for Queensland Health through to 2029. The company will provide Queensland Health with access to its laboratory information system capability until at least 1st January 2023. To provide the latest capability, the company will also be delivering an update to Auslab™ Evolution for further benefits.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 64.06% of the total shareholding. Jakeman Holding Co Pty. Ltd. holds the maximum number of shares with a percentage holding of 13.67%, followed by Mcconnell (Mark) with a holding of 12.30%.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

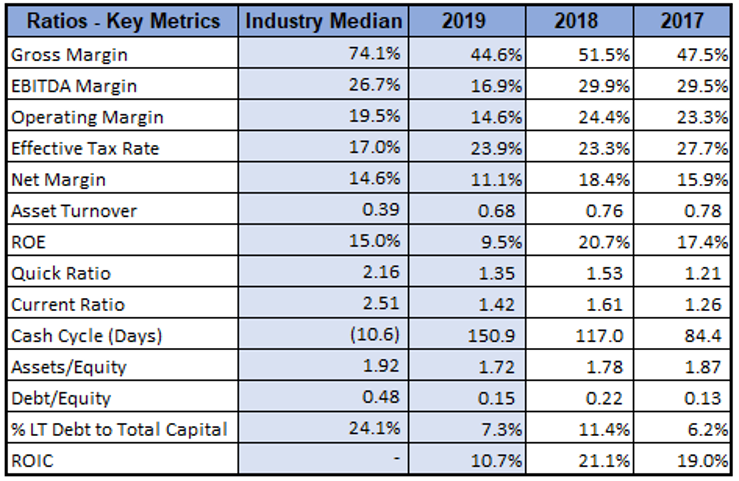

Key Metrics: In FY19, the company reported a gross margin of 44.6%, lower than FY18 gross margin of 51.5%. This came in as a result of the delayed customer-controlled extensions and lower customer spend in Q4. Despite the above result, the company is optimistic about business growth, looking at the potential contribution to gross margin from SaaS offerings like Citadel-IX. Currently, the product is growing with a gross margin of 30-40%, which is expected to improve over time. Debt levels for FY19 also stood at decent levels, with a debt-to-equity multiple of 0.15x, lower than the industry median of 0.48x and the prior corresponding year multiple of 0.22x. Current ratio of the company stood at 1.42x in FY19.

Key Metrics (Source: Thomson Reuters)

Outlook: The company is progressing on SaaS acquisitions in the eHealth sector and expects to execute one acquisition in the near-term. Moreover, in Q2FY20 and beyond, it is looking forward to a contribution from the recently confirmed contracts in the Government, Defence and Tertiary Education sectors. As the company delivered on its expectations for Q1FY20, it has reaffirmed the guidance issued for FY20. Revenue for FY20 is expected to return to growth, precisely a low double-digit organic revenue growth on FY19. Integration of Noventus is expected to deliver $18 million in revenue and $2 million in EBITDA, with pre-Noventus margins remaining consistent with FY19..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/EBITDA Multiple Approach.png)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company generated positive returns of 56.07% over a period of 3 months. Currently, the stock is trading below the average of its 52-weeks trading range of $2.940 - $8.900. On the face, the company’s performance in FY19 may seem subdued due to the fall in revenue and margins. However, a holistic view of the numerous initiatives by the company during FY19 and Q1FY20, provides a clear picture of how the business is heading towards growth. The company has executed various contracts that will support revenue growth in the coming years. Moreover, it reported a confirmation to the contracts that were earlier deferred and expects a contribution from the same in Q2FY20 and beyond. As per the management, the business is well funded to make further investments for product enhancements and new technological capabilities. As a result of continued commitment to guidance and favourable performance in Q1FY20, CGL reaffirmed the FY20 guidance and expects its revenues to return to growth. The contract extension with Queensland Health signifies the company’s commitment to its clients and will build a greater sense of confidence among other long-standing relationships of CGL. We have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). Considering the key business developments during FY19 and beyond, continued progress on Citadel 2.0 strategy, expected contribution from acquisitions and contracts, product development initiatives, and anticipated growth in the SaaS business, we give a “Buy” recommendation on the stock at the current market price of $4.790, up 0.63% on 31st January 2020.

CGL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...