Company Overview - Tiger Resources Limited (Tiger) is engaged in mineral exploration, development, mining and sale of copper concentrate. The Kipoi Copper Project (KCP) is located approximately 75 kilometers NNW of Lubumbashi in the Katanga Province of the Democratic Republic of Congo. Tiger has a 60% interest in the Kipoi project. The remaining 40% interest is held by La Generale des Carriere et des Mines. The Lupoto Permit is located approximately 10 kilometers south of the Kipoi Project. The Company owns a 100% interest in the Lupoto Copper Project. The Company has a six-month option agreement to conduct initial exploration activities on approximately 27square kilometers La Patience PR-10715, located at approximately 10kilometers south-east of Kipoi.

Analysis – Tiger is a recently established African copper producer with the company’s key asset being its 60% interest in the Kipoi copper project. Kipopi copper project produced 43.5kt of copper in 2013 from a Heavy Media Separation (HMS) plant at a cash cost of US$0.61/lb. Tiger is developing the Kipoi project in sequential stages and is currently in a late stage of development that will see the HMS plant replaced with a phase 1 SX-EW plant. In our view the staged development of the KPC has smoothed the capital spend over a manageable period however funding uncertainties and the DRC location may have kept investors on the sidelines. Operating in the DRC does not come without political instability and expropriation risk. Potential changes to the mining code may be forthcoming but we take comfort that the Kipoi mine is already owned by a state backed mining company.

Tiger share price performance (Source - Company Reports)

Tiger share price performance (Source - Company Reports)

We believe the investor appetite in copper is starting to slowly rebuild. With some other Australian copper plays hindered by short mine lives we believe TGS’s 11 year mine life and low cost profile compensates for the country risk. Increased mined life is an opportunity. Growth to mine life could come from the following sources :- 1) Increased Recovery – The recovery rate of a heap leach is susceptible to variation and overcall. Successful leaching of the pads could result in a higher grade pregnant liquor that feeds the SX-EW plant. 2) Increased resource to reserve conversion – The current Kipoi reserves account for circa 70% of the overall resource base. Should the copper price rally over the coming years a higher copper price assumption could lead to increased resource to reserve conversion thereby extending the mine life. 3) New resources & reserves – Ongoing drilling of existing pits and exploration targets provides a modest potential for the addition of new resource and reserves. However with a established mine life of around 10 years extending mine life through the addition of new ore is unlikely to be a key priority.

Copper production in DRC (Source - Company Reports)

Copper production in DRC (Source - Company Reports)

Tiger’s present focus is the development of a 50ktpa SX-EW copper project to replace the previous HMS plant. While rewarding shareholders with eventual dividends will likely be a desired outcome, we believe TGS could look to embark on a regional consolidation strategy that will look to set up Kipoi as a copper producing hub. Given the technical and financial challenges in building an SX-EW plant which TGS has largely overcome we see TGS looking to extend mine life through local/regional exploration and also potentially through the acquisition of regional oxide projects to provide feed to Kipoi longer term.

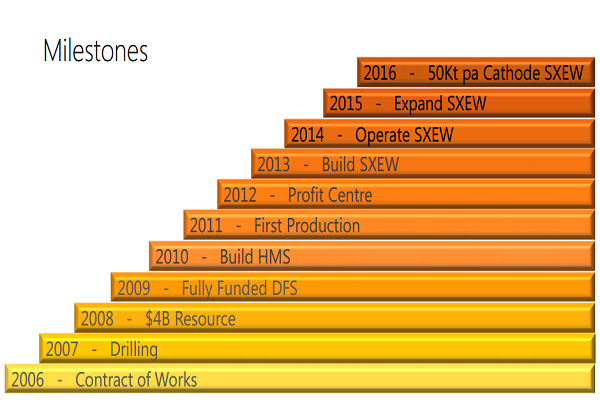

Construction & Production Milestones (Source - Company Reports)

Construction & Production Milestones (Source - Company Reports)

Tiger resources announced in May that it has commenced copper cathode production from its 60% owned Kipoi project in the Democratic Republic of Congo. First cathode was produced on 25

th May after the completion of the stage 2 SX-EW plant. The company expects the 25ktpa capacity SX-EW plant to reach full production within 3 months and is targeting output of 12kt in CY14. The company also continues to produce a copper concentrate from its stage 1 heavy media separation (HMS) plant and is targeting 39kt of product in calendar year 2014 for a total of 51kt.

Pregnant liquor pond containing high grade copper (Source - Company Reports)

Pregnant liquor pond containing high grade copper (Source - Company Reports)

After the weaker than expected March period a number of investors had expressed concerns over the balance sheet liquidity of Tiger. We believe that the unchanged guidance for the HMS output suggested that the weak March period should not be repeated. Tiger has continually added to its reserve and resource base over the past two years which now stands at nearly 1Mt of contained copper in all categories nearly twice the existing reserve.

Interior of the solvent extraction module (Source - Company Reports)

Interior of the solvent extraction module (Source - Company Reports)

Tiger’s project team completed Stage 1 at Kipoi in 2011 and commissioned stage 2 in 2014 on time and on budget and the project has infrastructure in place. We expect Stage 2 SX-EW expansion to grow production to 50,000tpa by 2016 at bottom quartile cash costs. The current 10 year mine life does not include over 20Mt of known resources or potential from several targets near the existing mine site and we think it is likely that additional exploration will significantly extend the mine life. While the discount in Tiger’s shares includes some systemic risk due to DRC country risk, we see significant potential upside for the shares as the company executes on its stage 2 Expansion.

Cathode stripping machine (Source - Company Reports)

Cathode stripping machine (Source - Company Reports)

TGS last month raised A$20m via an institutional placement at $0.34/share. In addition to the placement TGS has also signed a non-binding term sheet to extend its offtake prepayment facility from US$50m to US$75m. We expect the repayment terms of this facility are likely to have also been extended which if drawn provide TGS with an extremely strong working capital buffer. TGS has stated it intends to use $21m of the proceeds to accelerate the implementation of several discretionary items associated with the phase 2 of the expansion to 50ktpa of copper cathode. We are disappointed TGS has chosen to raise equity to accelerate this expenditure by only a couple of months.TGS will also use the funds to provide a loan of US$10m to its 60% subsidiary La Société d'Exploitation de Kipoi SPRL (SEK), the loan is expected to provide SEK with sufficient funding to purchase the DRC government’s right to a 5% stake in the Kipoi project pursuant to the mining code. The balance of funds raised will provide TGS with additional working capital.

TGS Daily Chart (Source - Thomson Reuters)

TGS Daily Chart (Source - Thomson Reuters)

TGS has achieved a significant milestone with the commencement of cathode production. Whilst the commissioning phase of any project is a volatile period we remain positive on TGS and put a BUY recommendation on the stock at the current price of $0.34.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...