Kalkine has a fully transformed New Avatar.

Company Overview: Webjet Limited is engaged in the provision of online travel booking. The Company is engaged in digital travel business providing services in regional consumer markets, as well as global wholesale markets via the online channel. It operates through the segments, including Business to Consumer Travel (B2C Travel) and Business to Business Travel (B2B Travel). The Company's B2C division consists of Webjet and online republic brands. Its B2B division consists of Lots of Hotels and Sunhotels brands. Lots of Hotels brand operates in approximately 25 markets, providing coverage across the Middle East and Africa. Sunhotels brand has over 6,000 directly contracted hotels. It offers its services through the Website, www.webjet.com.au. Its products include cheap flights, hotels, holiday packages, car hire, cruises, exclusives, and travel insurance. It offers cruises, such as P&O Cruises, Princess Cruises, Carnival Cruises, Royal Caribbean Cruises, Celebrity Cruises and Norwegian Cruise Line.

.png)

WEB Details

Solid Performance in 1H FY 19 Amidst European Concerns: Webjet Limited (ASX: WEB) is a small-to-mid-cap company with the market capitalisation of ~$1.97 Bn as of April 01, 2019. It is principally engaged in the provision of online travel bookings with the help of its B2C and B2B divisions. The company had released its 1H FY19 results wherein it generated a total transaction value of $1.9 billion reflecting a YoY rise of 29% and demonstrating a 2% rise in B2C and 65% rise in B2B. The growth in B2B for 1H FY 2019 included six months contribution of Jac Travel as compared to 4 months in prior corresponding period (or PCP). However, after adjusting the acquisitions’ impact, organic growth stood at 21% even though there was softness in bookings because of the hot European summer. The company’s revenue from ordinary activities (post cost of sales) witnessed a rise of 33% and stood at $175.3 million and net profit after tax (NPAT) rose by 61% and stood at $38.3 million (before acquisition amortisation). Despite the uncertainty surrounding the Brexit and soften demand for beach inventory due to record hot 2018 European Summer, WebBeds generated EBITDA which was more than double on YoY basis i.e. from $12.8 million in 1H FY 2018 to $30.1 million in 1H FY 2019. It was mainly driven by the robust growth in the key European and Middle East markets and meaningful EBITDA witnessed from the Americas. In 1H FY 2019, WebBeds business was known as WEB’s largest business unit because of robust EBITDA generation. The company had made announcement that Mr. Zi Mtenje had been placed on the designation of Company Secretary.

In a nutshell, we expect that Webjet Limited would be aided by its stable cash & equivalents, strong historical trend for dividend pay outs and acquisitions. Also, the company is possessing strong cash-generation capabilities which might help it further improving its liquidity position. Webjet had made deployments to help increase global scale, have stronger governance as well as other corporate overheads and, we expect, that deployments might payoff well in years to come and, as a result, the company can target long-term growth opportunities.

.png)

Strong 1H FY 2019 Results (Source: Company Reports)

Significant YoY Improvement in Key Margins: Webjet Limited witnessed significant YoY improvement in its key margins in 1H FY 2019 as is evident from its net margins which rose 9.9% YoY and stood at 15.1% reflecting the company’s capability to convert its top line into the bottom line. Also, WEB’s operating margin stood at 18.1% reflecting a rise of 11.4% on YoY basis which reflects that the company’s cost-effective strategies are paying off well. Moreover, the company has a decent balance sheet position with current ratio of 0.99x and debt to equity ratio of 0.33x in 1HFY19.

Management View on 1HFY19 Results: With respect to 1H FY 2019 results, WEB’s Managing Director named Mr. John Guscic reflected favourable views and he also highlighted the robust momentum witnessed by WebBeds business. He also threw light on the acquisitions of JacTravel and Destinations of the World (or DOTW) which have supported WebBeds business in terms of increasing global size and scale. Also, the management added that Webjet OTA (or online travel agency) has been gaining the market share even though there was a slowdown in domestic flights market and, because of the company’s strategy to focus towards the profitable bookings in Online Republic, there was an improvement in TTV and EBITDA margins.

Robust organic growth in Europe Aided WebBeds Business: In 1H FY 2019, the WebBeds business witnessed significant growth in all the regions. Europe also witnessed robust organic growth even though there was the presence of uncertainty with respect to Brexit and there was hot 2018 European summer which reduced demand for beach inventory. Also, the Asia-Pacific has been demonstrating robust growth across both customers and direct contracts. The company stated that DOTW integration is ongoing and is tracking ahead of plan. We expect that the company’s WebBeds business would continue to drive growth moving forward on the back of acquisitions which might support the overall company. The company’s management stated that there are numerous global growth opportunities for WebBeds, primarily in Asia-Pacific region.

.png)

1H FY 2019 Metrics of WebBeds Business (Source: Company Reports)

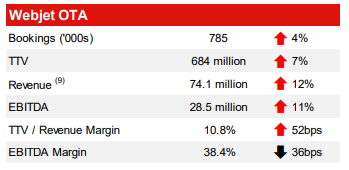

Market Share Growth Witnessed in Webjet OTA: During 1HFY19, there has been growth in the market share of Webjet OTA and the flight bookings witnessed the rise at around 3 times the market. An increase in OTA’s size and scale have been delivering value to airlines and other partners and there was an improvement in TTV margins across flights and ancillary products. Also, the EBITDA margins are more than 38% (as shown below). Moving forward in FY 2019, with respect to Webjet OTA, the company is targeting bookings growth of 3 times the market.

1H FY 2019 Metrics of Webjet OTA (Source: Company Reports)

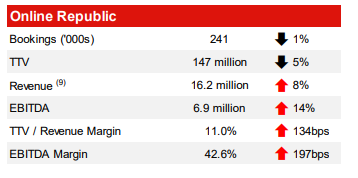

Decent Online Republic’s Performance in 1H FY 2019: The improvement in Online Republic’s 1H FY19 result reflects the strategy to focus towards the profitable bookings. The decline in acquisition costs along with lesser operating cost structure has led to the improvement in EBITDA margins. The significant performance was witnessed in Motorhomes and Cruise had underperformed in line with reduction with respect to capacity supply. The improvement in the TTV margins demonstrate the focus towards higher margin and profitable bookings and, we expect, that this would continue to support the business. With respect to Car Hire, the growth in bookings was flat which was in line with the global car rental market. However, Australian and New Zealand markets have outperformed.

1H FY 2019 Metrics for Online Republic (Source: Company Reports)

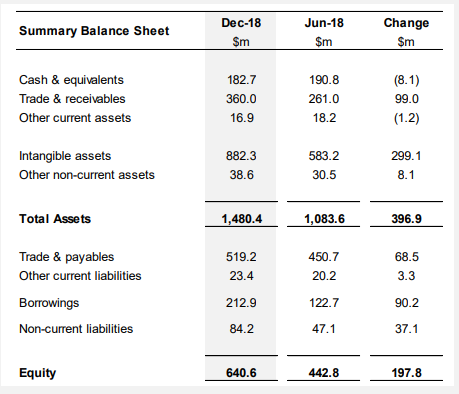

Stability in Cash & Equivalents: Webjet’s cash and equivalents have remained stable, as at the end of December 2018, they were maintaining $182.7 million which also includes $23.2 million of client funds. We expect that the decent position of WEB’s cash and equivalents would continue to support the company’s long-term growth objectives and further places it to tap growth opportunities. Also, the results for 1H FY 2019 demonstrates improvement in working capital management. We expect that the deployments made by WEB to support business activities might help it in tapping the growth opportunities moving forward.

Summary Balance Sheet as at December 2018 (Source: Company Reports)

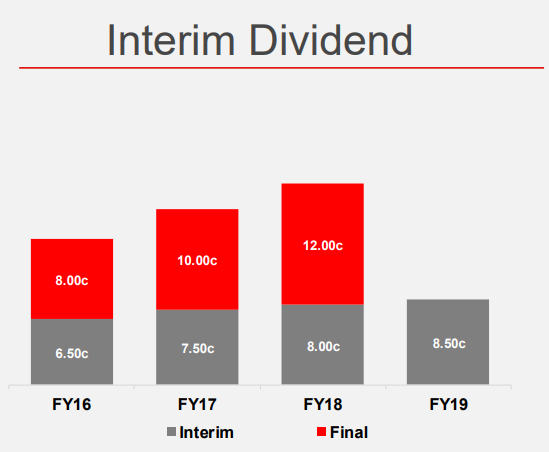

Decent Track Record of Dividends Ensures Decent Fundamentals: Webjet has been declaring dividends at a decent pace over the past few years which reflects decent fundamentals amidst a challenging environment. In 1H FY 2019, the company declared interim dividend amounting to 8.5 cents (fully franked) while, in the same period of the previous year, it was 8.00 cents per share. Therefore, we expect, that a decent declaration of dividends would attract attention of the market players.

Dividends (Source: Company Reports)

What to Expect from Webjet Moving Forward: Webjet Limited had reconfirmed the FY19 guidance and they happen to be on track to deliver at least $120 million EBITDA (excluding one-offs which are associated with DOTW acquisition). With respect to WebBeds, the company has been targeting bookings growth of over 5 times the underlying market in all markets. The early indications had reflected robust rebound for European summer bookings in FY 2020. With respect to Webjet OTA, the company is anticipating that TTV and bookings growth for 2H FY 2019 would be similar to 1H FY 2019.

Apart from these factors, we expect that the company’s stable cash & equivalents would continue to support its liquidity levels and might also further prepare to tackle the challenges. Also, in FY 2019, the company is expected to incur corporate costs amounting to around $15 million which includes option costs, D&O insurance as well as other costs which are associated with supporting the growing global business.

Stock Recommendation: The stock of Webjet Limited has managed to deliver decent returns as, in the span of previous three months, the stock delivered 32.51% return and, on the YTD basis, the stock posted 37.39% return. Also, as a result of decent fundamentals and balance sheet position, the company’s annual dividend yield stood at respectable levels of 1.86% as at 31 December 2018. Also, we expect that the acquisitions done by the company would continue to support its WebBeds business.

Therefore, it can be said that the company’s financials have witnessed a substantial improvement from the past five years as its top-line and bottom-line have witnessed CAGR of ~67.31% and ~21.41%, respectively in the period from FY 2014-FY 2018. We expect that strong performance would continue to attract the attention of the market players. The company has been able to generate respectable RoE of 4.7% in 1H FY 2019 which indicates that it has been delivering decent returns to its shareholders. Given the backdrop of aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of A$14.560 per share.

WEB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...