Company Overview - Western Areas Limited is an Australia-based producer of nickel. It is engaged in mining, processing and sale of nickel sulphide concentrate, the continued assessment of the feasibility and development of nickel mines and the exploration for nickel sulphides, other base metals and platinum group metals. It operates the Forrestania project, which consists of Flying Fox and Spotted Quoll nickel mines and the Cosmic Boy Concentrator, which treats the high grade ore and produces nickel concentrate for sale. Its project portfolio includes Carbon Disclosure Project, Mt Gibb Project (joint venture with Great Western Exploration Limited), Lake King Joint Venture and Musgrave Nickel-Copper Joint Venture. The Company’s subsidiaries include Western Platinum NL, Australian Nickel Investments Pty Ltd, Bioheap Ltd and Western Areas Nickel Pty Ltd.

.png)

WSA Dividend Details

Positive Exploration activity results: Western Areas Ltd (ASX: WSA) has been delivering positive exploration results with its Western Gawler Project in South Australia achieving another major earn-in milestone. The project is a farm-in and joint venture agreement with Strandline Resources and Monax Mining. Based on the agreements, Western Areas indicated the potential to acquire up to a 90% interest in major holdings of key contiguous tenements within the Project region. WSA completed 90% earn into Monax. The drilling efforts are ongoing in the region and over 50 further holes were planned to be drilled on the Western Gawler Project during the December quarter. Drilling at the Strandline ground have started while the test geophysical surveys are under progress. Meanwhile, all the three of Monax’s projects are showing promising exploration results and Mt Ringwood Gold Project low-cost exploration is being supported by third parties on the Western Gawler Craton and Phar Lap Projects. As a result, WSA is focusing to make Monax into a major gold project. The initial rock chip results taken from the Mt Ringwood Gold Project indicated positive results. Accordingly, the group is focusing to finish further field work on the highly prospective and vastly underexplored terrain and has also started field mapping and surface sampling on its new NT-based Mt Ringwood Gold Project. There is a scope of visible gold at Great Northern Leases. Drilling is also starting at the Phar Lap IOCG Project which is a Farm-in and Joint Venture Agreement with Iluka Resources.

.png)

Near Mine Exploration Highlights (Source: Company Reports)

Reported a debt free September Quarter: Western Areas reported a debt free position for the first time during September quarter of 2015 from the year of 2004, following the repayment of $125 million of convertible bonds during July 2015. The group reported a cash at bank (which includes FinnAust Mining) of $60.3 million. On the other side, WSA reported that its mine production reached 148,102 tonnes of ore at an average grade of 4.8% for 7,062 nickel tonnes during the September quarter which is the highest nickel in ore output from December 2013. Spotted Quoll mine production reached 80,702t of ore at 4.8% for 3,905 nickel tonnes (8.6M lbs), reporting the top quarterly production to date for the underground mine, and enhancing by 12% in nickel tonnes as compared to the earlier quarter. Mill throughput delivered 153,540t of ore at an average grade of 4.6% nickel with recovery of 89.2%. As per Flying Fox highlights, the mine delivered a production of 67,400 tonnes of ore mined at 4.7% for 3,155 nickel tonnes (7.0M lbs), with major ore production from longhole stoping (89%) while the rest is from jumbo development (11%). Meanwhile, the Cosmic Boy concentrator generated 153,540 tonnes of ore at an average grade of 4.6% nickel for a total of 41,221 tonnes of concentrate grading at 15.2% nickel during the September quarter. As a result, 6,252 nickel tonnes were produced with a metallurgical recovery of 89.2% as the plant was available 99.0%. Moreover, the highest concentrator throughput was achieved during September, at an average rate of around 80 tonnes per hour for four consecutive days.

.png)

September Quarter Production Highlights (Source: Company Reports)

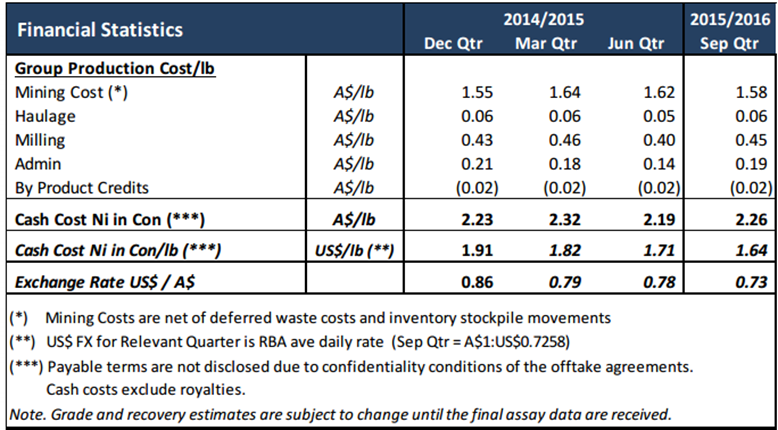

Focusing on operational efficiency to offset commodity pricing pressure: Despite the nickel prices pressure on the back of lower than estimated Chinese trade data and stainless steel demand, the group delivered a 37.5% rise in net profit after tax during fiscal year of 2015 and reported a final fully franked dividend of 4 cents per share in October 2015. This bottom line increase was mainly due to the group’s efforts to control its cost of production and delivery of a record decline in unit cash costs to $2.31/lb during the FY15 against $2.50/lb in FY14. The unit cash cost of production of nickel in concentrate (excluding smelting/refining charges and royalties) for the September quarter reached A$2.26/lb (or USD 1.64/lb), delivering a better performance than the group’s estimated average full year guidance range of $2.30/lb to A$2.50/lb for fiscal year of 2016. On the other hand, WSA’s September quarter cash costs have slightly increased as compared to the June quarter of 2015 as higher mill throughput was delivered during the June quarter. WSA approved Mill recovery enhancement project during July 2015 with project’s development cost estimated to be over $22 million during six months of construction. Meanwhile, WSA was able to decrease its unit costs from the last few periods due to the group’s positive reconciliation to reserve (including minimizing waste dilution), a steady and consistent mill feed blend as well as ongoing group’s efforts to control all costs at Forrestania.

Cash Costs Performance (Source: Company Reports)

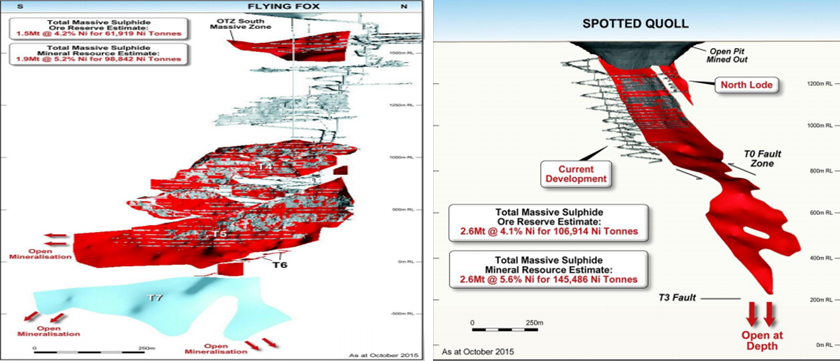

Strong resource potential: Western Areas has built a diversified assets base as well as made investments in potential capital growth projects like Mill Enhancement and Cosmos exploration and study work during 2015. The group’s core Flying Fox massive sulphide mineral resource reached 1,914,397 tonnes of ore at a grade of 5.2% nickel for 98,842 nickel tonnes during the September quarter while ore reserves reached 1,475,245 tonnes of ore at a grade of 4.2% nickel for 61,919 nickel tonnes. As per the Spotted Quoll update, Mineral Resources reached 2,579,139t of ore at a grade of 5.6% nickel for 145,486 nickel tonnes in September while ore reserve estimates are at 2,633,557t of ore at a grade of 4.1% nickel for 106,914 nickel tonnes.

Flying Fox and Spotted Quoll Mineral Resource and Ore Reserve estimates (Source: Company Reports)

Stock Performance: The shares of Western Areas plunged over 42.12% (as of December 08, 2015) during this year to date and fell over 13.85% in the last three months due to challenging nickel prices which were getting impacted by the ongoing decrease in stainless steel production as well as higher destocking periods. On the other hand, the shares slightly recovered in just last few days as management indicated an early positive sign for nickel industry wherein the LME refined stockpile decreased by around 10% from its recent highs coupled with decline in nickel pig iron output from China. Management also pointed to a recovering demand from China for 300 series stainless steel that has the highest nickel content. Moreover, battery market growth is estimated to generate a double digit growth, which would further add support to the nickel prices.

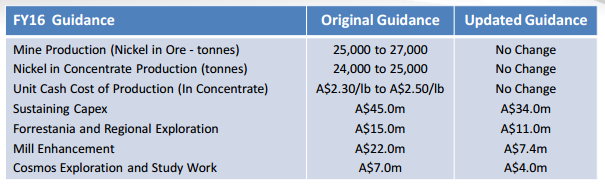

FY16 Guidance (Source: Company Reports)

Meanwhile, WSA is enhancing its current production via development ready projects like Odysseus, the Mill Enhancement Project and New Morning from its Flying Fox and Spotted Quoll assets. The group also acquired the Cosmos Nickel Complex and the exploration farm-in at the Western Gawler JV in South Australia to boost its long term production growth and exploration potential. On the other hand, WSA is adopting cost cutting initiatives and accordingly deferred capital expenditure expenses of over $32.6 million. With most of the development work being finished at the Flying Fox mine, the group has cut its capital expenditure estimates for fiscal year of 2016 to strengthen its cash flows. WSA is also targeting to achieve an optimal mining rate to maximize margins, on the back of short term nickel price volatility. We believe that the stock has the potential to grow further in the coming months as steady nickel prices estimations during FY16 might lead to a positive quotational pricing adjustments. Meanwhile, WSA shares are trading reasonably with a P/E of about 15x, as compared to its peers. Based on the foregoing, we give a “BUY” recommendation on this stock at the current price of $2.17

.png)

WSA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...