Company Overview - Whitehaven Coal Limited (Whitehaven) is engaged in the development and operation of coal mines in New South Wales. The Company operates in two segments: Open Cut Operations and Underground Operations. The Company’s Gunnedah operations include the Tarrawonga (70% owned by Whitehaven), Rocglen (100% owned by Whitehaven), and Sunnyside (100% owned by Whitehaven) open cut mines and the Gunnedah coal handling and preparation plant and train load out facility (CHPP’ (100% owned by Whitehaven). The Werris Creek mine is 100% owned by Whitehaven.

Analysis - We dealt with Whitehaven Coal Limited (ASX: WHC) sometime ago, and are back with our analysis update in view of some key developments for this Company, which is known to deal in Open Cut Operations and Underground Operations for coal mining.

First Mover Advantage in Gunnedah Basin (Source – Company Reports)

First Mover Advantage in Gunnedah Basin (Source – Company Reports)

Whitehaven as known to us, has the following project portfolio - Canyon, Maules Creek Project, Narrabri North, Rocglen, Sunnyside, Tarrawonga, Vickery Project, Werris Creek and so forth. The Company has plans to expand its open-cut mine portfolio.

Financial Performance FY14 (Source – Company Reports)

Financial Performance FY14 (Source – Company Reports)

As observed from the above, the FY14 revenue and EBITDA have gone up by 21% and 429%, respectively, as compared to the last year. The reported net loss included significant items of $10m on suspension of mining activities at the Sunnyside mine; cancellation of an infrastructure sharing agreement; write-offs of exploration expenditure; and provisions relating to bad debts.

At 30 June 2014, WHC had cash of $103m and net debt of $685m. There was no dividend declared in FY14 as per Company’s dividend policy.

Further, under the FY14 results, the Company reported some key highlights - improved safety performance across all the mines (with Seven Safehaven Rules introduction); record production from Werris Creek, Tarrawonga and Narrabri mines with saleable coal production reaching 8.2Mt (equity basis), i.e., 23% higher than last year; resolution on all legal hurdles enabling commencement of construction of the Maules Creek project in December 2013, and the project being on track with regard to first coal to be railed in the March 2015 quarter; mitigation of quality issues with Narrabri thermal coal; on-schedule completion of second longwall change-out at Narrabri; completion of Werris Creel mine’s expansion for increased production capacity; and cost reduction base set with the help of centralized procurement system.

Performance Summary (Source – Company Reports)

Performance Summary (Source – Company Reports)

The Company aims to double production to achieve sales of 23Mtpa by FY2018.

Narrabri yielded 5.7Mt in FY14 and is looked upon to produce 6.5Mtpa (managed basis) in FY15. The mine produced 1.697Mt ROM coal and 1.388Mt of saleable coal for the June 2014 quarter, which is 114% and 40%, up, respectively than in the previous corresponding quarter when a longwall change-out was under way. Narrabri is scheduled to have a single longwall move in FY2015.

Total open cut ROM production of 2.087Mt for the quarter was 43% higher than the previous corresponding period. Full year ROM coal production from the open cuts was 5.874Mt, 9% higher than the previous year. The Gunnedah CHPP is undergoing a restructure with reduction in number of employees. ROM coal production at Tarrawonga Mine in June was exceptionally high with a total of 340Kt produced in the month. The Rocglen Mine’s ROM coal production was of 0.458Mt and saleable coal production of 0.170Mt for the quarter. Werris Creek Mine’s production for the year was 2.356Mt of ROM coal and 2.310Mt saleable coal.

Maules Creek’s annualized production rate at the beginning are expected to be of 6Mtpa in Mar 2015 and should be expanded to its approved production level of 13Mtpa gradually. There has been an increase in funding (by $50m) to take care of the Maules Creek project till completion. The project is 55% complete.

This project is currently the largest under-construction coal mine project in Australia. The primary production will entail high quality thermal coal for electricity generators and metallurgical coals for use by steel makers.

Maules Creek Coal Overall Project S-Curve (Source – Company Reports)

Maules Creek Coal Overall Project S-Curve (Source – Company Reports)

Vickery Project by WHC has also been a target of attraction in the recent past. The Company is seeking JV partners as it intends to sell up to 25% of the project. State Government has given the approval for the Vickery mine but startup may be sometime in late 2017. The project may have the potential to positively impact the sales in 2015. The infrastructure already set, the Company would need to bank on low capital.

WHC is working on two additional track infrastructure projects and 30 tonne axle load upgrade to expand the capacity of the Gunnedah Basin rail system with regards to the Maules Creek contracted demand. As per the Company, these projects are on schedule for completion before the end of this calendar year.

WHC also has taken initiatives for increasing its market capabilities. It has opened an office in Tokyo, for instance.

The Company reported an expense of about $0.637 million on exploration during the June quarter 2014.

In 2014, WHC has awarded a US$100 million contract to Downer EDI Ltd. with regards to availing their services for construction for various projects including the Maules Creek Coal Handling and Processing Plant in the Gunnedah basin.

The Company may also refinance its existing debt facilities in the coming months.

The risks which we foresee constitute any delay in development work, costs at Maules Creek, problems with refinancing existing facilities, continuing poor sentiments in coal markets; commodity price and exchange rate fluctuations; and regulatory changes risks (such as decline in thermal coal use as environmental awareness and regulations increase, carbon tax and the mineral resources rent tax, etc.). Then one may also see a threat from operating and capital cost fluctuations.

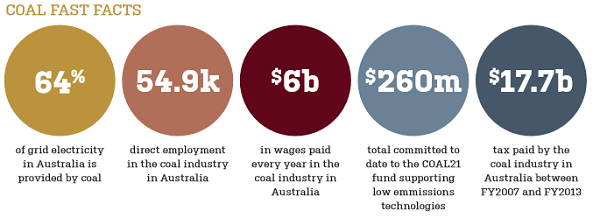

Coal Fast Facts (Source – Company Reports)

Coal Fast Facts (Source – Company Reports)

However, we do estimate a recovery in coal prices. This coupled with Maules Creek expectations to increase WHC’s exposure to higher value coals, may result in enriching the cash flow. We do see a margin expansion and a return to profitability in 2015 based on high output from WHC’s low cost and long-lived assets.

Saleable Production by Mine (Source – Company Reports)

Saleable Production by Mine (Source – Company Reports)

For instance, even in the existing softness in coal pricing and harsh currency scenario, WHC witnessed a 25% increase in production which translated to a 21.4% increase in revenue in FY2014. Further, the Company declared that there is an increase in global demand for coal in absolute tonnage terms. Even with declining coal’s share of energy supply but with growing demand for energy, the actual tonnage consumed may continue to rise.

Also, there are positive indications for the metallurgical coal market. Production cuts as reported are of the order of about 19.0Mtpa from the US, Canada, Australia and Mozambique, and suggest further cuts, which may help resurrect prices towards the end of this calendar year or early next year.

Breakdown of Whitehaven Coal Shareholder (Source – Company Reports)

Breakdown of Whitehaven Coal Shareholder (Source – Company Reports)

We also make a note of the recent news that 150 protesters descended on WHC’s site with an aim to affect production at WHC’s four coal mines, claiming that construction and expansion of coal mines will affect biodiversity and the environment. However, we also note a denial on any halt to operations by Whitehaven.

WHC Daily Chart (Source - Thomson Reuters)

WHC Daily Chart (Source - Thomson Reuters)

Based on the above observations and analysis, and in view of the fact that WHC is primed for a coal price up-turn and is doing well in terms of production, cost reduction and marketing strategies, we do see it as a long-term investment attractive player. Accordingly, we retain our recommendation as

BUY at the current price of $1.705.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...