Company Overview - Whitehaven Coal Limited (Whitehaven Coal) is an Australia-based company engaged in coal mining industry. The Company is a coal producer in New South Wales’ Gunnedah Basin. Whitehaven Coal owns three operating open cut mines at Werris Creek, Tarrawonga and Rocglen, the Narrabri North underground mine and Maules Creek Project. The Company also has interests in Vickery open cut project near its other open cut mines. The Company also has various exploration assets in New South Wales and Queensland. The Company’s projects include Canyon, Maules Creek Project, Narrabri North, Rocglen, Sunnyside, Tarrawonga, Vickery Project and Werris Creek. The Company’s other projects include Ferndale Project, Dingo Project, Sienna Project and Ashford project (Bonshaw). The Company operates in two reportable segments: Open Cut Operations and Underground Operations.

Analysis - We focus on Whitehaven Coal (WHC) in this report. The Company has announced about achieving financial close on 27th March 2015 for its $1.4 billion Senior Secured Bank Facility with a syndicate of Australian and international banks (ANZ, NAB, Westpac and a few other). The Company aims to use the facility’s $1.2 billion drawable line of credit for general corporate purposes. This has a maturity date of July 2019. The facility is expected to proffer flexibility for WHC over the next few years. Primarily, this debt refinancing will prove favorable than the existing facility and is estimated to result in a 100bps lower interest rate and an additional $200m funding headroom. The effective interest rate on WHC’s debt is believed to drop to under 5% from 6%. Further, the Company would be able to extend its debt maturity profile by around two and a half years. The Company conveys that the support from the bank syndicate is indicative of increased confidence in Company’s growth plans and the quality of its assets. Not only this, it reflects WHC’s upgraded solvency from cash margin standpoint while operationally, the Company with Maules Creek advancement ahead of schedule seems to do well. Given the fact that funding is in place to fully develop Maules Creek which has the potential to deliver higher volumes and earnings margins, WHC turns out be in the sweet spot for portfolio investors and corporate acquirers.

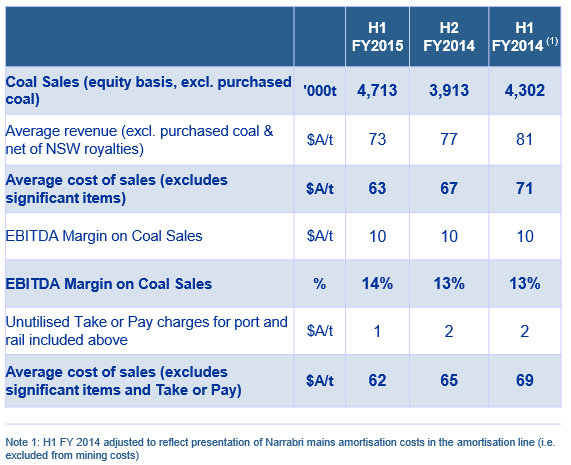

Sales and Cost Reduction (Source – Company Reports)

Looking at the advancements at Maules Creek, the Company has updated that railings from the mine commenced three months ahead of schedule. Given the entire situation and the progress made so far, WHC believes that the final CAPEX estimates would be about $25m lower than what was anticipated earlier, i.e., $767mn budget. In 1HFY15, the average cost of sales was $63/t. A further dip is expected in the costs by about $12/t in 2HFY15. The Maules Creek mine is particularly at 6mtpa with three months post the first coal shipments (with >700kt of coal already mined and March shipments to be ~470kt). About 2.5mt is expected to be the FY15 production. The mine is thus already generating a decent cash margin (although to be declared commercial by end of FY15). The Company has been able to sell low ash and high energy thermal coal unwashed.

Maules Creek Railing (Source – Company Reports)

As per the further updates, it is noted that the coal washery is about completion from mechanical standpoint and commissioning of the coal handling and the preparation plant has been reported for the month of April 2015. WHC further stated about on-track operations for the crushing and conveying circuits. Other key highlights entail assembling to be started for operation in 2015 by coal reclaimers; and the commencement of commissioning of coal stacker. The mine is reported to load 30t axle load trains of 8,200t. The Company believes that adequate contracted port capacity is foreseen until FY18 while there are no issues to port at the full production rate of >10mtpa.

Progress is expected with regards to completion of mine infrastructure area and the water dams. With two more excavators on order, the mining rates are expected to be about 9mtpa Run-of-Mine (ROM) from February 2016.

Saleable Coal Production (Source – Company Reports)

We also like that with all the efforts WHC is putting in place, the mining at Maules Creek may achieve a rate of 8mtpa in 1HCY16 and 10mtpa in 2HCY16 given the fact that full mining rate is about 13mtpa ROM for ~10.5mt of product coal. The EBITDA margins may be about $20/t in FY19 with EBITDA of $366mn. Furthermore, NPAT margins/tonne may surge to ~$6/t in FY19 with NPAT of ~$100mn. The net debt is likely to reduce to >$600mn in FY19. Overall, cost-out initiatives along with expansive coal market will prove beneficial. The Company is operationally cash flow positive given the spot coal prices. EBITDA margins of about $19/t or $20/t may be possible with spot thermal and met coal prices of US$64/t and US$86/t, respectively.

First Half Profitability (Source – Company Reports)

Once the full production is achieved for Maules Creek, WHC expects to do a low cost start up for Vickery. The production mix is expected to be 50:50 for met:thermal at full production. For met coal ramp up, WHC expects about 500kt in FY16, 1.5 to 2mt in FY17 and 2 to 3mt in FY18. The Company expects that the Vickery project should be offering a growth of 45mtpa post FY18.

The key growth drivers appear to be volume growth opportunity from Maules Creek, lower diesel costs, and the improvement in the outlook for thermal coal. Further, a foreign exchange rate may also be helpful.

Global Seaborne Thermal Coal Imports (Source – Company Reports)

Of course, one cannot neglect the risks related to commodity price and exchange rate fluctuations; infrastructure access based on contractual agreements etc. with or without risk of outages; operating risks; mine life extensions; operating and capital cost fluctuations; funding related risks; regulatory changes risks and the like.

Global Metallurgical Coal Demand (Source – Company Reports)

Nonetheless, the Company has demonstrated a striking organic growth profile with the saleable coal production increasing to around 20Mtpa by FY18 from the 10Mtpa in FY14. The production of higher quality pulverised coal injection (PCI) and semi-soft coal has also been witnessed to increase. The above 90% completion of the 10mtpa Maules Creek project with continuing improvement in productivity at Narrabri with an expectation of production increase to over 7Mtpa of saleable coal given the panel widening project in FY17, appear to be good catalysts. Lower unit costs are to be emanated from the aforesaid mines expected to work at a remarkable capacity. Further, debt covenants do not look as a concern in the near term given the recent debt refinancing. The earlier issues pondering over margin pressure, construction or commissioning risk and pending debt refinance seem to have been addressed now. The developments do show a great sigh of relief after the reported net loss of $77.9 million for the December half given weak coal prices. In the longer term, prospects for Chinese demand for Australian thermal coal is also expected to improve while benefits being expected to originate from the growing Indian demand.

WHC Daily Chart (Source - Thomson Reuters)

Based on the foregoing, we put a BUY recommendation for the stock at the current price of $1.48.

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...