Company Overview - Whitehaven Coal Limited (Whitehaven) is engaged in the development and operation of coal mines in New South Wales. During the fiscal year ended 30 June 2012 (fiscal 2012), Whitehaven Coal Limited and its controlled entities continued development at the Narrabri underground mine. The Company operates in two segments: Open Cut Operations and Underground Operations. The Company’s Gunnedah operations include the Tarrawonga (70% owned by Whitehaven), Rocglen (100% owned by Whitehaven), and Sunnyside (100% owned by Whitehaven) open cut mines and the Gunnedah coal handling and preparation plant and train load out facility (CHPP’ (100% owned by Whitehaven). The Werris Creek mine is 100% owned by Whitehaven. During fiscal 2012, the Company produced 4.28 million tons per annum of saleable coal. In June 2013, Farallon Capital Management LLC acquired a 9.905% stake in Whitehaven Coal Ltd.

Analysis - Whitehaven Coal (WHC) came out with its 1HFY15 results highlighting significant reduction in costs although the underlying net loss of $12m was reported. Net loss after tax was reported to be of the order of $78m given the $66m write-down of MRRT goodwill. The underlying EBITDA was $52m. It is to be noted that the Company could maintain EBITDA unit margins of $10/t owing to recent cost-out initiatives despite the weaker coal prices. Revenue of $371.8m dipped 8% from that witnessed during the corresponding period in FY14 due to falling coal prices.

Financial Highlights (Source – Company Reports)

The average cost of sales for 1HFY15 declined 11% from pcp to $63/t. There is a possibility of further decline by $1-2 in 2HFY15. The Company reported to have cash of $112m and net debt of $887m with a gearing of 22% as at 31 December 2014. WHC has reconfirmed the FY15 saleable coal guidance of 14Mt. Maules Creek final CAPEX is estimated to be lowered by $25m than the initial estimates of $767m.

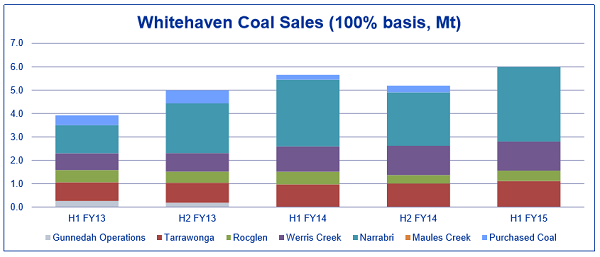

Saleable Coal Production – New Record (Source – Company Reports)

The December 2014 highlights specifically entailed railing of first coal from Maules Creek being three months ahead of schedule and first coal sales in January 2015. The construction at Maules Creek was 87% complete as at 31 December 2014 and the installed capacity to run at 6mtpa will be in place by mid-March 2015. The production at Maules Creek during the quarter totaled 94kt of ROM coal. WHC also reported coal sales of 2.9Mt for the quarter and a new record of 6.0Mt for the half year; ROM coal production of 2.2Mt for the quarter and 5.7Mt for the half year; and saleable coal production of 2.4Mt for the quarter and a new record of 5.7Mt for the half year. The third longwall change out at Narrabri was also completed ahead of schedule and on budget. Mining of LW04 commenced on 30 November 2014.

Maules Creek Mining Progress (Source – Company Reports)

The market senses that a boost is expected through 2015 for the Australia’s coalminers given the potential increase in market share from high-cost producers in the United States and Canada. This will benefit WHC to some extent. The coal sector has been struck by lower metallurgical and thermal coal trade, but the cost cutting has resulted in having the mines in a slightly better position. The share of the seaborne coal market has increased from 58% to 64% and there has been an increase in exports from Australia. The long-term scenario may differ slightly based on the demand and export situation. China will be a key target from supply and demand perspective. The country may tend to have more exports in view of the added tax on local coal sales. The price prospect for coking coal also looks little better this year.

Total Global Coal Industry Capex (Source – Company Reports)

Given the current situation, there is good chance that the coal sector may perform well in near future and WHC which illustrated a robust results with thrust on costs and margins may be good choice. The earnings may somehow be restricted owing to the current softness in coal markets. However, the Company does not expect a further weakening in thermal coal prices with an anticipation of price recovery in 2016. The production at Maules Creek mine and probable price improvement with the projected refinancing of $1.2 billion of debt will help WHC secure a better position. Refinancing of debt from US bond market may happen in two or three years’ time and not as of now. Existing $1.25bn facility is expected to perish by December 2016. In that case, the Company expects to come-up with a resolution in coming months given the solid appetite indicated by a range of banks in the US and Australia. As per the Company, Australian domestic debt may be a preferred option with the new facility expected to be of $1.25-1.4b with 5 to 7 years of duration. The refinancing activity may be looked upon as a catalyst for the performance and future growth.

Global Thermal Coal Demand (Source – Company Reports)

Asset development is also on track as directed earlier. The commencement of rail deliveries of coal from Maules Creek has been ahead of schedule. This project is expected to run about $25 million under its $767 million total budget. That is, about $25m of the contingency that was built into the $767m capex estimates is expected to be saved. The share of remaining Maules Creek capex is $120m out of which the Company expects to be able to defer about $20m in capex relating to site buildings. WHC has ordered an additional plant to enable output of 8.5mpta which is expected to be on site at end CY15. The plant, which is being financed by operating leases, is expected to be operational in early CY16. Early May is expected to mark the completion of the washery for production of met coal products in July 2015. This is of course subject to the market conditions.

The Vickery project is also considered to have a good potential in view of finalising a joint venture for development. The cost will be less than $50 million for its initial capacity of 4.5 million tonnes a year given that there is no requirement of constructing a processing facility on site or of a rail link until production increases beyond the current level. The government approvals in this regard were received in September 2014 and the Company re-stated that the earliest production from Vickery is not likely to happen before the full ramp-up of Maules Creek.

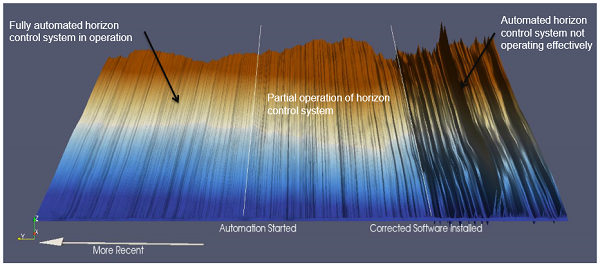

Narrabri Automation (Source – Company Reports)

As mentioned earlier, the net loss of $77.9 million for the December 2014 half has been reported by WHC in view of the fact that the falling Australian dollar could not balance the coal price softness then. However, the market is expected to be balanced in 2015 in view global production cuts in excess of 25 million tonnes per annum in metallurgical coal. Coupled with economic growth in Asia, the production cuts may bring the Asian seaborne thermal coal market to stability. The outlook for medium-term seems to be better in view of the recent International Energy Agency forecast of annual demand growth of 2.3% until 2019.

Record Sales for the Half Year (Source – Company Reports)

Overall, a constructive long-term view on coal markets, volume growth leverage from Maules Creek and refinancing of debt appear to be the key to success for WHC. Nonetheless, risks related to fluctuations in commodity price and foreign exchange, infrastructure access, regulatory change, operating and funding costs need to be considered for the resource sector.

Based on the foregoing, we reinstate a BUY recommendation for this stock at the current price of $1.525.

.png)

.png)

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...