Kalkine has a fully transformed New Avatar.

Company Overview: Whitehaven Coal Limited is engaged in exploration, project evaluation, project development and coal mining activities in New South Wales' Gunnedah Basin. The Company operates through two segments: Open Cut Operations and Underground Operations. It owns four open cut mines (Maules Creek, Werris Creek, Tarrawonga and Rocglen), one underground mine (Narrabri) and operates a coal handling and processing plant at Gunnedah. The Maules Creek Mine is located over 45 kilometers southeast of Narrabri and approximately 17 kilometers northeast of Boggabri in the Gunnedah Basin of New South Wales, Australia. The Werris Creek Mine is located over four kilometers south of Werris Creek on the Quirindi Road. The Tarrawonga Mine is located approximately 16 kilometers east of Boggabri. The Rocglen Mine is located over 28 kilometers north of Gunnedah on the Wean road. The Narrabri North Mine is located approximately 17 kilometers southeast of Narrabri and over 70 kilometers northwest of Gunnedah.

.png)

WHC Details

Growth Visibility in Long-run: Whitehaven Coal Limited (ASX: WHC) is involved in the development and operation of coal mines in New South Wales. As per FY18 report, its revenue is generated majorly from various countries such as Japan, Taiwan, Korea, India, China, etc. In FY18, Thermal Coal contributed ~80% of the total revenue while metallurgical coal contributed to the remaining portion. Its FY18 NPAT before significant items was reported at $525.6 Mn as compared to $367.2 Mn in FY17. Its underlying EBITDA for FY18 was reported at $940.0 Mn as compared to $714.2 Mn in FY17, which was majorly driven by a significant increase in EBITDA margin to $59/t in FY18 as compared to $46/t margin in FY17. This improvement can be attributed to strong operating performance coupled with the continued strength of the coal price environment, particularly in respect of high-quality thermal coal. Gross revenue for FY18 increased to $2,257.4 Mn as compared to $1,773.2 Mn in FY17, which was majorly due to the increase of realised price from $112/t in FY2017 to $130/t in FY18, and by an increase in sales of produced coal to 16.1 Mt in FY18 from 15.5 Mt in FY17. The increase in prices for thermal coal in FY18 was underpinned by the return of the market to supply/demand balance in FY17 following production cuts in a number of key coals producing countries, namely, China, Indonesia, the USA, and Australia. To maintain a balance between demand-supply, coal exporters are expected to reduce its production for the current year, which will help to control falling coal prices. As per projections, coal demand will increase till the next decade, especially from the markets such as Japan, Taiwan, Korea, and India, which will help the company to gain back the margins.

Moving forward, decent profitable margins, increase in infrastructure projects in the developing countries which require metallurgical coal to produce steel, are expected to act as tailwinds for the company.

.png)

Revenue Breakup by Product and Geography-wise (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 55.31% of the total shareholding. Farallon Capital Management, L.L.C., and Lazard Asset Management Pacific Company hold maximum interest in the company at 14.23% and 8.80%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

A Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for H1FY19 stood at 57.0%, 43.4% and 24.1%, better than the industry median of 52.5%, 35.9% and 20.6%, respectively, which implies decent fundamentals of the company. Its ROE for H1FY19 stood at 8.8%, better than the industry median of 6.6%, which implies that the company has delivered decent returns to its shareholders as compared to the broader industry.

Its debt to equity ratio for H1FY19 stood at 0.14x, below the industry median of 0.39x, which indicates that the company is less leveraged than its peer group, and it utilizes most its own funds to fuel its operations.

.png)

Key Metrics (Source: Thomson Reuters)

June ’19 Quarter Key Highlights: The total recordable injury frequency rate (TRIFR) at the end of June Quarter shown an improvement from 8.3 at the end of March to 6.16 at the end of June. It was added that group TRIFR remains well below NSW coal mining average of 14.67. The Run-On-Mine (ROM) coal production stood at 7.3Mt, which is 25% up as compared to the previous corresponding period. The June Quarter saleable coal production stood at 5.2 Mt, which is 9% up as compared to the previous corresponding period.

.png)

WHC’s Production & Sales Data (Source: Company Reports)

Full Year ROM Coal Production Exceeded Guidance: The ROM coal production on YTD basis till June 2019 was reported at 23.2 Mt, which exceeded the full year guidance. The company reported a record full year ROM coal production from Maules Creek at 11.7 Mt, which is an increase of 7% as compared to the previous corresponding period.

.png)

WHC’s FY2019 Production Guidance & Outcome (Source: Company Reports)

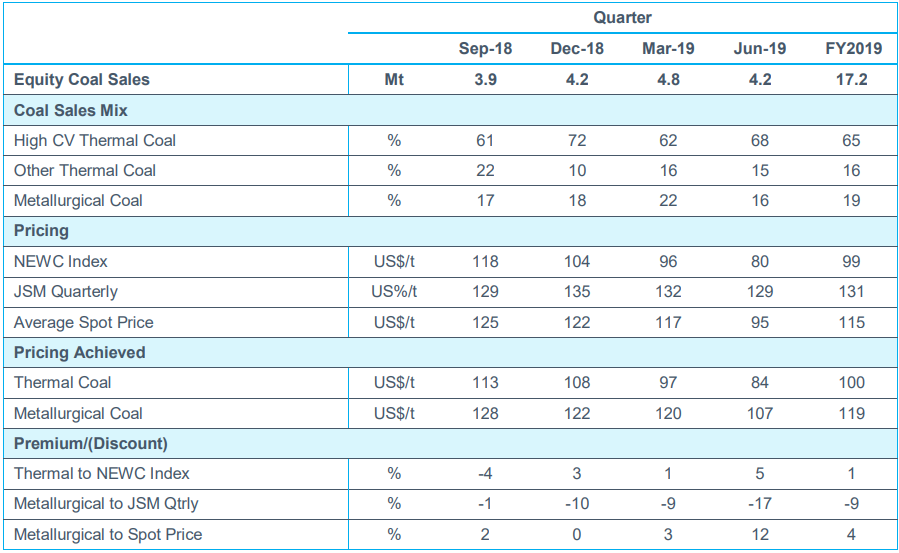

Equity Coal Sales for June Quarter & FY19 increased by 12% and 2% on pcp: Equity coal sales for the June quarter, including purchased coal increased by 12% to 4.364Mt as compared to the previous corresponding period. Managed coal sales, including sales of purchased coal increased by 12% to 5.338Mt as compared to the previous corresponding period.

Equity coal sales for FY2019, including purchased coal increased by 2% to 17.631Mt as compared to the previous year. Managed coal sales, including sales of purchased coal was reported at 21.638Mt, which was modestly lower than the previous year.

.png)

June ’19 Quarter WHC Equity Coal Data (Source: Company Reports)

Full-year Thermal Coal sales price reported higher than the benchmark price: The globalCoal Newcastle Index (gC Newc) thermal coal price softened to an average of US$79.86/t for the June quarter as compared with an average price of US$99.41/t for FY2019. In the Quarter, WHC achieved a price of US$84/t for thermal coal sales, which is 5% higher than the average gC Newc price for the period. For the full-year, WHC achieved a thermal coal sales price of US$100/t, which was US$1/t higher than the gC Newc price for the period.

The June quarter benchmark prices stood at US$208/t for the prime hard coking coal, US$129/t for the semi-soft coking coal (SSCC) and about US$141/t for Low Vol Pulverized coal injection (PCI) coal.

WHC’s Equity Sales and Prices Data (Source: Company Reports)

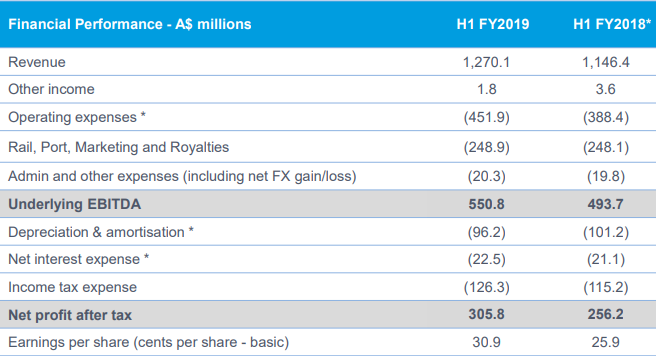

H1FY19 Financial Performance: Revenue for the period was reported at $1,270.1 Mn as compared to $1,146.4 Mn in the previous corresponding period, which was majorly driven by the substantial increase in realised prices to an average of A$155/t in H1FY19 up from A$124/t in H1FY18.The net profit after tax for the period was reported at $305.8 Mn as compared to $256.2 Mn in the previous corresponding period. The increased NPAT result was driven by a 28% increase in the per tonne EBITDA margin, which rose to $73/t in H1FY19 from $57/t in H1FY18 (restated). The increased EBITDA margin reflects the benefits of higher coal prices in the period.

H1FY19 Income Statement (Source: Company Reports)

Key Risks: WHC is vulnerable to certain risks such as volatility in the coal prices, foreign currency risk, operating risks such as unexpected maintenance and technical problems, failure of key equipment, etc.

What to expect: As per the release, thermal coal markets have softened due to a number of factors that caused prices to soften in the June quarter, majorly being low seaborne LNG prices into Europe and Asia, Chinese import restrictions and the negative impact upon global GDP from trade tensions between the United States and China. The decline in gas prices in Europe from US$9/GJ in September 2018 to US$3/GJ in June 2019 has led to power generators switching from coal to gas causing a reduction in demand for coal in the region.

Power demand in China has surged by 4.9% in the first five months of the year 2019. However, coal fired power generation increased in central and western parts of China. Moreover, growing domestic coal production (3.5% up y-o-y to May) has led to the overall reduction in coal imports in China.

Additionally, slowing world economic growth over trade tensions between the United States and China have also impacted the demand for thermal coal. Lot of measures are being taken by the central banking authorities to stimulate economic activity, which may cause an improvement in growth in FY2020.

With the benefit of both good weather and good prices, seaborne coal supply from Indonesia, Russia and Australia have increased year on year. With the softening of prices in the first half of 2019, the market is expected to rebalance as high-cost producers moderate the production. Exports from swing producers in the United States and Colombia have declined over the coal price environment. CRU estimates that exports from those two countries will fall by 21Mt and 5Mt, respectively in 2019. Over the course of the period since mid-2016, there has been little new large-scale production added to global thermal coal supply. With seaborne LNG trading below breakeven levels for new supply, some rebalancing can be expected to occur in this market as well.

The outlook for metallurgical coal remains healthy with steel production holding up well in several countries such as India, China and Japan, which are dependent upon the seaborne market to meet coking coal needs.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1- Price to Earnings (PE) Multiple Approach (NTM):

.png)

Price to Earnings (PE) Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

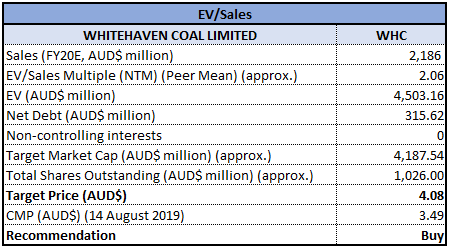

Method 2- EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: WHC’s shares generated a negative return of 25.42% in the span of the previous 6 months. Currently, the stock is trading close to its 52 weeks low level of $3.310 with reasonable PE multiple of 5.960x and an annual dividend yield of 8.38%, indicating a decent opportunity for accumulation. On the other hand, the recent slump in coal demand, especially by the import restrictions in the Chinese market, has put a toll on the coal prices. To maintain a balance between demand-supply, coal exporters are expected to reduce its production for the current year, which will help to control falling coal prices. As per projections, coal demand will increase till the next decade, especially from markets such as Japan, Taiwan, Korea, and India, which will help the company to gain back the margins. With the decent volume growth visibility, healthy balance sheet, respectable operating margins and return ratios, we have valued the stock using two relative valuation methods, Price/Earnings (P/E) and EV/Sales multiple and have arrived at a target price of low double-digit growth (in percentage term). While the group's earnings result is due around August 15, 2019, the performance seems to be in congruence with the outlook and expectation. Hence, we give a “Buy” recommendation on the stock at the current market price of $3.490 per share (up 0.867% on August 14, 2019).

.png)

WHC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...