Kalkine has a fully transformed New Avatar.

Company Overview: WiseTech Global Limited (ASX: WTC) is engaged in providing software solutions to the logistics industry. Through its services, the company enables logistics service providers for movement and storage of goods and information, domestically and internationally. The company operates through ~50 office locations, that serve a client base of 12,000 organisations across 150 countries. CargoWise One is the flagship technology offered by WiseTech, that enables smooth execution of highly complex logistics transactions and managing the operations on one database..png)

WTC Details

High Customer Loyalty Driven by Investments in Innovation: WiseTech Global Limited (ASX: WTC) is engaged in the provision of software solutions to the logistics sector through its flagship technology, CargoWise One. The technology has enabled customers to manage complex transactions, thereby boosting productivity and reducing costs. The company has developed a platform of trust through continuous product innovations and aims for further development, to boost customer retention and recurring revenues in the coming years. It is focused on expanding its flagship technology through innovation and acquisitions, enabling better business operations for logistics service providers across the world. In the last five years, the company has invested $309 million to enhance its pipeline of innovations and provided for multiple upgrades across its platform.

Revenue for the year ended 30th June 2019 amounted to $348.3 million, representing an increase of 57% on the prior corresponding period. The period was marked by high recurring revenues as a result of continued investments in innovation and product development. The company reported 99% recurring revenue in CargoWise One and 88% recurring revenue overall. EBITDA for the year came in at $108.1 million, up 39% on $78 million reported in the prior corresponding year. EBITDA margin excluding acquisitions over the 3 years covering FY16 (Pro-forma) – FY19, went up by 18 percentage points to 48%. The company provided for over 830 product upgrades and enhancements during FY19, with a total investment of $113 million. The company reported organic revenue growth of 86%, delivering on its objective of boosting the usage by existing customers. Moreover, the company has also seen a positive response from mid-large customers, which contributed a larger share of revenue during FY19. During the year, WiseTech benefitted from the network effect created through entry into new markets and acquisitions, as more and more players in the logistics industry adopt its technologies increasing its popularity across the globe. As a result of the benefits offered by CargoWise, a strong strategic vision and a never-ending drive for innovation, the company witnessed a mere annual attrition rate of less than 1%..png)

Top Customers Portfolio (Source: Company Reports)

1HFY20 Financial and Operational Highlights: During the half year ended 31st December 2019, the business continued to grow with revenue and gross profit rising by 31%. Net profit for the period witnessed a whopping increase of 160%, reflecting continued customer loyalty towards CargoWise and focus on growth strategy. During the half, existing and new customers continued to drive revenue and delivered growth of $24.3 million on the prior corresponding half.

With the business scaling remarkably over the past few years, the company resolved to increase its investment in research & development by 30-40% in FY20, to capitalise on opportunities in the future. While the management has downgraded the financial guidance for FY20, the company is confident on maintaining an upward trend and expects revenue in FY20 to deliver double digit growth in percentage terms, on the back of a business strengthened by an established brand value and continued product innovation.

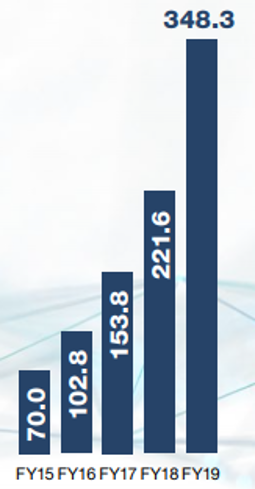

The company is focused on product development and has gained huge traction from the market on the back of its business model. With the high quality of offerings and a global footprint, the company has delivered significant growth in revenue over the period of FY15 – FY19. As a result of continuous efforts in areas of global expansion, enhanced product capabilities, industry penetration, etc., the company has reported a 5-year compound annual growth rate of 49.4% in revenue. In these 5 years, the company has introduced around 3,500 new features and enhancements to its product range, delivering on its strategy of increasing usage through innovation. During FY19, the company invested a substantial amount in high innovation product development that comprised 32% of the revenue generated during the period.

Growth in Revenue (Source: Company Reports)

Business Growth Led by Product Innovation and Global Footprint in 1HFY20: During the six months ended 31st December 2019, revenue came in at $205.9 million, representing an increase of 31% on the prior corresponding period. Gross profit increased at the same rate and came in at $169.4 million. Net profit for the period stood at $59.9 million, up 160% on the prior corresponding half. The Board declared an interim dividend amounting to 1.7 cents, up 13% on prior corresponding period dividend of 1.5 cents.

1HFY20 Results (Source: Company Reports)

During the half, the company invested for the expansion of its technology platform to grow its global footprint. New additions to product capabilities and logistics industry experts boosted the pipeline for future growth. With the rising needs of technology across the logistics industry, the company has its eyes on acquiring new customers and markets, while simultaneously increasing its business among the existing customers. During the half, WiseTech Global reported a growth rate of 24% in organic revenue from existing and new customers, driven by increased usage of CargoWise by existing customers, transition of licensing and added revenue from new products and features. To enhance its skill set, the company carries out acquisition of strategic assets in the form of software companies or specialist technology teams. Revenue from these acquisitions witnessed a rise of $24.9 million during the first half.

Progress on Growth Strategy: During the half, the company invested an amount of $73.3 million to expand its pipeline of commercialisable innovations and came up with more than 450 enhancements and upgrades in products across the CargoWise platform.WiseTech Global has its development teams in over 20 countries. Pursuant to the development initiatives in the first half, the company witnessed CargoWise customer revenue growth of $17 million, with increased usage across the customer base, increased popularity across new users and geographies and movement into new modules. The company has all the top 25 global freight forwarders using its platform, with an additional 10 large global forwarders in the process of completing global forwarding rollouts in CargoWise. Another strategic achievement was the addition of new customers on the platform, including Shanghai Coil Dragon International Logistics, Green Worldwide Shipping and PT Yamato Indonesia. Strategic acquisition after 1st July 2019 to serve added capabilities on its plate comprised of, Cypress in September 2019, Depot Systems in October 2019, Ready Korea in December 2019, and SISA Studio Informatica SA in February 2020.

While the company had begun recovering from the shock waves from the US-China trade war in early 2020, another challenge in the form of Coronavirus was awaiting the business. As a result of the shutdown in China, the company has seen adverse impacts on manufacturing, supply chains and economic trade across the world. Therefore, the impact of the same has been accounted for in the expected results for FY20. However, the company expects to see a quick rebound in the business as soon as China embarks on the path of recovery.

Shareholder Update: In a recent announcement, the company updated that The Capital Group Companies, Inc. ceased to be a substantial shareholder, with effect from 28th February 2020.

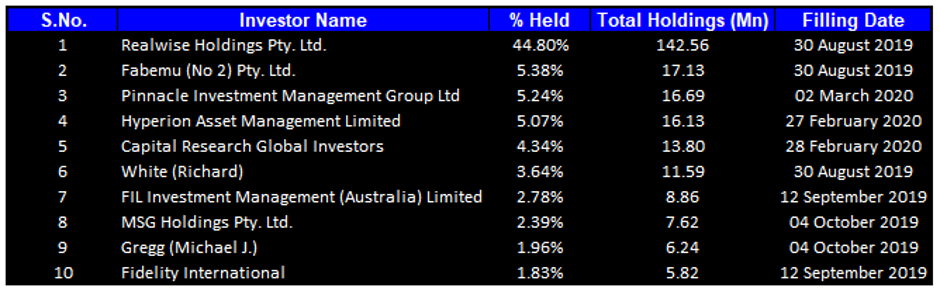

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 77.44% of the total shareholding. Realwise Holdings Pty. Ltd. held the maximum number of shares with a percentage holding of 44.80%, followed by Fabemu (No 2) Pty. Ltd. holding 5.38% of the shares.

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: For 1HFY20, the company reported gross margin at 80.9%, which was in line with the gross margin of the previous half. EBITDA margin and net margin for the half stood at 26.6% and 29.1%, respectively, at par with the industry median. Over the prior corresponding half, the company reported a reduction in debt as a multiple of equity, which stood at 0.05x in 1HFY20 and 0.08x in 1HFY19. Current ratio for the half also improved on the prior corresponding half and stood at 1.53x, reflecting a decent position to address the short-term obligations of the business.

Key Metrics (Source: Thomson Reuters)

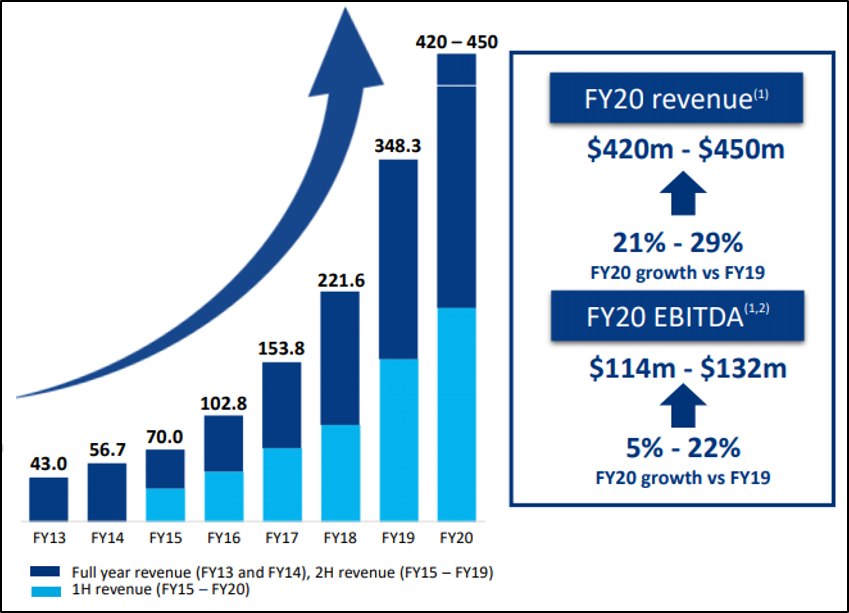

Guidance: Taking the potential impact of COVID-19 on the operations, the company now expects revenue for FY20 to be in the range of $420 million - $450 million, depicting growth in the range of 21% - 29% on FY19, reflecting the strength and resilience built over the years.EBITDA for the year is expected in the range of $114 million - $132 million, representing growth in the range of 5% - 22%. Previously, revenue was expected in the range of $440 million - $460 million and EBITDA in the range of $145 million - $153 million.

FY20 Forecast (Source: Company Reports)

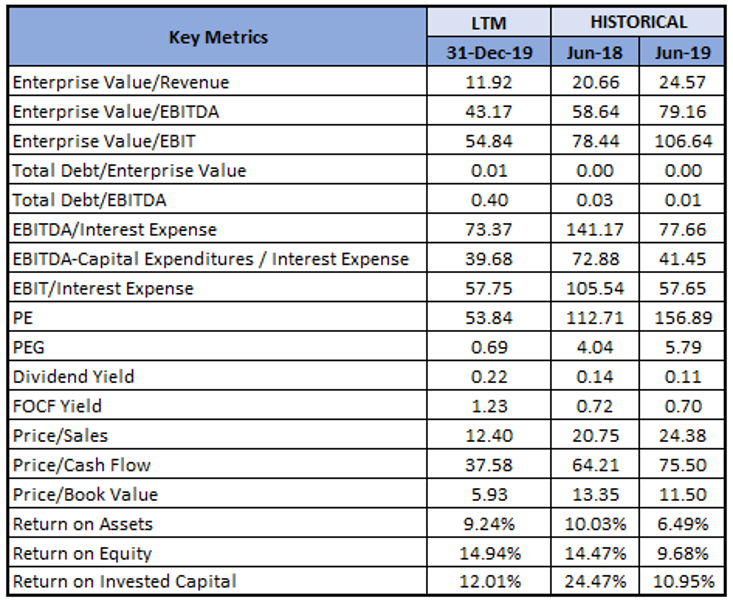

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: P/E Market Multiple Based Valuation(32).png)

P/E Market Multiple Method (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company has corrected by 42.26% in the last one month and is currently trading near its 52-week low of $14. Despite the outbreak of Coronavirus, that has taken a toll over the world economies, the company has issued revised financial guidance with double-digit growth in revenue and EBITDA on y-o-y basis. This reflects the confidence demonstrated by customers over the years that will continue to grow as the company continues to drive innovation on the platform. Historically, the stock of the company has been trading at ~4-year average P/E of 111.20x but presently it is trading at 74.41x of FY20e which makes it below the historical average. Hence, considering the growing popularity of CargoWise, increased investments in innovation, minimal customer attrition rate, and global expansion initiatives, we have valued the stock using a ~4-year average P/E market multiple of ~91.2x (20x discounted to 4-year average assuming qualitative earnings scenario due to the US-China trade war and unexpected coronavirus outbreak) to FY20E consensus EPS of $0.202 and arrived at a target price of lower double-digit upside (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $15.030, down 2.907% on 6th March 2020.

WTC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...