Company Overview - WorleyParsons Limited is engaged in providing engineering design and project delivery services, including maintenance and reliability support services to Hydrocarbons; Minerals, Metals and Chemicals; Infrastructure and Environment; and Power. Its segments include Hydrocarbons, which deliver services to the hydrocarbons market; Minerals, Metals & Chemicals, which deliver services to the minerals, metals and chemicals markets, encompassing alumina, base metals, precious metals, coal, iron ore and chemicals; Infrastructure and Environment sector, which offers a range of services in water, environment, transport, ports and marine terminals, restoration, geosciences, master planning and advanced analysis, and Power, which offers a range of services across the power generation, transmission and distribution value chain, from conventional technologies, such as fossil fuel and nuclear power generation.

Analysis - Today, we are re-looking at WorleyParsons (WOR), the engineering design and project delivery services’ giant, which has seen a lot of challenges in many of its key markets during the first phase of the year 2014.

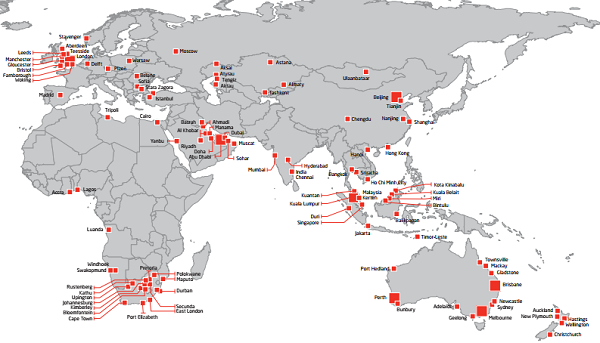

The Company is a globally diverse entity with about 157 offices in 46 countries, which in a way is beneficial while managing adverse market conditions in some geographies and capitalizing in others. WOR’s recent key decisions to prosper in difficult conditions are culminating into a positive environment. One such effort is directed towards the simplification of its corporate structure entailing reorganization of business into three segments, namely, Services, Major Projects and Improve. Other efforts relate to reduction in overhead costs and facilitating high-end customer satisfaction.

Although the FY14 balance sheet was strong with remarkable operating cash flow of $550.1 million, there was a decline in underlying net profit after tax. This was mainly due to low contribution from the Australian business and pitiable commercial performance on a project in Cord - the Canadian construction and fabrication operation. The Company reported an aggregated revenue of $7,364m, down 3%.

The Board resolved to pay a final dividend of 51.0 cents per share 20.5% franked, taking the total dividends for the year to 85.0 cents per share, down 8.1% from 92.5 cents per share last year. The Company admits that its total shareholder returns have gone down in recent years, and hopes that 2H14 may mark the beginning when it again starts providing satisfactory returns in view of its revised strategy and investment review framework.

Financial Performance (Source – Company Reports)

Financial Performance (Source – Company Reports)

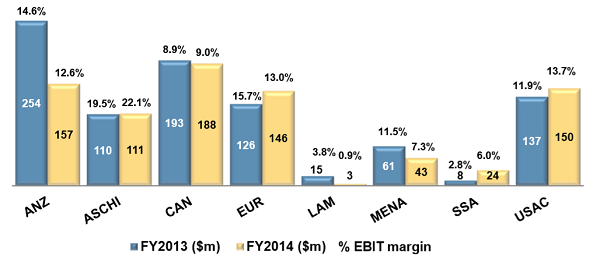

More or less, the earnings were in line with guidance. Further, the gearing ratio remained solid at 19.5%. The Company saw an improvement in Group EBIT margin in 2H.

There was increased contribution from Rosenberg and project activity in the UK. However, EBIT from ANZ led to a decline owing to weak project activity.

Among the sectors, the Hydrocarbons sector reported aggregated revenue of $5,372 million and EBIT of $627 million, which is a decline from the previous year. Reduced earnings were witnessed in all regions, barring Europe where the positive earnings resulted from Rosenberg WorleyParsons in Norway and Sub-Saharan Africa owing to a major project in said region. The Australian market witnessed a reduction in project activity. Improved performance of the WorleyParsons’ Cord business in the 2H could not offset the poor performance of project in the 1H.

Aggregated Revenue by Region (Source – Company Reports)

In the Minerals, Metals & Chemicals sector, the Company reported aggregated revenue of $1,066 million and EBIT of $131 million, lower than the previous year. The EBIT margin weakened by 0.7%.

For the Infrastructure sector, WOR reported aggregated revenue of $926 million and EBIT of $64 million, which is also less than what was witnessed last year. This sector also had 3.4% decline in EBIT margins. The faint resource project activity in Australian business and the cancellation of a nuclear project in European business were the key reasons of the results of Infrastructure sector.

Underlying Operating EBIT (Source – Company Reports)

Underlying Operating EBIT (Source – Company Reports)

Nevertheless, the Company’s efforts in realigning its business strategy appears to bring light through behind the dark clouds.

In terms of projects, WOR has about 16+ major project contracts which amount to ~12% of FY14 aggregated revenue. For example, there are 13+ major projects in North America which amount to ~21% of North America FY14 aggregated revenue.

Total Revenue by Region (Source - Company Reports)

The Company is in the process of coming-up with new ventures in alignment with existing businesses. For instance, an advisory business, namely, Advisian; and Digital Enterprise are two new ventures.

With a very recent announcement on renewal of contracts in Canada, WOR was happy to share the completion of negotiations and official award of extension of the engineering and procurement services agreement with two of its clients for an additional five years from July 2014. With this, the Company expects annual revenues of about CAD 150 million as a forecast.

WOR Global Operations (Source - Company Reports)

WOR Global Operations (Source - Company Reports)

The Company also announced that it has been selected to deliver engineering, procurement and construction management (EPCM) services for Chevron Munaigas’ Samal Wind Park Project in Kazakhstan.

Examples of other major projects awarded to WOR in 2014, include, but are not limited to, North West Redwater Partnership, Sturgeon Refinery Upgrader Piperacks/Flare – EPCM, Canada; Williams Companies Redwater Debottlenecking Modules, Canada; EP PetroEcuador Esmeraldas Refinery Rehabilitation Project Ecuador/Houston; Morobe Mining JV Wafi-Golpu Exploration Shaft, Pre-feasibility Study, Papua New Guinea; and Vale S11D Construction Management extension Brazil/ Canada. WOR has also discovered 174 fields in Arctic with 83% of discovered resources being in Russia.

From outlook standpoint, the Company expects flat global capital expenditure levels in Hydrocarbons sector for FY2015 in view of completion of on-going projects. It also expects new projects should be initiated by its customers for expanding WOR’s growth opportunities. The three recent under-cover contracts awarded to WOR are thought of as key factors that would bring improvement in the Company’s performance. A strong capital expenditure is expected for the Chemicals industry within the US. WOR believes that increasing fertilizer demand will help WOR with multifarious growth opportunities. The Minerals and Metals capital expenditure will face the decreasing trend and a recovery is foreseen in the medium term only. Non-resource Infrastructure has a stronger outlook as opposed to resource-related Infrastructure which depends on the outlook for the Hydrocarbons and Minerals, Metals & Chemicals sectors.

WOR also expects FY2015 margin improvement to be one of the key points which the Company wants to focus on along with ramping of awards. For example, WOR will initiate to work for opportunities identified to support LAM from Gulf Coast in FY2015.

Certain risks that the Company believes it faces relate to its reputation, business strategy and organizational changes, project delivery, competition, volatility of commodity prices and cyclical demand, legal and contractual risk due to disputes with third parties, and partnership-based performance in case of joint ventures and third-party engagements. Then, there also exists a risk with regards to converting new opportunities in the LNG, deepwater, US downstream and Norwegian Continental Shelf markets. WOR hopes that it is able to mitigate any of aforementioned risks in a timely manner with its persistent efforts.

Certain steps, such as those related to acquisition of MTG appear to be in alignment with WOR’s business strategy of leveraging and building on core technical skills and geographic trail. The Company’s recently acquired TWP business in South Africa is also found to be fruitful in improving the safety performance. There was a margin improvement in Asia, China and the USAC as projects with better margins replaced the projects with low margins, in 2H14 particularly.

WOR Daily Chart (Source - Thomson Reuters)

WOR Daily Chart (Source - Thomson Reuters)

From competition standpoint, WOR has a broad technical expertise, diverse geographic landscape, realigned business strategy; healthy balance sheet and cash flow, which can be leveraged to emerge as a strong leader.

Moreover, the Company is putting efforts in order to have minimal contract deferrals and cancellations in view of a lot of uncertainty in the market conditions, which is expected to be little faded in coming years though, thereby benefitting WOR. Further, its realigned business strategy is showcasing paybacks in terms of margin and operations. Moreover, various design contracts won by WOR should be heavy on its pocket while adding to the profits. Given this scenario, we recommend a

BUY for this stock at the current price of $14.32.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...