Trading update for YTD March

The period saw a moderate decline in revenues though margins continue to be maintained. Aggregated revenues came to $ 5.32 billion, a decline of 5% over the previous period and the underlying EBIT was $ 251.3 million, down 4.7% over the previous period. EBIT margin was maintained at 4.7%. The underlying NPAT at $ 139.9 million was down by 3.3% over the previous year though NPAT margin was also maintained at 2.6%.

Aggregated revenues for the third quarter amounted to $ 1.7 billion down 5.7% over the previous year. The underlying EBIT at $ 70.5 million was down 17.5% over the previous year and the underlying EBIT margin at 4.1% was down 0.6% over the previous year. The underlying NPAT of $ 35.6 million declined by 18.9% over the previous year while the underlying NPAT margin at 2.1% was down by 0.3% over the previous year. Because of the decline in margins in the third quarter, the company has taken the necessary action to make the appropriate adjustments to the business.

Among the appropriate actions taken include adjustments to the headcount. The position relating to the global headcount was as follows:

.png) Global Headcount (Source: Company Reports)

Global Headcount (Source: Company Reports)

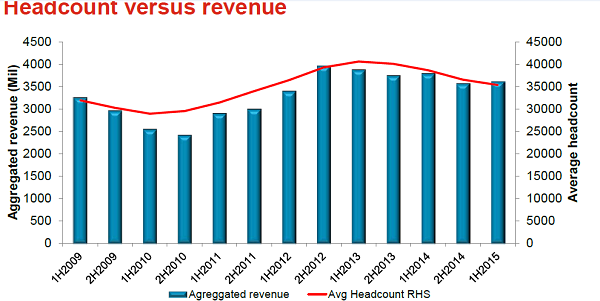

The headcount has been adjusted to provide a closer correlation with revenues after making necessary adjustments and the relationship can be seen below:

Headcount Vs Revenue (Source: Company Reports)

Several other measures were taken to reduce costs and boost revenues. The monthly hours charged versus utilisation rates are showing an upward trend. Selected operations have been transferred to execution centres with lower costs. Excess floorspace have been released and IT operations are being moved from a fixed cost basis to a variable cost basis. Occupancy levels are being increased in offices and the average cost of debt has been reduced.

The security of earnings and therefore their certainty have been increased as the year has progressed and the typical profile has changed from 50% secure and 15% blue sky to 95% and a negligible percentage respectively. Approximately, $ 1 billion in new awards have been achieved

.png)

New awards achieved (Source: Company Reports)

The diversification of the customer base has promoted increased resilience and the top 10 contracts account for only 15% of revenues and the majority of revenues are generated from smaller contracts thus providing a much larger customer base.

.png)

Diversification of customer base (Source: Company Reports)

The company continues to be regarded by customers as the market leader in the hydrocarbons industry.

The strategy framework

The company uses a strategic pyramid which puts together various levels of coordinated effort. The different levels consists of corporate strategy, strategy for global sectors, strategies by region and strategies by location. Each level is built on the success of the level that supports it and harmonises with the overall purpose of the company.

.png)

The strategy pyramid (Source: Company Reports)

The company defines its purpose as being a professional services business, a partner in the delivery of sustained economic and social progress and creating opportunities for countries and communities to create their own future. It recognises this can be done only with shareholder support earned by generating earnings growth and delivering satisfactory returns.

With respect to near-term shifts, the business has to reposition itself. To cope with the oil price shock, the business opportunities lie in asset productivity enhancement, oil recovery enhancement, and improvements in refining industry margins and increased chemical activity in south-east Asia and the Middle East. The low prices of gas need to be offset with chemical and petrochemical activity and the development of high energy intensity processes such as the manufacture of aluminium. The fall in commodity prices such as iron ore, copper and coal provide opportunities in productivity advisory and enhancement services, the optimisation of supply chains and upgrades and expansions which are capital intensive. The geopolitical situation will give rise to customers seeking support for advisory and execution activities in foreign markets and capitalising on the continuing investment in China.

It is clear that the company is now in a transition period where historical revenues and the underlying EBITDA will no longer be sufficient and the future can only be secure through its strategy for growth.

.png) Strategy for growth (Source - Company Reports)

Strategy for growth (Source - Company Reports)

The differentiators have been identified as technical capabilities and local presence as the key to future growth. There will be an enhanced focus on improvements in the front-end with selective delivery offerings such as PMC and EPCM/EPC. The emphasis will be on 5 projects and 5 strategic themes. Project 1 will be to build an advisory business that is world class and seeks to dominate the early phases of projects. This will include strategic and management consulting, niche and specialist consulting as well as technical consulting. Project 2 will involve being the global choice for PMC providers which will involve moving away from commodity services and focusing on areas such as cost control, contract management and planning. Project 3 will involve building a major improvement business focusing on operating and capital expenditure especially in selected areas such as LNG, water and power. Project 4 will concentrate on being the smartest and most responsive local services provider which will bolster the willingness of customers to pay. Finally, project 5 will involve the differentiation from competition by applying the optimisation of global delivery centres and the use of digital technology for delivery.

.png) Worley Parsons Daily Chart (Source - Thomson Reuters)

Worley Parsons Daily Chart (Source - Thomson Reuters)

There will be emphasis on the management of four critical financial risks including currency risk (such as matching the currency of payment to the currency of cost), interest-rate risk (95% of debt is currently at fixed rates), liquidity risk for normal and stressed conditions and credit risk to evaluate potential customer defaults. Gearing will be maintained within the target range of 25% to 35% and the headroom on funding will be maintained at around 1.5 times EBITDA and interest cover below 10 times.

We believe that the prices of the stock will continue to fluctuate in tandem with commodity and energy prices because of its role in the energy and mining businesses. We believe that the share is presently undervalued in relationship to the fundamentals and that's the market has bottomed out. We put a BUY on the stock at the current price of $10.86.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...