Company Overview - WorleyParsons Limited is engaged in providing engineering design and project delivery services, including maintenance and reliability support services to Hydrocarbons; Minerals, Metals and Chemicals; Infrastructure and Environment; and Power. Its segments include Hydrocarbons, which deliver services to the hydrocarbons market; Minerals, Metals & Chemicals, which deliver services to the minerals, metals and chemicals markets, encompassing alumina, base metals, precious metals, coal, iron ore and chemicals; Infrastructure and Environment sector, which offers a range of services in water, environment, transport, ports and marine terminals, restoration, geosciences, master planning and advanced analysis, and Power, which offers a range of services across the power generation, transmission and distribution value chain, from conventional technologies, such as fossil fuel and nuclear power generation.

Analysis - We cover WorleyParsons (WOR), the engineering company providing professional services to energy and resources sectors etc., in this report. The Company reported that WorleyParsonsCord has been awarded an oil sands fabrication, modularization and construction contract in January 2015. Specifically, WOR has been selected to provide fabrication, modularization and construction services in an agreement with a major exploration and production company in Canada to construct an oil sands mining project. This contract will be led and executed by the WorleyParsonsCord Edmonton Operations location and is expected to boost the performance. The project is valued at about $135 million CAD and is expected for completion in mid-2016.

The other important announcement entails Suncor extending its engineering and procurement multi-use agreement with WOR. This extension has been done for an additional three years wherein WOR will be providing its engineering, procurement and project delivery services for Suncor major projects. In fact, WorleyParsons Global Delivery Center offices in China and India are positioned to provide support to WOR personnel deployed on Suncor projects across Canada, as and when necessary. A further update entails fetching of the award for regional preferred status framework agreements for BP’s downstream business units. This entails WOR to proffer engineering, procurement and construction management services. Further, the agreement is a multi-year agreement with a contract for the onsite Improve relationship at the Kwinana refinery held by WOR since 2008. Through such platforms, WOR intends to create mutual value in long-term relationship with BP.

WOR Services (Source – Company Reports)

With the above in hand, we also make a note of uncertainties over global capex and unfavorable oil price environment. Given the economic conditions, WOR is noted to be down >50% in 6 months and >70% in 3 years. However, the gearing looks to be into the target range of 25-35% and $300-800m of capital is available for buybacks. With FY14 gearing of 19.5%, WOR has been below the target gearing range of 25-35% which looks good. Gearing has remained <25% for the past 5 years with an eye on acquisitions. It is important to note that in present scenario as well, WOR can raise debt at 5% at ease. Also, a buyback accretion may favorably balance out the risks associated with earnings. In addition, WOR has a strong balance sheet. Market reports that the ASX200 is on an 80% P/E premium to WOR as opposed to 5 year average 10% discount. On the other hand, WOR’s global peers trade on a 25% premium as opposed to 5 year average 5% discount. In the last 5 years, the Company witnessed about 127% cash conversion of earnings. The mid-cycle is expected in FY15.

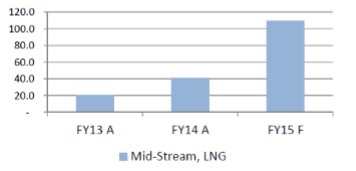

Mid-stream LNG (Source – Company Reports)

The business still remains as one of the global leaders which is capital light. It further has 100% cash conversion of earnings in market with long-term prospect. The 1H15 results due in February 2015 are expected to be solid with 8% annualised yield estimated to be delivered.

We have also noted that ‘not so encouraging’ results from WOR’s peers such as Wood Group and Jacobs Engineering may indicate a negative outlook for WOR. However, we would like to be patient with the expected results in February 2015 to hear from the horse’s mouth directly. The Company has otherwise underperformed global peers by 15% including peers who have more greenfield construction exposure than WOR. WOR has at the same time outdone many domestic energy players such as STO. Also, any significant amount of WOR’s FY15 revenues to be cancelled or deferred is not expected as most of the revenues are associated with near-completion brownfield projects or greenfield projects.

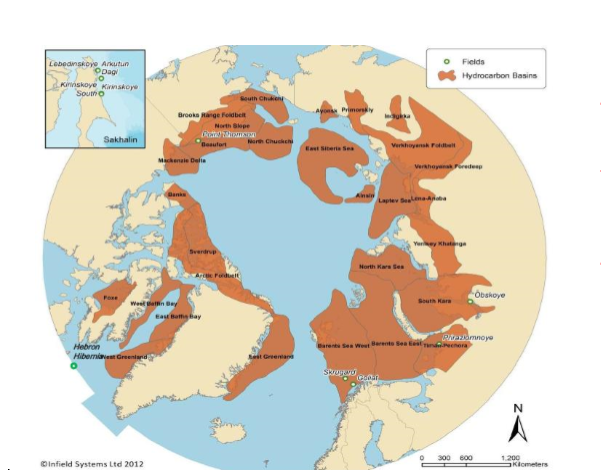

Potential in Arctic Reserves (Source – Company Reports)

Weaker A$ with 88% of revenues outside of Australia and New Zealand has benefitted WOR. Till sometime back and as reported by the Company, the translation effect of a 1c change in A$ vs US$, vs GBP and vs CAD has been about $0.6m, $0.8m and $0.4m, respectively to group NPAT. Nonetheless, the observed A$ benefit in FY14 was more than this indicating an operational benefit with A$ revenues less than A$ costs. Based on the WOR prospective, a large number of small to medium sized contracts across Improve (brownfield, debottleneck, asset management) and Services (pre-FEED, FEED services, etc.) with various new ones are not to be underestimated for performance evaluation. It is also understood that about ~50% of WOR’s hydrocarbons business is mid/downstream/gas which should be relatively defensive. It looks that 70% of WOR Hydrocarbons is oil exposed and 30% gas. 22% of the Company’s FY14 EBIT emanated from MMC & Infra, within which chemicals sector growth (Asia, US) is expected to continue.

Looking a little more backwards, the business re-organization has been complete and the Company could resolve its Cord issues. This collectively improved the 2H14 margins. We also are reminded that WOR reported sales of A$9.57 billion for the fiscal year ending June of 2014, which was indicative of an increase of 8.6% versus sales of 2013 (A$8.81 billion) giving the Company the fourth straight year of sales growth. The Company’s dividend yield is also, in general, higher than its comparable companies (such as Downer EDI Limited and Leighton Holdings Limited). The earnings segments hydrocarbons; minerals, metals and chemicals; infrastructure and environment; and power, may have seen slight turbulence owing to economic downturn but still have the potential to resurrect the growth wave given WOR’s internal efforts.

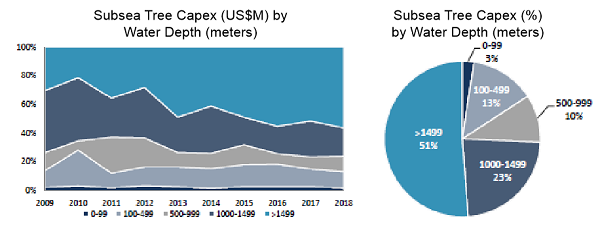

Deepwater CAPEX (Source – Company Reports)

As highlighted by WOR during its investor day, its global major projects outlook is flanked by key projects with significant procurement spend winding down in FY15, margin improvement focus, development of Global Delivery Centers, expectation of projects in early FEED moving forward, ramping up of awards in FY15 as we recently witnessed, and tracking several proposals and prospects. The positives catalysts entail recovery in oil prices, value-accretive acquisitions, and cost management strategy. On the other hand, a high level of competition, any delays in projects, contract execution failure and failure to convert new opportunities in LNG, deep-water, US downstream and Norwegian Continental Shelf markets may prove detrimental to some extent. With a gradual bounce in oil price, there is much more to be expected from WOR. The short term oil price outlook has been harsh but oil prices to be higher on a 6-12 month view since December 2014 is the expectation at large.

WOR Daily Chart (Source - Thomson Reuters)

Accordingly, we put a BUY recommendation for this stock at the current price of $10.42.

Please wait processing your request...

Please wait processing your request...