Kalkine has a fully transformed New Avatar.

Company Overview - WorleyParsons Limited is a professional services business company. The principal activities of the Company consist of providing engineering design and project delivery services, including providing maintenance, support services and advisory services to sectors, which include hydrocarbons; minerals, metals and chemicals, and infrastructure. Its segments include Services, Major Projects, Improve andAdvisian. Its geographic segments include Australia, Pacific, Asia and China; Europe, Middle East and Africa, and Americas. It offers a range of services from small studies to the delivery of mega projects. Its OneWay is an integrity management framework. Its EcoNomics is a framework, which includes Sustainable Decisions, Sustainable Project Delivery and Sustainable Operations. It serves multi-national oil and gas, resources and chemicals companies, as well as regionally and locally focused companies, national oil companies and government owned utilities. It operates in over 40 countries.

WOR Details

Awarded EPCM Contract by Qatar Shell: WorleyParsons Limited (ASX: WOR) has bagged the five-year Engineering, Procurement and Construction Management (EPCm) services contract for the Pearl Gas to Liquids (GTL) and associated facilities in Qatar by Qatar Shell. WOR’s EPCm services is mainly for a portfolio of brownfield projects and the contract would be executed by WorleyParsons Qatar with support from WorleyParsons Global Delivery Center in India. GTL produces 140,000 barrels of GTL products each day and also produces 120,000 barrels per day of natural gas liquids and ethane. Moreover, this contract would strengthen the relationship between WOR and Qatar Shell.

Realignment of the business: WOR has realigned the business into the four business lines of Services, Major Projects, Improve and Advisian in fiscal year of 2016. These efforts are mainly due to the weak performance by the group across its divisions despite their efforts in fiscal year of 2016. WOR Services division aggregated revenue fell 20.7% to $3.4 billion during the period. The segment margin fell to 7.3% as compared to 7.9% in prior corresponding period. Major Project’s division also reported an aggregated revenue decrease to 20.4% to $1.3 billion during the period while the segment margin rose to 8.5% against 7.9%. As per Improve business line, aggregated revenue lost 10.4% to $519.3 million while the segment margin fell to 4.5% as compared to 4.7%. This Aggregated revenue weakness is mainly on the back of reductions in sustaining capital expenditure by oil sands customers. Advisian business line aggregated revenue fell 6.5% to $655.7 million while segment margin fell to 6.8% against 7.5%. But the group is continuing to invest in their business to build a major consulting and advisory business.

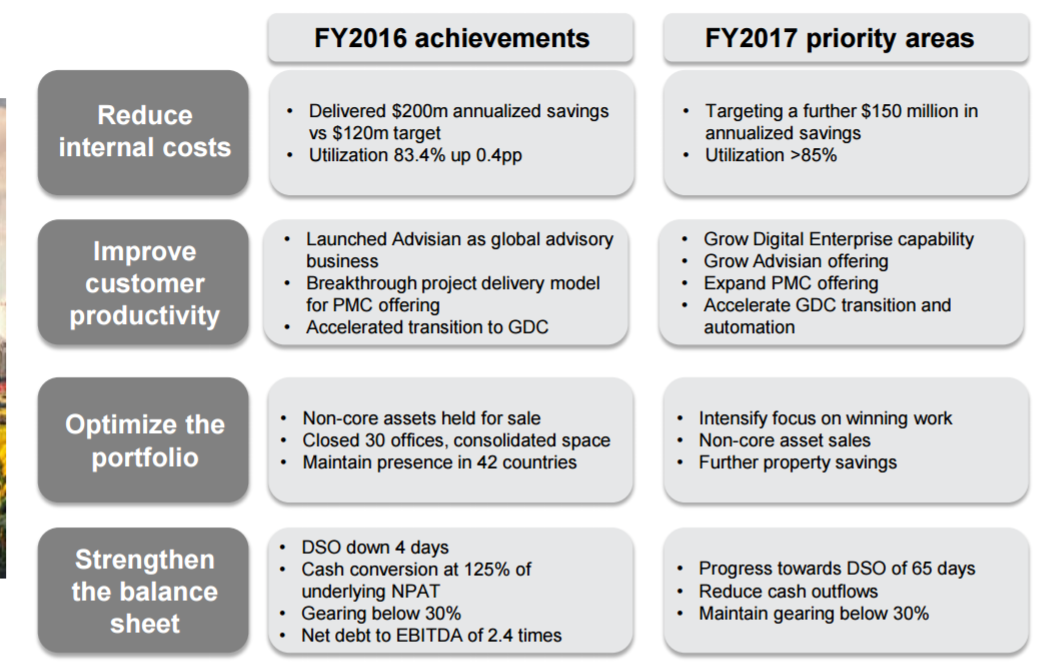

Exceeded the target in the Cost Reduction Program: WOR cut overheads by $170 million as compared to FY 15, exceeding the expectation of $77m. This move is a part of their cost reduction program. By the end of June, WOR had achieved the annualized cost reductions of $200 million, exceeding the target of $120 million. WOR has reduced 800 people since July 2016 and is currently employing 23,700 people. Moreover, WOR had closed 30 offices with an associated floor space reduction of 73,000 square meters for cost savings. Further, WOR has reduced the non-labor spend by reducing third party vendor spend through renegotiation and demand management, restructuring the information technology platform and support organization. These savings reduced the impact of lower revenues due to the fall of the commodity prices on the underlying EBIT margin. Additionally, WOR has identified the initiatives to generate a further $150 million in annualized savings throughout FY 17, raising the overall target from the multi-year program to $350 million from $300 million as anticipated in February. Meanwhile, WOR is looking at the way the company operates and aims to support the business through improved resource management, rising utilization of the Global Delivery Center (GDC), the alignment of remuneration practices with local markets and rationalization of the support functions and general management.

.png)

Delivered $200m in annualized savings (Source: Company Reports)

Strengthened the Balance sheet: WOR has taken steps to strengthen the balance sheet by reducing the net debt by $115 million and improving the net debt to net debt plus equity ratio. WOR has implemented a number of cash conservation measures including lowering capital expenditure, reduced spend on mergers and acquisition, and finalization of the sale of Exmouth power station. Further, to strengthen the balance sheet WOR has decided to not pay a dividend in FY 16. As a result of these initiatives, WOR has reduced the cash outflows by $255 million. Additionally, WOR is targeting an improvement in cash position of $300 million over the medium term. On the other side, the group is offloading their non-core assets to further boost their balance sheet strength while enhance their focus in core assets. Accordingly, WOR has identified non-core assets to be held for sale including the South African public infrastructure business and the WOR’s interest in Cegertec WorleyParsons in Quebec. In fact, WOR has now finalized the sale of the South African public infrastructure business.

.png)

Current balance sheet metrics (Source: Company Reports)

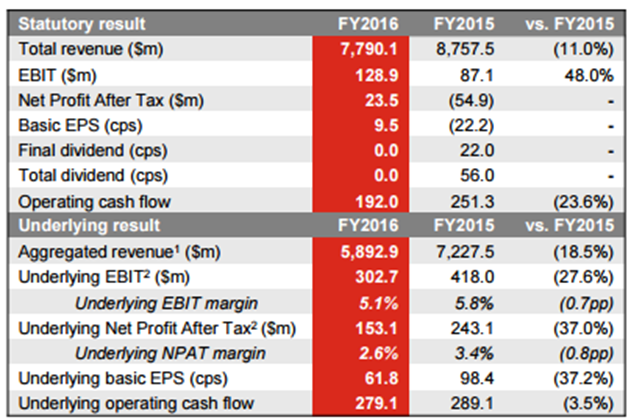

Fiscal year of 2016 Performance: WOR has reported an 11% fall in the statutory revenue in FY 16 which was down to $7,790.1 million. However, the statutory NPAT rose to $23.5 million profit from a $54.9 million loss. Moreover, WOR has posted an 18.5% fall in the aggregated revenue to $5,892.9 million and a 37% fall in the underlying NPAT to $153.1 million. Underlying basic earnings per share (EPS) fell to 61.8 cents in fiscal year of 2016 as compared to 98.4 cents However, the second half showed improvement in the earnings and margins. Operating cash flow reached $192 million during the period as the group generated $87 million in cash outlay for overhead reduction costs. Gearing fell 29.2% as compared to 32.4% in December 2015. The average cost of debt rose 4.8% against 4.7% with interest cover at 5.0 times down from 5.9 times in December, 2015. Net debt to EBITDA fell to 2.4 times as compared to 2.5 times in December 2015.

Financial Performance for FY 16 (Source: Company Reports)

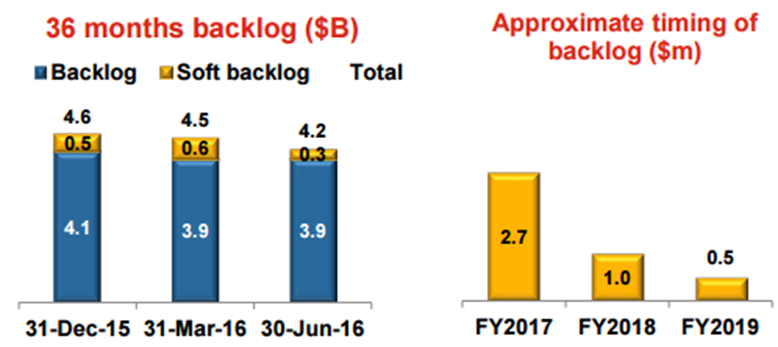

Backlog Scenario: WOR has secured 85 significant contracts for a total value in excess of $2.8 billion in FY 16 as compared to 105 significant awards for the prior corresponding period with a contract value in excess of $3.2 billion. The backlog at 30th June 2016 is $4.2 billion, in which $2.7 billion is relating to FY17. This can be compared to $4.6 billion as at 31st December 2015, and $4.5 billion as at 31st March 2016.

Backlog (Source: Company Reports)

Strategic Priorities: WOR’s strategic priorities for FY 17 are to defend and strengthen the leadership position in providing professional services to the onshore conventional and offshore hydrocarbons, heavy oil, and oil sands sectors. Moreover, WOR is seeing opportunities for expansion in sub sectors of chemicals and new energy, including renewables. There are additional opportunities for WOR in all the sectors in Saudi Arabia, and is also looking for opportunities in the power sector, industrial water and supporting investments aligned to China’s One Belt One Road regional development plan. WOR is focused on the ongoing development of the digital capability. Additionally, WOR intends to maintain key competencies in the minerals and metals sectors and wait for the market improvement. Meanwhile, WOR is seeing signs of recovery in trading conditions with the recovery of the commodity prices.

Priorities (Source: Company Reports)

Stock Performance:WOR stock surged 59.52% in the six months (as of November 22, 2016). Given the volatile environment, the group’s customers in resource and energy segments have cut capital and operating expenditure. Despite this pressure, WOR has successfully won 85 major contracts in the fiscal year of 2016 wherein the overall contract value exceeded $2.8 billion. Advisian and Project Management Consulting divisions also contributed to these awards. The group was also able to decrease their debtor days outstanding by four days during the second half of financial year 2016 and is now aiming to cut this by 15 days. WOR is targeting the debtor days outstanding in line with the industry average of 65 days. Cash outflows were reduced by over $255 million driven from their efforts of cutting capital expenditure and spending on acquisitions. WOR did not declare their dividend to maintain the cash flow even though this move disappointed the investors to some extent. The group is now aiming for $300m improvement in cash, selling selected non-core assets, maintaining the net debt/EBITDA to be in the range of 1.5-2.0 times, gearing to be less than 30% and building capacity for dividend. We give a “Buy” recommendation on the stock at the current price of – $ 9.20

WOR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...