Kalkine has a fully transformed New Avatar.

Company Overview: WorleyParsons Limited is a professional services business company. The principal activities of the Company consist of providing engineering design and project delivery services, including providing maintenance, support services and advisory services to sectors, which include hydrocarbons; minerals, metals and chemicals, and infrastructure. Its segments include Advisian, Energy and Chemical Services, Mining, Minerals & Metals Services and Major Projects and Integrated Solutions. It offers a range of services from small studies to the delivery of mega projects. Its OneWay is an integrity management framework. Its EcoNomics is a framework, which includes Sustainable Decisions, Sustainable Project Delivery and Sustainable Operations. It serves multi-national oil and gas, resources and chemicals companies, as well as regionally and locally focused companies, national oil companies and government owned utilities.

.png)

WOR Details

New Energy Source Expected To Provide Huge Opportunities: WorleyParsons Limited (ASX: WOR) has an engagement in providing engineering design and project delivery services, including providing maintenance, reliability support services and advisory services in sectors such as Hydrocarbons (extraction and processing of oil and gas), Minerals, Metals & Chemicals (extraction and processing of mineral resources and manufacturing of chemicals) and Infrastructure (projects related to water, environment, transport, ports and site remediation and decommissioning; and all forms of power generation, transmission and distribution). Improving market conditions, recent acquisitions, respectable bottom-line performance, decent balance sheet, proper risk mitigation system, decent product outlook, etc. are expected to act as tailwinds for the company in delivering sustainable value to its shareholders in the long run. From the financial standpoint, the company has achieved a significant growth path from FY16 profit before extraordinary items of $23.5 million to $143.9 Mn in FY18, posting a CAGR growth of 147.5% over FY16-FY18.

Transition from the traditional energy source to the alternative and green energy sources is expected to provide a huge opportunity for the WorleyParsons in the coming decade.

.PNG)

Current Focus on Growth (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 48.76% of the total shareholding. Dar Al-Handasah Shair and Partners Holdings Ltd. and Jacobs Engineering Group Inc. hold maximum interest in the company at 20.23% and 9.90%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Footing In Key Margins Reflects Improving Financials: WorleyParsons Limited’s key financial ratios witnessed an improvement on the YoY basis as its net margin stood at 3.3%, which reflects a marginal rise of 0.5% on the YoY and, thus, it can be said that the company’s capabilities to convert its top line into bottom line has been improved. Additionally, its gross and EBITDA margin in 1H FY 2019 stood at 8% and 6.9%, which implies an increase of 0.8% and 0.1%, respectively on the YoY basis.

It seems like that the company is possessing decent liquidity levels as is evident from its current ratio of 3.31x at the end of 1H FY 2019 and can be said that the company would be able to meet its short-term obligations. Also, it can be said that the company would be able to make deployments towards strategic operational activities which might act as the growth catalysts moving forward.

It looks like that the company has been reducing its exposure towards debt component which could further help in stabilizing the balance sheet of the company. This can be seen from its 1H FY 2019 Debt/Equity ratio of 0.13x which has witnessed a significant fall of 74% on the YoY basis. Not only this, the company’s long-term debt as a percentage to total capital stood at 9.3% reflecting a fall of 15.9% on the YoY basis. The deleveraged balance sheet is generally considered as positive largely because it reduces the future commitments.

.png)

Key Ratios (Source: Thomson Reuters)

Key Risks: Long term objective of on the company can have impact from various risks such as health, safety and environment risks, operating risks including payment of fees and liability for costs and delays, risk related to volatile commodity prices, stiff competition, climate change risk, liquidity risks, and risk associated with multiple jurisdiction where different regulatory and compliance issue can delay the work outcome, which may lead to not accurately meeting forecasted numbers.

H1FY19 (ended on December 31, 2018) Key Highlights: The company stated that its aggregated revenue witnessed a rise of 11.1% to $2,566.2 million in 1HFY19. This result can be attributed to improved market conditions and the inclusion of a full six months of revenue from the UK Integrated Solutions business. The statutory net profit after tax (NPAT) for the half year period was reported at $82.4 million as compared to $1.4 million in the previous corresponding period. The cash flow from operations was reported at $21.0 million, which is down from the $44.3 million in the previous corresponding period. Company’s net debt increased to $783.9 million up from $662.5 million at June 2018, which was mainly driven by foreign exchange movement. Company’s contract backlog increased to $6.6 billion as at December 31, 2018, which is an increase of 10% from the previous corresponding period.

During the period, the total recordable case frequency rate for employees improved to 0.10 (per 200,000 man-hours) compared to 0.12 as at June 30, 2018.

.png)

H1FY19 Income Statement (Source: Company Reports)

Sector Overview: The Hydrocarbons sector reported an increase in revenue by 13% pcp to $1,949.7 million in 1HFY19. This was due to the result of the full period of UK IS, growth in Norway and Canada West partially offset by lower revenues in the US, Cord and parts of the Middle East.

During 1HFY19, the Minerals, Metals & Chemicals sector reported an increase in revenue by 23.9% pcp to $265.3 million. The increase in the aggregated revenue was mainly because of Major Projects in Australia, with Advisian also seeing an increase in the early phase work. The Infrastructure sector reported a decrease in revenue by 5.2% pcp to $351.2 million.

What to expect: As market conditions are improving, Company’s resources and energy customers are increasing early phase activity for the next cycle of investment. This is reflected in recent level of contract awards as well as the growing backlog. JacobsECR acquisition is expected to help the company in becoming important player across hydrocarbons, chemicals and minerals & metals in the global arena, and deliver enhanced earnings diversification and resilience, including greater exposure to more stable customer operational expenditure revenues.

As per the International Energy Agency (IEA), World Energy Outlook 2018, there will be a shift in the energy sources by the year 2040. As can be seen from the below table that under new policies and sustainable development, traditional energy sources such as coal and oil may lose their market share to modern energy sources, which include gas, nuclear and renewables by the year 2040. Core sectors which will support the energy transition are, a. Upstream & midstream; b. Downstream & chemicals; c. Mining, minerals & metals; and d. Power & new energy.

.png)

Energy Demand Projection (Source: Company Reports)

Upstream & Midstream Sector Opportunities: Upstream investment has been estimated at 11% CAGR for gas and 4% CAGR for oil from 2019 to 2022. The Midstream market is experiencing a sharp increase in project sanctions aligned to the company’s global footprint. As per the company reports, company finds growth opportunities across the value chain i.e. a. Oil & gas production, processing, storage & transport; b. Greenfield LNG outside battery limits (“OSBL”) and MMO; c. Floating storage & regasification; and d. Gas-fired power generation, transmission & distribution.

.png)

Oil and Gas Investment (Source: Company Reports)

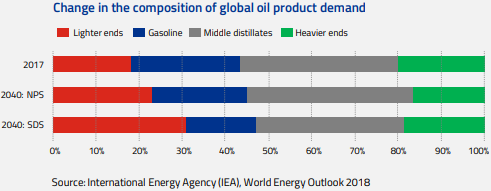

Downstream & Chemicals Opportunities: Major shifts in the composition of oil product demand is presenting challenges for refiners i.e., a. fall in demand for gasoline and diesel; b. demand for lighter feedstock supply; c. increased proportion for chemical feedstock; d. decreased yields for residues; e. response to IMO 2020 regulations. The changes are driving investment in upgrades and brownfield projects with CAPEX investment expecting 5.5% CAGR to 2022 (3 year CAGR). Company is well-positioned with its customers, geographic diversity and leading desulphurization technologies, to grab the opportunity.

Global Oil Product Demand Transition (Source: Company Reports)

As per International Energy Agency report under Sustainable Development Scenario, primary chemical demand strength is expected to increase by 30% to 2030, and the long-term growth would be underpinned by demand for end-use products (e.g. plastics, fertilizers) by developing economies. Capability and geographic positioning in investment hotspots provide strong growth platform.

Global Primary Chemical Production by Scenario (Source: Company Reports)

Mining, minerals & metals (MMM) opportunities: Company’s core MMM capability is well aligned to metals critical to the energy transition such as aluminium, copper & nickel and lithium & cobalt.

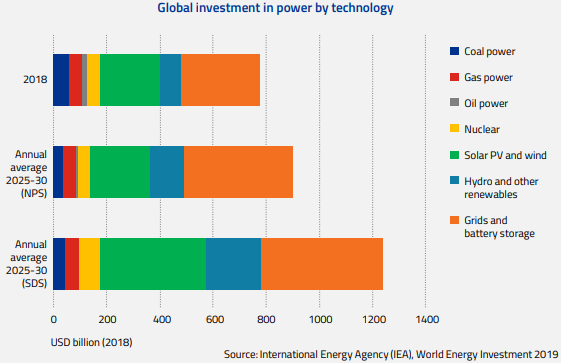

Power & new energy opportunities: As per IEA data, global investments are trending towards new energy sources which are solar and wind, nuclear, hydro and power networks and storage. The focus areas for growth would be offshore wind, distributed energy systems (including microgrids & storage), emerging technologies (hydrogen) and power operations & maintenance.

Global Investment in Power (Source: Company Reports)

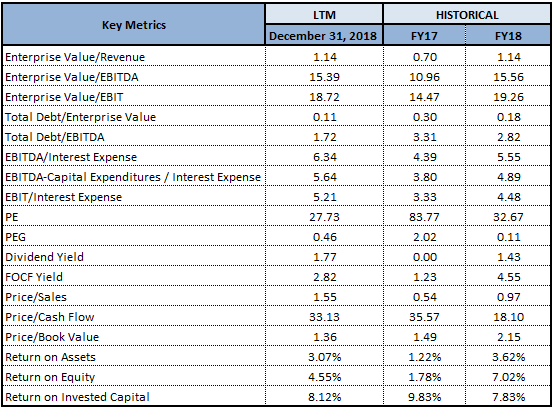

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: WorleyParsons Limited’s share delivered a decent Year-to-Date return of 30.60%, while in the span of the previous six months the returns stood at 6.32%. It is presently trading slightly above the average of 52 weeks high and 52 weeks low levels of $20.028 and $10.720, respectively. Given the backdrop of a strong balance sheet, and decent bottom-line growth over the past three years, the company’s future earnings look promising. Hence, we give a “Buy” recommendation on the stock at the current market price of $15.410 per share (up 2.121% on July 24, 2019), and expect a high single to low double-digit growth in 12-18 months.

.png)

WOR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...