Kalkine has a fully transformed New Avatar.

Company Overview: WorleyParsons Limited is a professional services business company. The principal activities of the Company consist of providing engineering design and project delivery services, including providing maintenance, support services and advisory services to sectors, which include hydrocarbons; minerals, metals and chemicals, and infrastructure. Its segments include Advisian, Energy and Chemical Services, Mining, Minerals & Metals Services and Major Projects and Integrated Solutions. It offers a range of services from small studies to the delivery of mega projects. Its OneWay is an integrity management framework. Its EcoNomics is a framework, which includes Sustainable Decisions, Sustainable Project Delivery and Sustainable Operations. It serves multi-national oil and gas, resources and chemicals companies, as well as regionally and locally focused companies, national oil companies and government owned utilities.

.png)

WOR Details

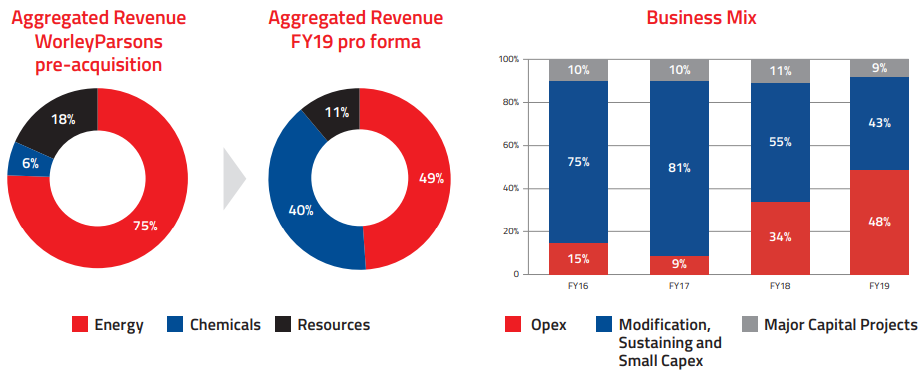

Underlying NPATA increased by 42.7% on yoy to $259.8 Mn in FY19: WorleyParsons Limited (ASX: WOR) is involved in providing engineering design and project delivery services, including providing maintenance, reliability support services and advisory services in various sectors such as Hydrocarbons (extraction and processing of oil and gas), Minerals, Metals & Chemicals (extraction and processing of mineral resources and manufacture of chemicals), and Infrastructure (projects related to water, environment, transport, ports and site remediation and decommissioning and all forms of power generation, transmission and distribution). On August 21, 2019, WOR released its annual report for FY19 wherein it highlighted that the company completed the acquisition of energy, chemical and resources division of Jacobs Engineering Group Inc. or “ECR” in the month of April 2019, which positioned the company as a pre-eminent global player in energy, chemicals and resources sector. Its aggregated revenue grew by 35.6% to $6,439.1 million in FY19 as compared to the prior year. The underlying NPATA increased by 42.7% to $259.8 million as compared to the prior year, which can be attributed to the performance of the Major Projects & Integrated Solutions (MPIS) line of business. It delivered a cash flow of $236.3 million as compared to $259.7 million in FY18. Its Backlog on June 30, 2019 was $18 Bn as compared to $16.4 Bn on June 30, 2018. The period witnessed an improvement in NPATA margin with Backlog grew by 10% during the year across all sectors with a strong increase in the Americas, largely on the back of the ECR acquisition. Its gearing is at 20.9% at 30 June 2019, and leverage has remained flat at 1.9 times. The funding structure of the ECR acquisition has allowed the leverage to remain flat through the transaction. The Board of Directors declared an unfranked final dividend payment of 15.0 cents per fully paid ordinary share, which is in addition to the interim dividend of 27.5 cents per share for the full year. The record date and payment date are on August 28, 2019 and September 25, 2019, respectively.

Considering a decent outlook in energy, chemical and resources sector, especially in the developing and under-developed market, we presume that the company might enhance its global footprints and market share in the upcoming period. Presently, it has a presence in ~ 51 countries and employs more than 57K people around the globe.

.png)

FY2019 Key Financial Metrics (Source: Company Reports)

Line of Business Performance in FY19:

Energy & Chemicals Services aggregated revenue increased by 28.64% on Y-o-Y: The Energy & Chemicals Services reported aggregated revenue of $2,854.2 million and segment result of $278.8 million in FY2019 as compared to aggregated revenue of $2,218.7 million and segment result of $227.0 million in FY2018. The segment margin was decreased marginally to 9.8% from 10.2%. The increase in aggregated revenue can be attributed to the acquisition of ECR and growth in North America and the Middle East.

.png)

Revenue from Energy & Chemicals Services (Source: Company Reports)

Mining, Minerals & Metals Servicesaggregated revenue increased by 88.66% on Y-o-Y: The segment reported aggregated revenue of $286.2 million and segment result of $31 million in FY2019 as compared to aggregated revenue of $151.7 million and segment result of $9.2 million in FY2018. The segment margin witnessed a sharp improvement of 10.8% from 6.1% in the previous year. Significant projects within Australia and Mongolia drove the aggregated revenue growth in FY2019.

.png)

Revenue from Mining, Minerals & Metals Services (Source: Company Reports)

Major Projects & Integrated Solutionsaggregated revenue increased by ~47.1% on Y-o-Y: The segment reported aggregated revenue of $2,745 million and segment result of $231.7 million in FY2019 as compared to aggregated revenue of $1,866.6 million and segment result of $172.4 million in FY2018. The segment margin declined to 8.4% from 9.2%. Aggregated revenue increased on account of the acquisition of ECR, increased procurement revenue in the UK Integrated Solutions business in the North Sea and an upturn in the Norway business.

.png)

Revenue from Major Projects & Integrated Solutions (Source: Company Reports)

Advisian aggregated revenue increased by 8.1% on pcp: Advisian reported aggregated revenue of $553.7 million and segment result of $35 million in FY2019 as compared to aggregated revenue of $512.2 million and segment result of $17.5 million in FY2018. The segment margin improved to 6.3% from 3.4%. The increase in aggregated revenue was driven by increased project with undertaken by INTECSEA, specifically with project work in India.

.png)

Revenue from Advisian (Source: Company Reports)

Sector Performance in FY19:

Aggregated revenue from Energy sector increased by 20% in FY19 to$4,480.1 million with segment result of $437.1 million and margin of 9.8% as compared to segment result of $347.7 million and segment margin of 9.3% in FY2018. The increase in aggregated revenue is a result of the ECR acquisition, increased project revenue from a key international oil company customer, and increased project work in Saudi Arabia. Strong growth in Canada, Oman and Qatar also supported the increase to aggregated revenue in FY2019.

The Chemicals sector performed well with posting a whopping growth of 121% in aggregated revenue to $1,326.6 million as compared to $599.0 million in FY18. Segment result stood at $94.3 million with a margin of 7.1% in FY2019 as compared to segment result of $43.0 million and segment margin of 7.2% in FY2018. The sector saw continued growth in the North American and Europe markets.

The Resources sector reported aggregated revenue of $632.4 million and segment result of $45.1 million with a margin of 7.1% in FY 2019 as compared to aggregated revenue of $430.1 million, segment result of $35.4 million and segment margin of 8.2% in FY2018. The increase in aggregated revenue was a combination of the acquisition of ECR combined with revenue generated by a major project in Australia.

Sectoral Revenue Contribution (Source: Company Reports)

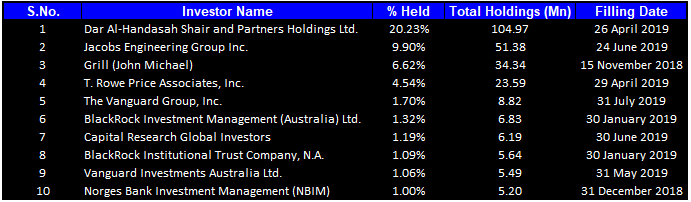

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 48.64% of the total shareholding. Dar Al-Handasah Shair and Partners Holdings Ltd. and Jacobs Engineering Group Inc. hold maximum interest in the company at 20.23% and 9.90%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

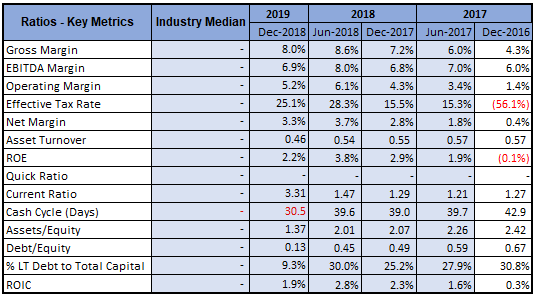

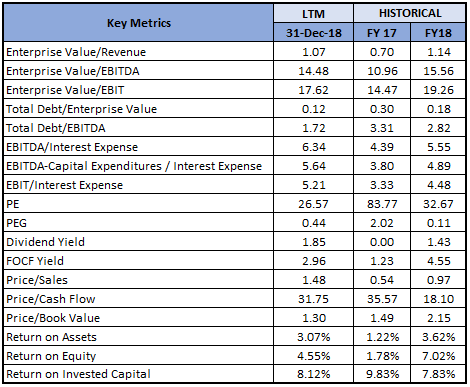

A Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for H1FY19 stood at 8.0%, 6.9% and 3.3%, better than the result in H1FY18 at 7.2%, 6.8% and 2.8%, respectively, which implies decent fundamentals for the company. Its current ratio for H1FY19 stood at 3.31x, better than the result in H1FY18 at 1.29x, which implies the company is in a better position to address its short-term obligations. Its debt to equity ratio for H1FY19 stood at 0.13x, lower the result in H1FY18 at 0.49x, which implies the company is deleveraging its balance sheet and generating enough cash to fuel its operations.

Key Metrics (Source: Thomson Reuters)

Recent Updates: Rosenberg Worley, Worley’s Norwegian subsidiary, has been selected by Vår Energi AS to provide life extension services for their Jotun A FPSO (floating production storage offloading) vessel. Rosenberg will provide management, engineering, procurement, refurbishment, construction and commissioning services for the FPSO. It will involve decommissioning, refurbishment in the yard in Stavanger and offshore deployment. The project will enable the continued production of oil and gas from the Balder field until 2045.

INTECSEA Inc, a wholly-owned subsidiary of Worley, has been awarded a project management consultancy contract by Reliance Industries Limited for the MJ Field deep-water gas and condensate project. Under the contract, INTECSEA Inc will provide PMC services for the development of Reliance’s subsea gas and condensate resource located in deep water of approximately 1,000 meters in the MJ Field offshore of India. The contract covers the engineering, procurement and construction phases and involves subsea facilities and offshore processing using a floating production storage and offloading facility and existing gas trunk line.

Key Risks:The company is vulnerable to certain risks such as health, safety and environment risk, operating risks (contract management risk, demand risk, project delivery risk, cybersecurity risk), reputation risk, financial risks (liquidity risk, internal reporting risk, taxation risk), and strategic risks (integration risk, climate risk).

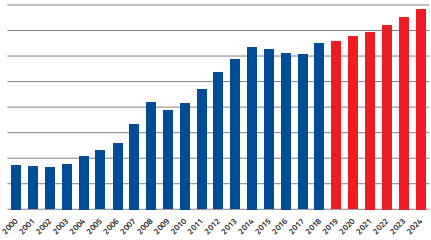

What to expect: The energy, chemicals and resources market indicators and growth in backlog provide evidence of continued improvement in market conditions. Presently, these markets are being tempered by global macroeconomic uncertainty. As a result of the ECR acquisition, the company has enhanced the diversity and resilience of its earnings. WOR has the global technical and financial strength to support its Energy, Chemicals and Resource customers as they navigate a changing world. In FY2020, the company expects to deliver the benefits of the acquisition of ECR, including the realization of cost, margin, and revenue synergies.

Chemicals Capital Expenditure - Trend and Outlook (Source: Company Reports)

Energy Outlook: Global macro trends such as population increase and growth in underdeveloped nations continue to drive world energy demand, with all outlooks forecast growth in the Upstream oil and gas markets to 2040. Gas production volumes continue to grow as countries seek a midterm clean fuel source to fill an expected resource gap caused by the reduced acceptance of coal. Whilst selected intercountry pipelines have been sanctioned, it is the LNG industry that is a primary enabler for the global gas economy. Predicted supply side shortages in the early 2020s have driven investment back into the LNG industry for both greenfield developments and major expansions within the heritage LNG centres. WOR has elevated the LNG subsector to its strategic focus of investments in the coming years.

Renewables such as solar, wind and nuclear power will play a major role in future global energy demands. Grids, including micro-grids and storage will also occupy a significant share in spending as a means to integrate these technologies. WorleyParsons Limited is looking to enhance its portfolio in offshore wind, expand its offerings around distributed energy solutions, position itself as a leader in the emerging hydrogen technology space, and globalize its power operations.

Key Valuation Metrics (Source: Thomson Reuters)

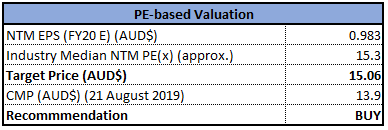

Valuation Methodology: P/E Multiple Approach (NTM):

P/E Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: On the backdrop of decent top-line and bottom-line performance for FY19, respectable margins, past acquisitions, ongoing projects and a promising outlook for energy, chemical, and resources market, it is expected that the company would be delivering sustainable value for its customers and shareholders in the forthcoming time.

WorleyParsons Limited’s share is presently trading below the average of 52-week high and low levels of $20.028 and $10.720, and given the present scenario, the current trading level might be considered as an opportunity for stock accumulation. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, PE multiple, and have arrived at a target price of high single-digit growth (in %). Hence, in view of the aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $13.90 per share, down 3.873% on August 21, 2019.

.png)

WOR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...